One of the big questions for the economic recovery is the extent to which the improvement in the housing sector is sustainable. The statements from the Federal Open Market Committee (FOMC) over the past three years reveal an interesting evolution in the way the Committee views housing activity. Consider the subtle changes:

| - | 06/2009: Household spending has shown further signs of stabilizing but remains constrained by ongoing job losses, lower housing wealth, and tight credit. |

| - | 09/2009: [A]ctivity in the housing sector has increased. |

| - | 11/2009: Activity in the housing sector has increased over recent months. |

| - | 12/2009: The housing sector has shown some signs of improvement over recent months. |

| - | 03/2010: [I]nvestment in nonresidential structures is declining, housing starts have been flat at a depressed level. |

| - | 04/2010: Housing starts have edged up but remain at a depressed level. |

| - | 06/2010: Housing starts remain at a depressed level. |

| - | 09/2010: Housing starts are at a depressed level. |

| - | 11/2010: Housing starts continue to be depressed. |

| - | 12/2010: The housing sector continues to be depressed. |

| - | 08/2011: [T]he housing sector remains depressed. |

| - | 04/2012: Despite some signs of improvement, the housing sector remains depressed. |

| - | 08/2012: Despite some further signs of improvement, the housing sector remains depressed. |

| - | 09/2012: The housing sector has shown some further signs of improvement, albeit from a depressed level. |

| - | 12/2012: [A]nd the housing sector has shown further signs of improvement.... |

| - | 01/2013: [T]he housing sector has shown further improvement. |

| - | 03/2013: [T]he housing sector has strengthened further.... |

| - | 07/2013: [T]he housing sector has been strengthening.... |

I'll leave the exact parsing of FOMC statements to private experts. What I want to address is the way banks are reacting, or perhaps contributing or being less of a barrier, to the strengthening housing sector.

In my July 10 posting, I discussed the correlation between bank construction lending and residential construction activity—larger changes in construction lending are associated with a higher level of construction put in place. Last week the Census Bureau reported that total construction spending fell. The good news is that residential construction, on a seasonally adjusted annual rate, was essentially flat from May to June and was up significantly compared to June 2012. So is bank behavior consistent with improving residential construction spending? Two sources help to shed light on what banks are thinking and doing: the Senior Loan Officer Opinion Survey (SLOOS) and bank call reports as of June 30, 2013.

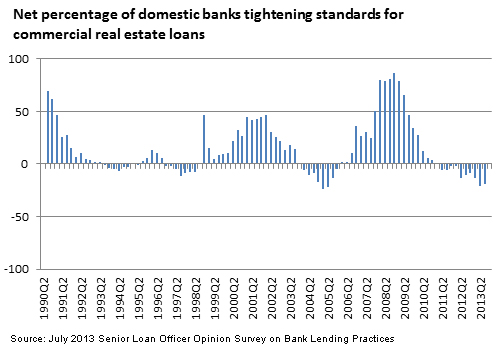

The SLOOS asks how the respondent banks' credit standards for approving applications for commercial real estate loans (CRE) loans have changed over the past three months. Since 2011Q2, the net percentage of domestic banks tightening standards for CRE loans has been negative, which indicates loosening (see the chart). CRE, however, includes not only loans for construction and land development (C&D), but also loans secured by nonfarm, nonresidential properties and multifamily residential properties. The latter two loan types finance existing structures rather than construction activity, thus it is impossible to determine whether the loosening since 2011 applies to construction lending.

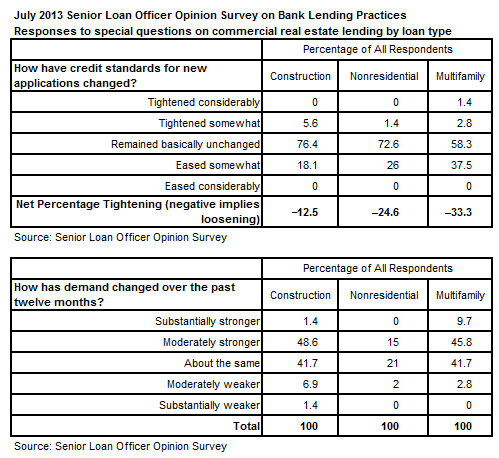

Fortunately, the most recent SLOOS had special questions that asked for the changes in standards and demand over the past 12 months for the three different types of CRE loans: C&D loans, loans secured by nonfarm nonresidential properties, and loans secured by multifamily residential properties.

Though on net the standards for all CRE loans type appear to be loosening, multifamily and nonresidential loans are likely to have been the drivers of the easing of overall CRE standards since 2011Q2. Unfortunately, because these were special questions, there is no time series to aid with putting the responses in context.

Do actions speak louder than words?

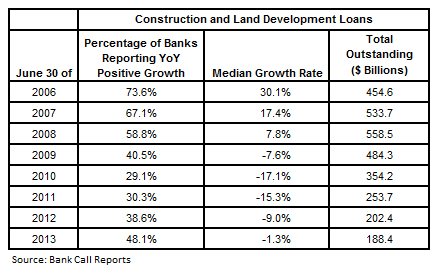

Ideally, to gauge bank lending activity, we would look at the volume of new construction loans—new loans enable new activity. What we observe, however, is total C&D loans outstanding—which net out loan payoffs, write-downs, and reclassifications—continue to be decreasing in aggregate. In contrast to the overall industry where the top 100 banks account for 80 percent of total bank assets, the top 100 C&D lenders, which are not necessarily the top 100 banks, account for only 60 percent of bank C&D lending. Given the available data and the fact that smaller banks are relatively more important in the C&D space, the percentage of banks that are increasing their construction lending may be a better indicator of changing sentiment (see table below).

With 48.1 percent of banks reporting year-over-year growth in C&D loans, activity cannot be classified as robust, but neither is it bouncing along the bottom. Not that we should aspire to the frothy levels of C&D lending that prevailed during the housing bubble, but compared to 2010, it is clear that more banks are reentering the C&D market, which bodes well for housing starts and construction spending going forward.

By Carl Hudson, director of the Center for Real Estate Analytics in the Atlanta Fed's research department