Introduction

Between 2021 and 2022, cities across the country experienced their steepest rent increases in over a decade. According to the Realtor.com’s Rental Report, median rent growth year over year across the top 50 metros was in double-digits throughout the second half of 2021, peaking at 17.5 percent in December. In some markets, rents rose by over 30 percent year over year by early 2022. In this Partners Update, we analyze the discrepancy between recent real-time rent changes and a commonly used indicator of area housing cost, the Department of Housing and Urban Development’s (HUD) Fair Market Rent (FMR) estimates. We discuss the implication of these gaps for FMR users and explore how an updated HUD methodology for calculating FMRs addresses these challenges.

HUD designed its FMRs to determine subsidy amounts for households in its housing assistance programs. They are also an important measure tracked by developers, landlords, researchers, and policymakers to understand local housing costs for policy or development purposes.

In late 2021, we noticed that our estimates of local housing costs produced by the Atlanta Fed’s CLIFF tools were not keeping pace with rising rents across the country. Our estimates used HUD FMRs to represent local housing costs. Inaccurate FMRs directly affected our county-level estimates of the overall cost of living for different family types by underestimating the actual cost of housing.

In early 2022, we began research on the potential gap between HUD FMRs and real-time rent data. We evaluated alternative real-time rent datasets to design a way to adjust HUD FMRs to better reflect up-to-date market rent dynamics. Simultaneous with and apart from this work, HUD reviewed its own methodology for calculating FMRs and updated it to incorporate real-time rent datasets. In July 2022, HUD circulated a new, temporary methodology for comment, and in September 2022 published the 2023 FMRs, calculated using that methodology.

What are Fair Market Rents (FMRs)?

HUD’s FMRs estimate gross rent (shelter plus utilities) and are used in administering HUD’s public and assisted housing programs. FMRs are “the rent, including the cost of utilities (except telephone), as established by HUD for units of varying sizes (by number of bedrooms), that must be paid in the market area to rent privately owned, existing, decent, safe, and sanitary rental housing of modest (non-luxury) nature with suitable amenities.”1 FMRs are calculated annually for each metropolitan and nonmetropolitan area in the United States.2

FMRs are published each year around September 1 and become effective for one year, generally beginning on October 1. Thus, FMR is a forward-looking measure of rent and represents HUD’s best estimate of what rent will be in the year ahead. FMRs are based on the unit’s number of bedrooms and its location. For example, in 2022, a monthly FMR for a two-bedroom apartment was $943 in Birmingham, Alabama, and $1,672 in Miami, Florida. FMRs for a studio apartment were $765 and $1,162, respectively.

How are FMRs Used?

Primarily, FMRs are used by HUD to determine maximum monthly assistance payments (so-called “payment standard amounts”) for households in the Section 8 Housing Choice Voucher (HCV) program, to set public housing flat rents, and to determine initial renewal rents for some expiring project-based Section 8 contracts.

In 2021, 2.3 million households received rental support through the HCV program, and over 840,000 lived in public housing. If FMRs do not accurately reflect the cost of housing in a given area, these households might face financial consequences. For example, if HCV payment standards are set too low, households would not be able to easily use vouchers because their value is below what most landlords ask. Available units with rent at or below the FMR might also be concentrated in high-poverty neighborhoods with poor access to economic opportunity. Research suggests that this can result in so-called “neighborhood effects” that worsen socioeconomic and health outcomes for families, and especially for children.3

HUD FMRs also affect the availability and affordability of privately developed housing stock intended for low-income residents. Low Income Housing Tax Credit (LIHTC) developments may be stacked with project-based Section 8 Housing Vouchers, which are allocated to a unit rather than a household. When this practice is in place, HUD FMRs can directly affect the feasibility and underwriting of these projects. The underlying rents on project-based vouchers are determined by HUD FMRs and, if these rents are included in the project’s financial feasibility analysis, they can increase a project’s financial viability.4 Thus, in markets where rent is high or rising but FMRs have lagged, methodological updates that increase HUD FMRs amounts could bolster feasibility of LIHTC projects that stack with the project-based voucher program.

Increases in FMRs can also affect the affordability of new and existing LIHTC units, which typically are reserved for households under 50 percent or 60 percent Area Median Income (AMI). Rent limits for a LIHTC unit would ordinarily be calculated using 30 percent of the AMI for the unit.5 However, many income limit adjustments affect these maximum-rent scenarios, and in “high housing cost (HHC) areas”–places where the housing cost to income ratio is relatively high–LIHTC rent and eligibility limits are indexed to FMRs instead of area median income. This means that the upper rent limit is no longer directly tied to how much people in the area tend to make. Instead, it is determined by how much people are paying for housing–regardless of whether incomes have kept pace. LIHTC units subject to HHC adjustments may become available to higher-income renters (crowding out lower-income renters) and rents themselves could increase, though the amount that rent can increase in any given year is limited.

In addition to directly affecting the affordability and availability of housing stock, FMRs inform many cost of living measures. The ALICE Threshold, University of Washington Self-Sufficiency Standard, and MIT Living Wage Calculator all use FMRs as an estimate of rental housing cost in a given area. Inaccurate FMRs bias the estimates and lead to incorrect conclusions by researchers and policymakers that rely on them.

Accurate FMRs also affect the analytical tools used to estimate eligibility and the dollar value of public benefits programs. For example, Supplemental Nutrition Assistance Program (SNAP) eligibility determination is based on a family’s net income, which is calculated as total income minus certain deductions, including rent. Some tools that model benefits eligibility, such as Atlanta Fed CLIFF tools and National Center for Children in Poverty’s Family Resource Simulator, use FMRs as an estimate of how much a typical family pays in rent and therefore how much rent deduction it can claim. Inaccurate FMRs lead to incorrect predictions of a family’s eligibility for SNAP and the amount of SNAP benefits a family can receive.

How were FMRs Calculated Prior to 2023?

FMR is a forward-looking measure that uses data from prior years, so HUD first needs to adjust data from past sources for inflation, then to forecast rents one year into the future using model-based techniques. FMR can be broken down into three components:

- A base rent. It represents the 40th percentile gross rent paid by recent movers (those who moved to their present residences within the past two years) into standard-quality dwelling units (defined as a rental unit that is more than 2 years old and has full plumbing and a full kitchen, meals not included). This component is calculated using the most recent American Community Survey (ACS) five-year estimates. For example, 2023 base rents are calculated using 2015-2020 ACS data.

- An inflation-based update factor. Since the base rent estimates are produced using ACS data from prior years, they need to be inflated to the year in which FMRs are determined. An inflation-based update factor is used to adjust for a realized historical rent inflation and to bring the rent values from the year in which the ACS data was collected to the current year.

- A trend factor. Finally, since HUD calculates FMRs in advance of each year, this factor is applied to forecast rent inflation for the year ahead. In HUD’s words, this factor is used “to trend the rentals so that rentals are current for the year to which they apply.”6 For example, the 2023 FMR estimates were determined in 2022 and had to be forecasted one year ahead.

For pre-2023 FMRs, HUD used a weighted average of two Bureau of Labor Statistics (BLS) Consumer Price Index (CPI) components, Rent of Primary Residence and Fuels and Utilities, to inflate rent estimates from the ACS year to the current year. Whenever available, HUD uses local versions of these components, published by BLS for 23 large metropolitan areas. Around half of the US population lives in the metropolitan areas where local inflation measures are available. For the remainder of the country, HUD uses one of four regional CPI measures.

The problem with this methodology is that these two rent components of the CPI reflect changes in average rent paid by all renters, not just recent movers. As a result, FMRs lagged behind the actual “fair” rent on the market, especially in rental markets that experienced greater churn. Moreover, when metropolitan area-level CPI estimates are not available, HUD uses national rent CPI that does not capture actual rent changes, which can be highly heterogeneous across locations.

HUD’s Updated 2023 Methodology

In 2022, in response to both a change in 2020 ACS data availability and local rent increases, HUD implemented a number of improvements to its methodology. The main methodological change was made to the inflation-based update factor. Instead of relying solely on rent CPI to produce inflation adjustments, HUD combined it with real-time measures of rent from six private data sources: RealPage average effective rent per unit, Moody’s Analytics REIS average market rent, CoStar Group average effective rent, CoreLogic Inc. single-family combined three-bedroom median rent, Apartment List Rent Estimates, and Zillow Observed Rent Index. These observed rent data are combined with CPI housing cost and fuels and utilities data to create the rent inflation measure.7 As a result, 2023 FMR estimates based on the updated methodology are more representative of actual rent trends than estimates based on the pre-2023 HUD methodology.

Comparison of Pre-2023 and 2023 FMR Methods

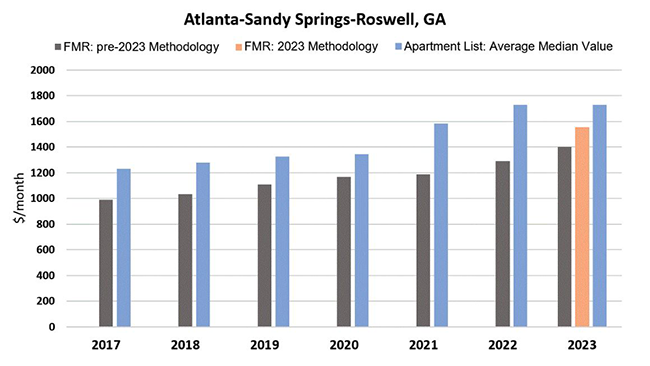

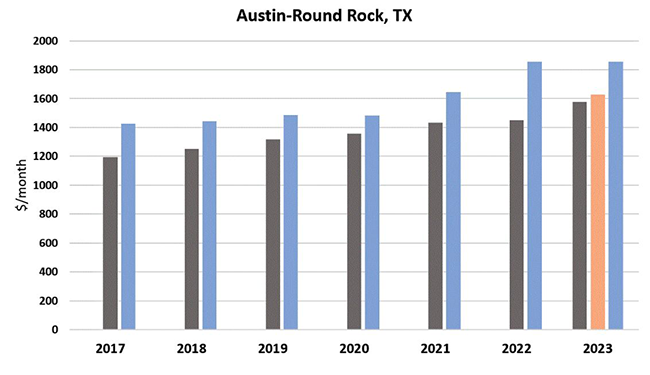

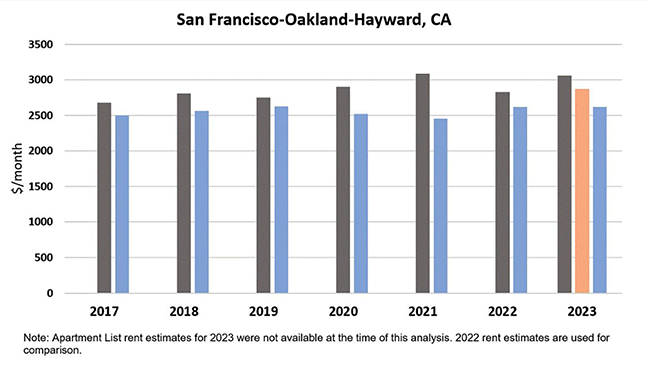

As an illustration, Figure 1 shows the monthly FMR dollar amount in the given year for a two-bedroom apartment alongside the corresponding real-time estimates of rent retrieved from the Apartment List Rent Estimates database. Apartment List data is available online for free and provides monthly estimates of the median rent paid for new leases of one- and two-bedroom apartments in a given market and aggregated at the national, state, core-based statistical area (CBSA), county, and city levels. We show the FMR and real-time Apartment List data for three Metropolitan Statistical Areas (MSAs), Atlanta, Georgia, Austin, Texas, and San Francisco, California. The data is shown for years 2017 to 2022.

Since real-time Apartment List data is not yet available for 2023, for that year we compare FMR to unadjusted 2022 Apartment List estimates. While we don’t expect the Apartment List estimates for 2023 and 2022 to be identical, for the purpose of this analysis the 2022 data is used as a proxy for the not-yet-available 2023 figures. This allows us to visually demonstrate the differences between the pre-2023 methodology and the revised HUD methodology. To do so, we plot two separate FMRs estimates for 2023. The gray bars show the FMR from 2017 to 2023 using HUD’s pre-2023 methodology. The blue bars show Apartment List data for the same time period, in which the estimate for 2023 is the unadjusted 2022 Apartment List estimate, as discussed above. The orange bar, only shown for one year, reflects the FMR using HUD’s new methodology. Figure 1 shows that before adjusting its methodology HUD’s FMRs systematically underestimates the rent for Atlanta and Austin and overestimates it for San Francisco. However, prior to 2021 the discrepancy was relatively small. Atlanta and Austin represent markets where rent rose significantly in 2021 and 2022. In San Francisco, on the contrary, rents fell. Since the inflation-based update factor used by the FMRs captures only average rent inflation, it underestimated the 2021 and 2022 changes in rent in areas where the rent increase was above the average (Atlanta and Austin) and overestimated the 2021 and 2022 changes in rent for places where the rent growth was below the average (San Francisco).

Figure 1: Dollar Difference Between FMRs and Real-Time Apartment List Rent Estimates. Two-Bedroom Apartment

Source: HUD FMR and Apartment List Rent Estimates. Authors' calculations.

Note: Apartment List Rent Estimates do not include utilities, while HUD FMRs do. Apartment List's metro area estimates are also based on Core-Based Statistical Areas (CBSAs), which are different from HUD’s MSAs. For the accuracy of the comparison, we use Apartment List's county estimates and add the value of average monthly utilities provided by the Atlanta Fed Cost-of-Living Database to the Apartment List estimates. In addition, since Apartment List estimates used in this analysis are at the county level, we calculate the average median value by taking the average of estimates for all counties within the given MSA.

The gray and orange bars for 2023 on Figure 1 illustrate the extent to which HUD’s updated methodology remediated the real-time-rent-to-FMR discrepancy. We observe that across three MSAs, HUD’s pre-2023 FMR methodology—when applied to 2023 and adjusted to the CPI—would underestimate or overestimate the actual changes in rents more significantly than the new 2023 HUD FMR methodology. However, a gap persists between the 2023 FMR and the latest available Apartment List real-time rent measure.

With the new methodology, FMR incorporates more timely rent data on the local markets. Several of HUD’s rent data sources are proprietary. See this table that compares HUD FMRs with the two publicly available, real-time rental datasets that are used by HUD, with corresponding methodological differences.

Conclusion

HUD’s updated 2023 methodology allows for changes in real-time rents to inform its annual estimate of FMRs. In doing so, FMRs can more accurately reflect rent prices in more volatile markets, providing more reliable data to cost-of-living and benefits eligibility calculators that use FMRs to estimate housing cost. Updated FMRs may also benefit landlords, HUD-assisted households, and other HUD-funded housing program beneficiaries. Nationally, rents began declining in September 2022 and are currently estimated to be only 3.3 percent higher than February 2022. A retrospective assessment of how the new HUD FMR methodology compares to 2023 real-time rent indicators will reveal how well it performs against the previous methodology.

By Elias Ilin, Sarah Stein, CED adviser, Edgar Reyes, Atlanta Fed economic research analyst, and Grace Meagher, CED research analyst. The views expressed here are the authors’ and not necessarily those of the Federal Reserve Bank of Atlanta or the Federal Reserve System. Any remaining errors are the authors’ responsibility.

_______________________________________

1 24 CFR § 888.111 found at https://www.ecfr.gov/current/title-24/subtitle-B/chapter-VIII/part-888/subpart-A/section-888.111

2 HUD also calculates Small Area FMRs (SAFMR) for metropolitan areas where units leasing to Housing Choice Voucher recipients are concentrated in high poverty areas, among other criteria laid out in 24 CFR § 888.113 (available at https://www.ecfr.gov/current/title-24/subtitle-B/chapter-VIII/part-888/subpart-A/section-888.113.

3 Chetty, Raj, Nathaniel Hendren, and Lawrence F. Katz. 2016. "The Effects of Exposure to Better Neighborhoods on Children: New Evidence from the Moving to Opportunity Experiment." American Economic Review, 106 (4): 855-902; Kling, Jeffery R, Jeffrey B. Liebman, and Lawrence F. Katz. 2007. “Experimental Analysis of Neighborhood Effects.” Econometrica, 75 (1): 83-119.

4 In a recent interview with the Atlanta Fed, a national low-income housing syndicator observed that these stacking practices have become increasingly common in LIHTC proposals over the past five years.

5 26 U.S.C. § 42(g)

6 42 U.S.C. § 1437f (c)(1)(A)

7 HUD calculates weighted averages of the year-over-year change in rent for each rent data source, by area. HUD applies a final measure of rent inflation that treats this figure by weighting it at 60 percent and adding the CPI rent inflation measure at 40 percent. HUD then adds in the CPI Fuels and Utilities index.