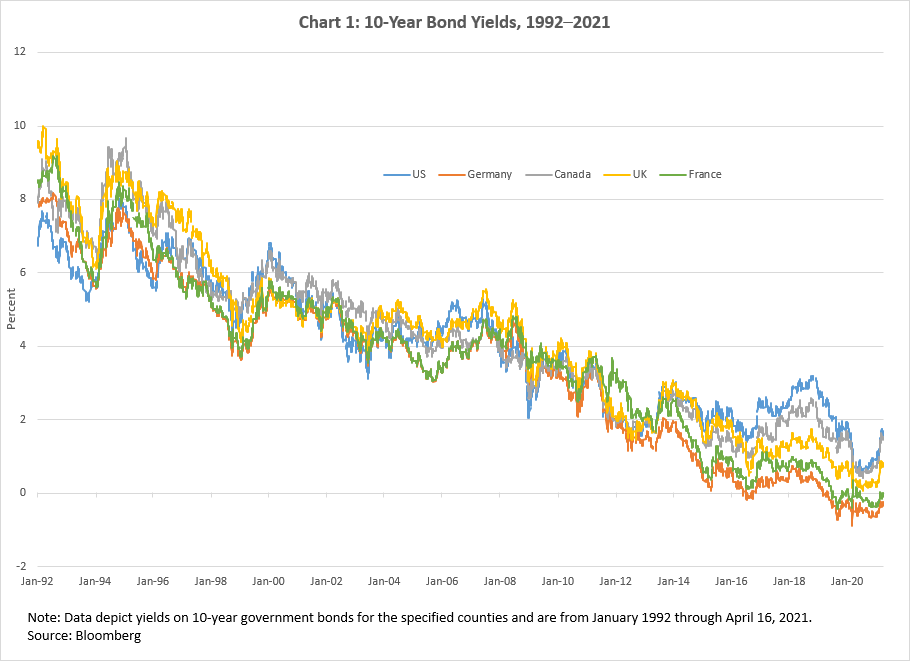

The answer to this question seems obvious simply from observing the secular comovement of global nominal yields across some advanced economies plotted in chart 1.

This observation raises the possibility that domestic bond yields, including those in the large U.S. Treasury market, may be anchored by global economic developments (see, for example, here![]() and here

and here![]() ), provision of global liquidity, and international markets arbitrage. The synchronized dynamics in global yields during the last few months serve as a stark reminder of the powerful role that global bond markets play in the transmission of country-specific shocks as well as of monetary and fiscal impulses.

), provision of global liquidity, and international markets arbitrage. The synchronized dynamics in global yields during the last few months serve as a stark reminder of the powerful role that global bond markets play in the transmission of country-specific shocks as well as of monetary and fiscal impulses.

Yet the standard term structure models (see, for example, here![]() ), that policymakers and market participants use to form their expectations about the future path of the policy rate, are typically estimated only with information embedded in domestic yields. Global influences enter only via the term premia—that is, the extra returns that investors demand to hold long-term bonds—and are influenced by the flight to safety and arbitrage across international markets. But because the term premia are obtained as a residual component in the model, any misspecification of the factor structure that drives equilibrium interest rates—by omitting a common global factor, for example—may result in erroneously attributing some fundamental movements to the term premia.

), that policymakers and market participants use to form their expectations about the future path of the policy rate, are typically estimated only with information embedded in domestic yields. Global influences enter only via the term premia—that is, the extra returns that investors demand to hold long-term bonds—and are influenced by the flight to safety and arbitrage across international markets. But because the term premia are obtained as a residual component in the model, any misspecification of the factor structure that drives equilibrium interest rates—by omitting a common global factor, for example—may result in erroneously attributing some fundamental movements to the term premia.

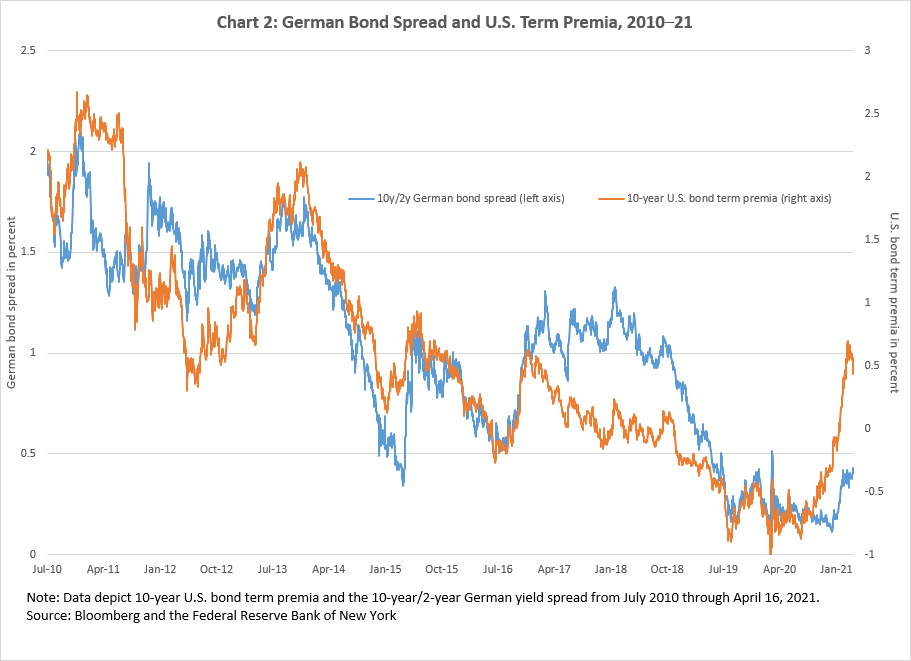

Chart 2 illustrates this point, presenting a less-noticed and even overlooked empirical regularity between the term premia![]() on the spread between the 10-year U.S. bond and the 10-year/2-year German bond, which is the benchmark bond for the Eurozone government bond market. This comovement has proved remarkably strong since 2014.1

on the spread between the 10-year U.S. bond and the 10-year/2-year German bond, which is the benchmark bond for the Eurozone government bond market. This comovement has proved remarkably strong since 2014.1

Take, for example, the pronounced decline in the term premia and the accompanying slide in the German bond spread between 2014 and 2019. Although technical factors might be behind the downward trend in the German bond spread—for example, large Eurozone bond outflows triggered by the euro-area crisis and the introduction of negative interest rates—the slope of the yield curve could also convey important information about the fundamentals of the economy. If the term premia on the 10-year U.S. bond reflect an exogenous "distortion" in the U.S. yield curve due to a flight to safety or an elevated demand for global safe assets, yields are likely to return to normal levels when the uncertainty shock dissipates. In contrast, if investors interpret the yield curve's decline as an endogenous "risk-off" response—that is, a switch to less risky assets—to a deteriorated global environment that can spill over to the U.S. economy, the term structure model would require a "global" factor whose omission may otherwise contaminate an estimate of the term premia.

So how sensitive is the estimate of the future path of policy rate to model specification? I next illustrate this sensitivity by augmenting the factor space in a standard (five-factor) term structure model with incremental information from an additional global factor, not contained in the other factors. Given the reasonably tight correlation between the term premia for the 10-year U.S. bond and the 10-year/2-year German bond spread, it seems natural to use the latter as an observed proxy for a global factor, although other statistical approaches for extracting one or more common global factors are certainly possible.

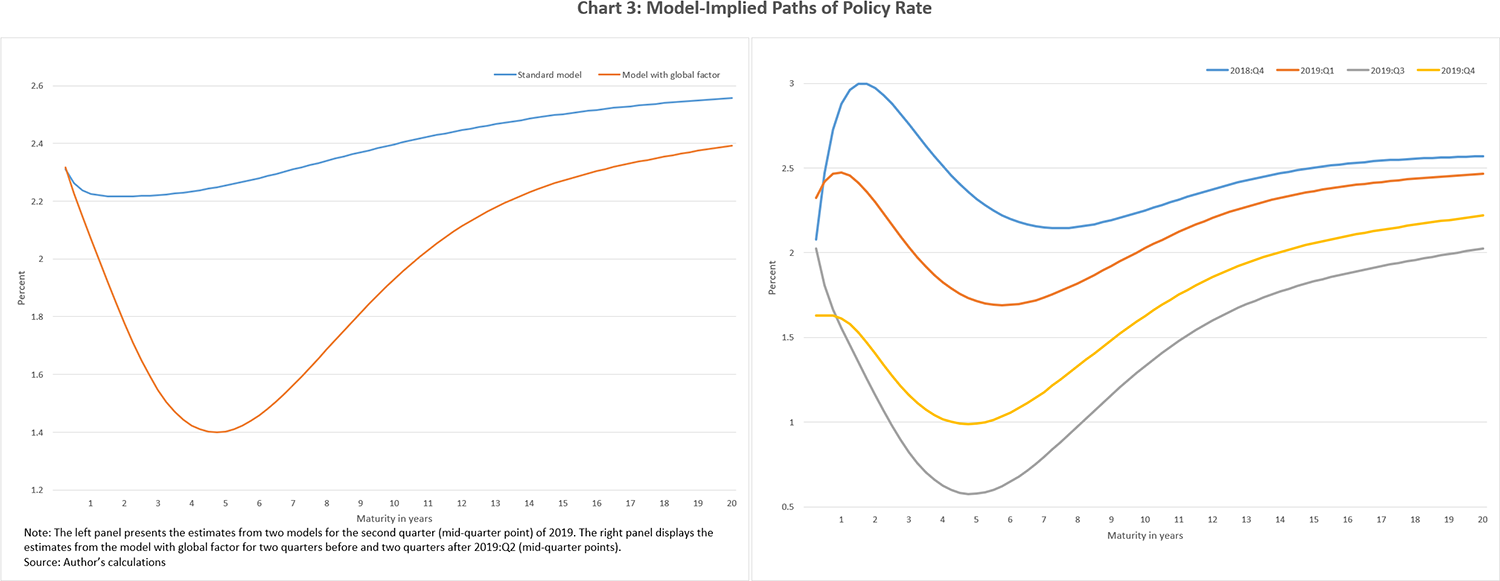

To quantify the potential effect of the global factor, I focus on yield curve dynamics seen in 2019, a period characterized by elevated economic, trade, and geopolitical uncertainty that led to a material decline in observed yields. But did a fundamental shift in the expected path of policy rate, or lower term premia, drive this decline? In the left panel of chart 3, I plot the expected policy rate paths for the second quarter (or midpoint) of 2019, obtained from models with and without a global factor. (Recall that in the second quarter of 2019, the target range for the federal funds rate was 2.25 percent to 2.50 percent.)

The difference in the shape of the expected policy rate paths implied by the two models is striking. (The models' estimates use unsmoothed yield data at quarterly frequency, with continuous bond maturities from one to 80 quarters.) Although the expected policy rate path for the standard model is fairly flat, the rate path for the model with a global factor is deeply inverted up to five-year maturities, suggesting that over this horizon one could have expected rate cuts of almost 100 basis points. These expectations occurred against the backdrop of stable growth and inflation outlook in the United States but deteriorating global economic and trade conditions. The right panel of chart 3 displays the evolution of the expected rate path, estimated from the global factor model, for the two quarters before and the two quarters after the second quarter of 2019, as the Federal Reserve started to adjust its policy rate lower. It is worth noting that the strong effect of the German 10-year/2-year spread in the term structure model with global factor is a relatively recent phenomenon. (Additional results suggest that this factor has only a muted impact on the model estimates prior to 2014.)

The policy implications of these findings warrant several remarks. One direct implication is that the common global determinants of the neutral rate of interest, as well as inflationary dynamics, could constrain the potency of domestic monetary policy. A prime example of these constraints was the policy rate normalization phase undertaken by the Fed during the 2016–18 period, which was characterized by global disinflationary pressures, underwhelming economic performance in Europe and Japan, slowing economic growth in China, and escalating trade tensions. These forces were potentially counteracting the Fed's policy efforts and exerting downward pressure on the global neutral rate of interest. The recent economic and financial developments resulting from the COVID-19 pandemic (such as the global nature of the shock, synchronized monetary and fiscal response across countries, and international financial market comovements) and the ongoing recovery appear to only strengthen the case for the importance of incorporating global information in bond-pricing models.

By

Nikolay Gospodinov, a financial economist and senior adviser in the Atlanta Fed's Research Department

1 [go back]

I should note that the correlation between the two series increased from 52.9 percent before 2014 to 76.2 percent after 2014. Interestingly, the beginning of 2014 marks another important shift in financial markets: a sharp and persistent compression in the breakeven inflation forward curve, as a Liberty Street Economics blog post![]() recently discussed. A similar flattening is present in the forward term premia of nominal bonds. This is consistent with the interpretation that such flattening—starting in 2014—is likely the result of a new regime, characterized by the compression of inflation risk across maturities.

recently discussed. A similar flattening is present in the forward term premia of nominal bonds. This is consistent with the interpretation that such flattening—starting in 2014—is likely the result of a new regime, characterized by the compression of inflation risk across maturities.