Welcome to the Whirlwind

May 12, 2026

Key points

- The conflict in the Middle East is the latest in a series of shocks to hit the US economy over the past several years, Atlanta Fed interim president Cheryl Venable writes in a new quarterly essay.

- A sharp rise in oil prices and shipping costs is intensifying cost pressures for companies that rely heavily on energy.

- If the conflict lasts many more months, prices across the economy could rise enough that consumers will rein in spending, creating an unwelcome combination of pressures on price stability and economic activity.

- It is impossible to forecast with any certainty how economic circumstances will ultimately play out. So far, economic activity broadly appears to be holding up reasonably well, according to aggregate data and feedback from business contacts.

- The labor market shows signs of solidifying after employment growth slowed markedly in 2025. The most recent monthly unemployment rate, 4.3 percent in April, was only 0.1 percentage point higher than a year earlier and below the monthly average during the twenty-first century.

Our recently retired president, Raphael Bostic, began a tradition of publishing a quarterly essay detailing his thoughts on monetary policy and the economy. As the Atlanta Fed's interim president and representative on the Federal Open Market Committee (FOMC), I'm pleased to continue that practice in the spirit of transparency that guides us as a public institution.

Honestly, I've stepped into a bit of a whirlwind when it comes to monetary policy.

First, the good news. In the face of multiple challenges, the macroeconomy is carrying on. It grew 2 percent in the first quarter, according to the initial estimate of real gross domestic product from the US Bureau of Economic Analysis (BEA).

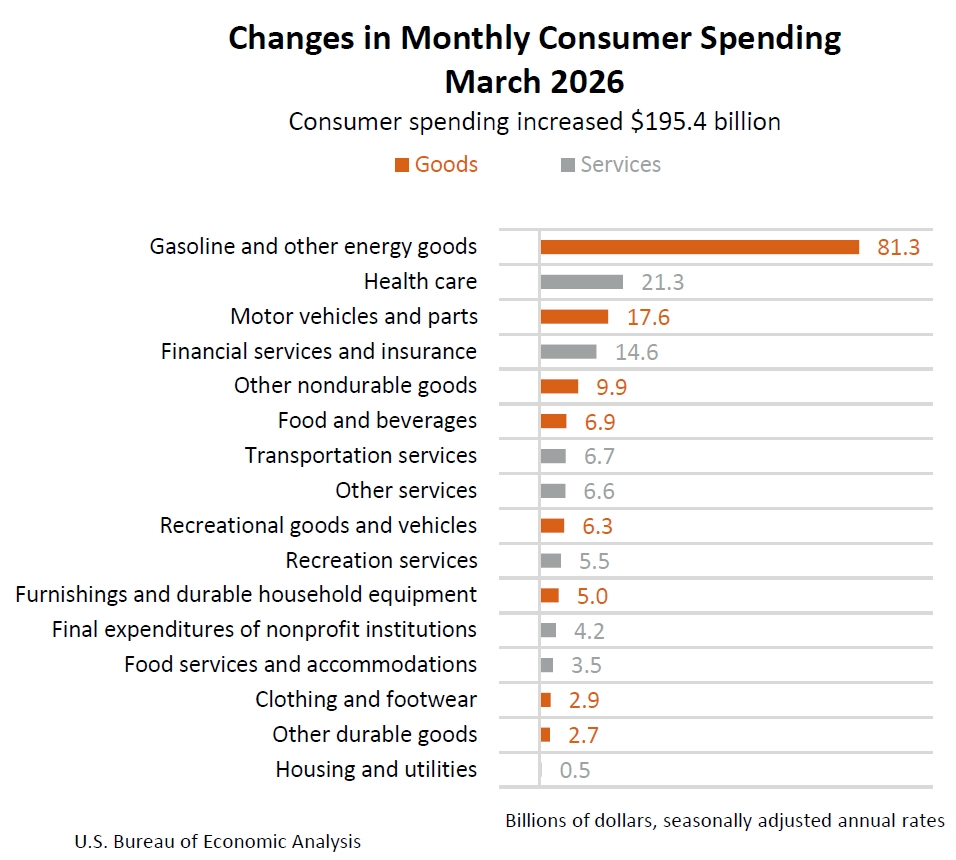

That's about what our staff economists view as the economy's long-term trend growth rate, or the norm. The rate of growth in real (inflation-adjusted) consumer spending did ease a little in the first three months of the year, likely a result of higher gasoline prices compelling consumers to spend less on other items while paying higher prices at the pump. In non-inflation adjusted dollars, and at an annual rate, US consumers spent $81 billion more on gas and other energy products in March than in February, according to the BEA (see chart below). That does not include utilities; it's mainly gasoline. By comparison, the month-over-month increase in spending on gas and other energy goods in February was $6.7 billion.

The trajectory of consumer spending is important, as consumption—households' spending on goods and services—accounts for two-thirds of US economic activity. By and large, though, our business contacts say that demand for products and services is holding up, and their costs haven't yet spiraled as a result of disruptions related to the Middle East conflict.

But the US economy is confronting another in a series of shocks: first came the global pandemic, then an inflation spike, Russia's invasion of Ukraine, tariffs, government shutdowns, and now a conflict in the Middle East that's restricted supplies of petroleum and other commodities vital to the global economy.

This turmoil clouds the economic outlook. A sharp rise in oil prices and shipping costs is intensifying cost pressures for companies that rely heavily on energy, like manufacturers and freight carriers. More worrisome, elevated energy costs over many months could exert upward pressure on prices all across the economy.

And contacts in the energy industry tell our staff and me that oil prices are unlikely to return to pre-conflict levels quickly, even if the Middle East conflict is resolved soon. Keep in mind this is unfolding as inflation has now exceeded the Fed's 2 percent goal for 61 months and counting (through March). Year-over-year inflation for April was 3.8 percent, measured by the consumer price index. The Fed's preferred measure, the personal consumption expenditures price index, is due out in late May but is almost certain to exceed 2 percent.

The Federal Reserve has a dual mandate to pursue price stability and maximum employment. All the factors I've mentioned raise direct concerns about price stability. Coming off the post-COVID-19 inflation spike and price increases related to tariffs, consumers may find that they can only take so much. Further price increases on top of already-elevated inflation could slow down real aggregate spending growth and begin a chain of effects culminating in potential damage to the labor market. Lower spending growth would mean reduced demand across the economy, which in turn would lower firms' revenues, and likely compel companies to cut costs. Since labor is a significant expense for most businesses, payroll would probably be a target for cost cutting.

Labor market appears to be solidifying

Right now, the labor market continues to look solid, if a tad unusual. Following a significant slowdown in 2025, employment growth strengthened in early 2026. Monthly job growth averaged about 76,000 new jobs through the first four months of this year, according to the US Bureau of Labor Statistics. That followed meager increases of just 10,000 net new jobs a month in 2025, which represented a sharp deceleration from 122,000 jobs a month in 2024 and even stronger numbers in 2023.

At his news conference after the April FOMC meeting, Fed Chair Jerome Powell described this situation as an "uncomfortable" state of balance in the labor market. He was referring to the reality that we don't need as many new jobs to keep the unemployment rate steady because the labor force is barely growing. (That is largely due to reduced immigration.)

In fact, the most recent monthly unemployment rate, in April, was 4.3 percent, only 0.1 percentage point higher than a year earlier and below the monthly average during the twenty-first century.

US economy has been resilient

In sum, what my Atlanta Fed colleagues and I are hearing through conversations with contacts and the Bank's surveys of business leaders goes like this: most contacts say the disruptions emanating from the Middle East are not meaningfully affecting business yet. But, if the conflict lasts many more months, prices may rise enough that consumers will rein in spending, creating an unwelcome combination of pressures on price stability and economic activity.

Frankly, it's impossible to forecast with any certainty how these circumstances will play out. At this point, projections of a slow recovery from the effects of the conflict are grounded more in speculation than fact. That said, the longer the turmoil lasts, the more concerned I become.

To bring this home, what does today's complex economic and geopolitical environment mean for monetary policy? Look to the April FOMC meeting. In my view, the Committee acted appropriately in leaving the federal funds rate target at 3.5 to 3.75 percent. As the chair explained, monetary policy appears to be mildly restrictive to neutral, positioning the Committee well to react once macroeconomic conditions begin to clarify.

With inflation still well above our target, and renewed price pressures brewing from a historic disruption in global oil supplies, the time is not right to loosen policy and risk stoking further inflation. Nor is it clear that now is the time to react forcefully to these new inflationary pressures, as doing so could upset the unusual balance in today's labor markets. Therefore, I think the optimal policy approach in the face of risks to both sides of the dual mandate is to wait and see.

The performance of the economy has been steady, yet the road ahead looks bumpy. The team here at the Atlanta Fed and I will remain diligent in tracking these fluid conditions and crafting the best monetary policy stance to achieve our twin goals of full employment and price stability on behalf of the American people.