A children's health insurance subsidy policy change in Florida has implications for children's access to health care and financial outcomes for families. Led as a bipartisan effort and passed unanimously in both chambers of the Florida legislature, lawmakers extended the eligibility of the Children's Health Insurance Program (CHIP) in Florida from 200 percent of federal poverty level (FPL) to 300 percent of FPL. For a family of four, 200 percent of FPL is $55,500 and 300 percent of FPL is $83,250. (These federal poverty levels are for the year 2022.) This policy change serves as a two-generational strategy because it aims to improve outcomes for both children and their parents. The legislation's intent is to provide continued and expanded access to subsidized health insurance and to help maintain affordable access to primary and preventive health care for children of working families. In addition, the extended eligibility means that parents can earn more income—either through increased hours of work or career advancement—without triggering a "benefits cliff". In this Partners Update, we focus on how the policy change affects parents by mitigating the benefits cliff.

A benefits cliff occurs when working more hours or receiving higher wages puts a family above the income eligibility limit for public assistance programs and the loss of assistance is greater than the value of the wage increase. When this occurs, the family's total financial resources decline even as wages have increased. This can create a dilemma for workers, who must then choose between their family's immediate well-being and financial best interest and their own longer-term wage growth and career advancement.

Policy background

Florida KidCare is the umbrella for several subsidized health insurance programs. Under the existing law, which will change on January 1, 2024, families lose access to subsidies once their income exceeds 200 percent of FPL in three CHIP-funded programs: MediKids, Healthy Kids, and Children's Medical Services. Families that qualify for a subsidy pay a monthly per-household premium of $15 or $20, depending on income level. When families' earnings exceed 200 percent of FPL and they want to continue health insurance coverage for children through KidCare, their current options are to enroll in MediKids Full Pay for children ages 1–4 and pay a $210.18 monthly premium, or Healthy Kids Full Pay for children ages 5–18 and pay $259.50 per month. For some families, a modest wage increase could result in annualized premiums changing from $240 to $3,114, a steep budget shift for many families that could trigger a benefits cliff.

As of January 1, 2024, eligibility for CHIP-funded programs will increase to 300 percent of FPL. The law also authorizes new premium tiers for families above 150 percent of FPL. The new policy requires that at least three but no more than six tiers of premiums be established for the family contribution to the health insurance program. The tiers, or family co-pay, increase as income increases in alignment with FPL up to 300 percent FPL. These changes can make a tangible financial difference for families accessing the subsidy and increase their net financial resources as earnings rise. Net financial resources are defined as income after taxes, adding in any public assistance received, minus basic household expenses.

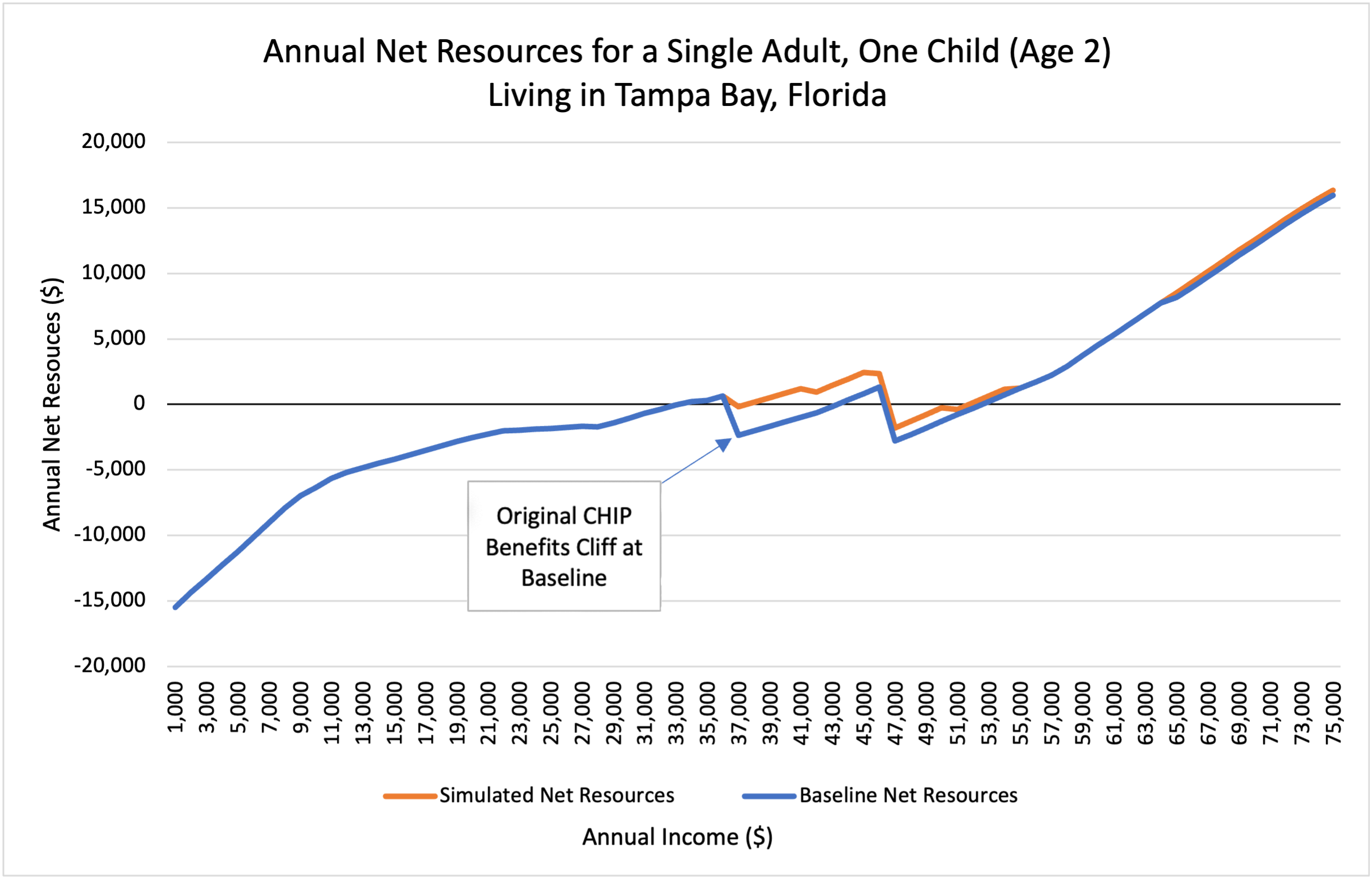

Illustrating how the change mitigates the benefits cliff

A hypothetical scenario helps illustrate the potential difference in net financial resources for families: a single parent with a 2-year-old living in Tampa, Florida, works and accesses public assistance to make financial ends meet. She receives assistance for food, housing, childcare, children's health insurance, and available tax credits. As the blue line in the figure below illustrates, if she were to lose access to children's health insurance at 200 percent of FPL (about $37,000 for a family of two) her net financial resources would decline by more than $2,600, which is a benefits cliff. The orange line shows the families' potential net resources under the new policy. With children's health insurance eligibility extended to 300 percent FPL (about $55,000), the benefits cliff caused by the loss of children's health insurance at 200 percent FPL is eliminated. The extension of eligibility to 300 percent FPL could, in theory, simply shift the benefits cliff up the income distribution. However, the figure shows how possible adjustments to the co-pay schedule near 300 percent FPL can largely smooth this benefits cliff. Rather than a sudden loss of the subsidy, the modified co-pay could gradually reduce the subsidy amount to zero, creating an "off ramp" rather than a "cliff." Once the subsidy is lost at 300 percent, the orange line equals the baseline blue line since in each scenario families are paying the same cost for the full-pay plan.

Source: Federal Reserve Bank of Atlanta Policy Rules Database and authors' calculations. Expenses are based on United For ALICE. (2023), "Household Survival Budget Methodology for Federal Reserve Bank of Atlanta Tools." UnitedForALICE.org/Methodology.

Note: The net resource values in both the baseline and simulated scenarios include the following public assistance package: Childcare and Development Fund, Child Tax Credit, Earned Income Tax Credit, Housing Choice Voucher Program (Section 8), Medicaid for Kids, and the Supplemental Nutrition Assistance Program. Estimates for public assistance received were based on 2022 public assistance rules and eligibility thresholds.

The benefits cliff that occurs in both scenarios, at approximately $46,000 in annual income, reflects the loss of eligibility to the childcare subsidy at that wage threshold and is not related to children's health insurance. However, as illustrated, the change to the children's health insurance subsidy eligibility does serve as a partial mitigant to the childcare cliff. Without the policy change, the childcare subsidy cliff results in the family falling significantly under the $0 value or break-even line for the minimum net financial resources needed to meet basic household expenses. In that situation, the family would likely face difficult budgeting decisions to make ends meet. With the policy change, the net financial resource loss still dips under the break-even line, but not to the same degree. While the childcare cliff could still present a significant financial barrier for the family budget, the household net resources are higher with the revised policy and the family is better positioned financially overall.

The hypothetical example offers only an illustration of how the new policy can mitigate benefits cliffs for a working single parent with one child. The effect of the policy change on benefits cliffs will differ across families, depending on the public assistance programs they receive, their family composition, their county of residence, expenses, and other factors. It is outside the scope of this analysis to examine the policy's hypothetical impact on all Florida families. Rather, our intent is to provide a simplified illustration of how forthcoming changes to eligibility and co-pay schedules can mitigate benefits cliffs and increase families' net financial resources.

Note: To support the implementation of the new policy change, the Florida legislature included $20.6 million in the 2023-24 General Appropriations Act.

By Brittany Birken, director and principal adviser in Community and Economic Development, Austin McTier, economic research analyst in Research, Alexander Ruder, director and principal adviser in Community and Economic Development, and Alvaro Sánchez, senior research analyst in Community and Economic Development. Sanchez and McTier provided the analysis for the article. Birken, Ruder, Sanchez, and McTier are with the Atlanta Fed's Advancing Careers Initiative. The views expressed here are the authors' and not necessarily those of the Federal Reserve Bank of Atlanta or the Federal Reserve System.