A message from Federal Reserve Bank of Atlanta president and CEO Raphael Bostic

The Federal Reserve Bank of Atlanta is deeply concerned about the COVID-19 pandemic and its profound effects on the health and well-being of our staff and the citizens of the communities we serve. But even amid this global pandemic, business continues to be transacted.

This is why we remain committed to serving the American people by continuing to do the job Congress gave us—promoting maximum employment and stable prices, and protecting the stability of the financial system.

A key part of our mission is ensuring that the nation's payments system is accessible, safe, and efficient. As part of this, we work to understand the profound changes technology is bringing to our payments networks. Expanded computing power and communications capabilities are fueling an explosion in financial technology, or fintech. Recent years have witnessed the introduction of thousands of apps allowing consumers to make payments and manage their personal finances.

These new payment options offer unprecedented convenience, to be sure. But they also raise new concerns about the safety of our payments and personal data. To better understand and mitigate those concerns, the Atlanta Fed adopted promoting safer payments innovation as a top strategic priority.

Our 2019 annual report will explain the safer payments innovation strategic priority. We believe the Atlanta Fed is uniquely positioned to tackle this issue. As home to the Federal Reserve System's Retail Payments Office, the Atlanta Fed houses the largest assemblage of retail payments expertise in the Fed System.

I believe this work is particularly important now. Lockdowns and concern about infection could increase the use of electronic payments in the long term, and so a deep understanding of these issues can help us make sure the payments system works for everyone.

As you hopefully stay healthy and heed the advice of public health experts, I encourage you to take a few minutes to read our 2019 annual report. Listen to the accompanying podcast. I hope you learn about our work to encourage innovation that keeps our payments system safe and accessible to everyone.

The Atlanta Fed aims to balance innovation and safety

Atlanta Fed president Raphael Bostic often says that if the nation's payments system were to crash even for an hour, it would be a big problem for the Federal Reserve.

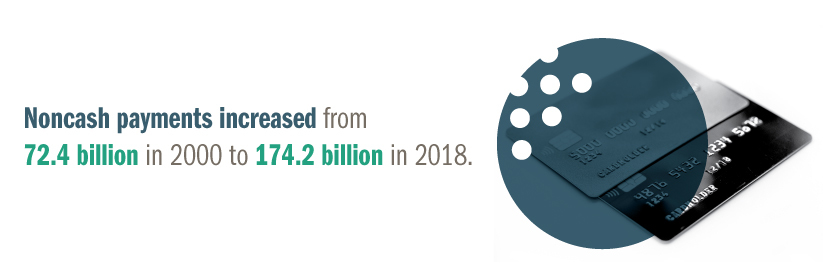

Would it ever. Consider that every hour, people in the United States make on average about $11 billion in noncash retail payments. That's from nearly 400,000 retail transactions a minute, according to the 2019 Federal Reserve Payments Study.![]() Driven mainly by debit and credit card purchases, the number of noncash payments in 2018 rose by 22 percent in just three years.

Driven mainly by debit and credit card purchases, the number of noncash payments in 2018 rose by 22 percent in just three years.

A secure, efficient, and effective payment and settlement system is vital to the U.S. economy, and the Federal Reserve plays an important role in helping maintain its integrity. While the underlying "rails" that carry vast loads of electronic payment information have been in place since the 1970s, the number of entryways to those rails has soared with the proliferation of financial technology, or fintech. And each new doorway to the payments system is a new opportunity for fraud.

In 2019, the Federal Reserve Bank of Atlanta launched a multipronged strategic priority aimed at helping to balance innovation and safety. This initiative—balancing innovation and security—encompasses business units across the Atlanta Fed.

In collaboration with the payments industry, the Atlanta Fed aims to:

- safeguard consumers and the payments system amid rapid innovation

- understand the fintech landscape and emerging technologies most likely to affect the payments ecosystem and the new risks these innovations present

- engage with stakeholders to gather and share knowledge

- experiment with emerging financial technology to solve the Bank's own business problems

We explore below how the Atlanta Fed plans to achieve these goals.

Why the Atlanta Fed?

First, though, why is the Atlanta Fed in particular trying to foster safer innovation in the payments industry? There are several reasons, but a couple stand out.

For one, the Atlanta Fed is home to the Federal Reserve System's Retail Payments Office. The Retail Payments Office not only operates two major payments networks—the Fed Automated Clearinghouse (FedACH), which handles direct deposits among other payments, and Check Services, which processes the nation's checks—but it also guards the safety and efficiency of the nation's broader payments ecosystem. Thus, the Atlanta Fed houses the largest collection of retail payments expertise in the Federal Reserve System.

Second, metropolitan Atlanta is a hub of the payments processing industry. Some two-thirds of payments processed in the United States pass through wires and computers operated by companies in Georgia, according to the Technology Association of Georgia, earning the metro area the nickname Transaction Alley.

"There is a nexus that makes it imperative for us to be in this space," said André Anderson, first vice president and chief operating officer of the Atlanta Fed and head of the RPO. "This is an area where we can make a real difference."

An influx of fintech firms is rapidly altering the payments ecosystem. This ecosystem comprises the FedACH and its rival, the Clearinghouse, major card processing networks, hundreds of payment processors, thousands of financial institutions and merchants, and an abundance of apps and other consumer payment services.

To be sure, the surge in electronic payments coursing through that system has been driven in the very recent past in part by economic and population growth. The coronavirus pandemic has also changed people's behavior. Many people are now buying more stuff online or through contactless applications on their phones. And the explosion of fintech services that allow consumers to move funds with an app is also fueling the surge, noted Mary Kepler, senior vice president and head of the Atlanta Fed's Retail Payments Risk Forum.

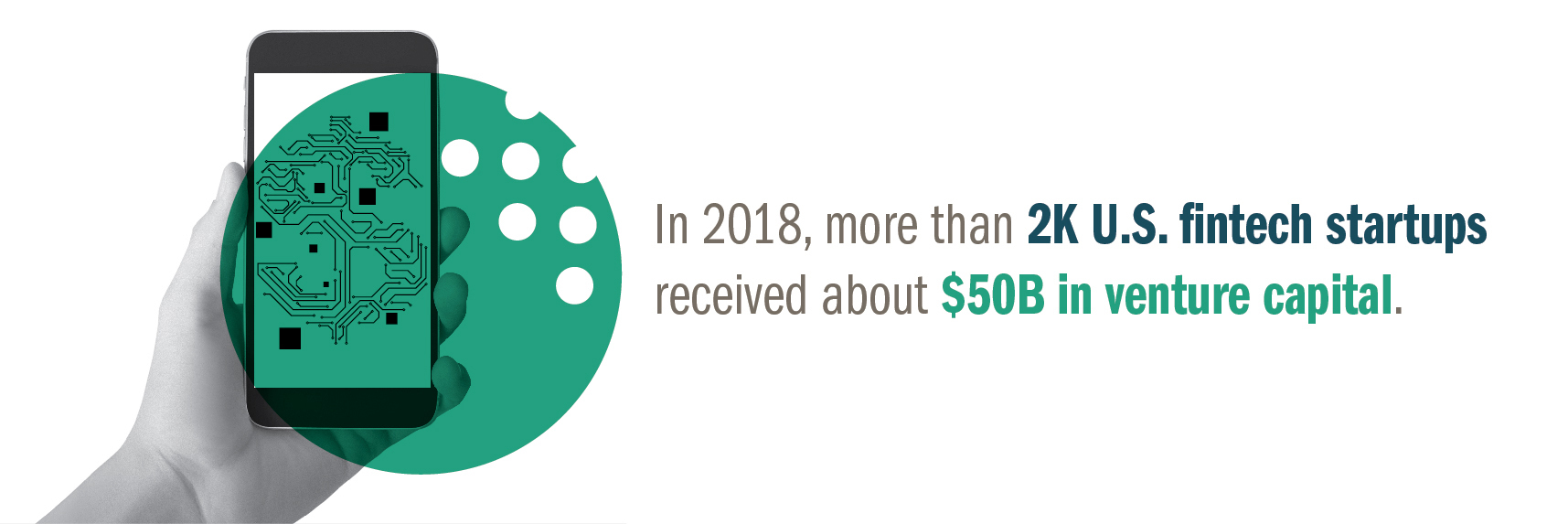

Thousands of fintech products have debuted in recent years, from widely used products like PayPal and Venmo to offerings from firms with five employees. In 2018 alone, more than 2,000 U.S. fintech startups combined to attract roughly $50 billion in venture capital, according to CB Insights, a technology industry analytics firm. Georgia by itself is home to about 170 fintech firms of various sizes, according to the Technology Association.

Many of these companies offer services consumers use on the more than 250 million smartphones in use in the United States. For all the convenience the devices offer, each is also an opening for potential fraud that did not exist a decade or so ago.

"They all attach to the payments system in one way or another," Kepler said of fintech products. "That broadens the landscape for payments, and it broadens the openings for fraud. So we have an obligation to do what we can to influence safer practices. This seems especially important right now given the growth in electronic payments during the coronavirus pandemic."

What the Atlanta Fed is doing

What is the Atlanta Fed doing to promote safer payments innovation?

Much of the work focuses on relationships and research. A third focus involves experimenting with new technologies to solve internal business problems.

Start with relationships. The Atlanta Fed is cultivating ties with the University System of Georgia and the payments and fintech community in the Southeast. The Reserve Bank is offering its regulatory and payments security expertise to help the university system craft a fintech-focused curriculum for a new fintech academy, as well as for traditional colleges and technical schools.

The key there, Kepler said, is to help ensure an adequate talent pool for fintech firms and for the Fed, too. Through much of the recovery from the Great Recession, companies in various businesses consistently reported trouble finding and keeping technical employees such as software developers and engineers.

Meanwhile, the Atlanta Fed and the Fed System are exchanging knowledge and building ties with fintech firms and banks that partner with fintechs. The mission: to influence the direction of innovation so that firms are more likely to incorporate security early in the development process.

Many fintech firms are small and lack in-house expertise in payment and data security and regulatory affairs. Therefore, balancing speedy development of apps with sound security and regulatory compliance can be a quandary for young companies without deep pockets.

Take Qoins, an Atlanta-based startup with five employees whose financial wellness app has helped users pay off more than $11 million in debt since 2017. The company had an early stumble navigating regulations that govern how firms set up accounts to handle customers' funds. The issue prompted Qoins to hire an experienced compliance officer, a significant financial commitment, said Christian Zimmerman, the company's founder and CEO.

Zimmerman visited the Atlanta Fed for the Federal Reserve System's inaugural "innovation office hours" event. A couple dozen fintech entrepreneurs and bankers who work with fintechs discussed payments security, regulation, financial inclusion, and other matters with experts from the Atlanta Fed and the Fed Board of Governors. These sessions are part of the Fed's effort to establish relationships with the fintech industry and promote safe innovation.

Sheena Allen also came to "innovation office hours" and described it as more of a back-and-forth conversation than she expected. Founder and CEO of Atlanta-based CapWay, which makes a mobile banking and financial education app, Allen said the discussion centered on financial inclusion and data security.

Assembling people for substantive conversation is a core Fed duty, in payments and other policy areas. As Cheryl Venable, executive vice president and RPO product manager, said at the office hours event, "We don't have all the answers, but when we convene inclusive groups of parties involved with the issues, the right answers often reveal themselves."

Financial inclusion and payments innovation

Turning to research, the Atlanta Fed's Retail Payments Risk Forum and economic researchers are exploring the financial inclusion implications of payments and fintech advances. This work combines the Bank's safer payments innovation priority with another strategic focus—improving economic mobility and resilience, particularly for those born into poverty.

Bostic has noted that some digital payment services effectively limit financial inclusion by locking out people who use cash. In a recent paper, Atlanta Fed research economist Oz Shy reported that lower-income people are less likely than the larger population to hold debit or credit cards. And without the option to use cash, they can find their access to goods and services constrained.

Yet while technology can limit financial inclusion, it can also expand it. Technology can fundamentally ease access to the financial system, making payments more efficient, easier, and cheaper. So the circumstances enabled by fintech give rise to a new notion of financial inclusion that might encompass two elements.

One element of a new approach to financial inclusion is "to make sure nobody's excluded by how we do things," Bostic said.

Broad access to the payments system is critical to helping people, particularly low- to moderate-income individuals, avoid predatory financing entanglements, said Mike Johnson, executive vice president of the Supervision, Regulation, and Credit Division at the Atlanta Fed. Johnson's division plays a role in these matters in part by helping banks meet their obligations under the Community Reinvestment Act, or CRA. Enacted by Congress in 1977, the CRA is designed to encourage depository institutions to help meet the credit needs of their communities, including economically distressed neighborhoods, consistent with safe and sound operations.

The economic effects of the shelter-in-place protocols implemented to protect communities from the proliferation of COVID-19 make safe and sound credit flow to distressed neighborhoods and small businesses even more critical.

A second element is that the very definition of exclusion merits rethinking in today's marketplace, Kepler said. She noted that the traditional formulation of financial inclusion as simply moving people without bank accounts into the mainstream banking system might be obsolete when people can use smartphone apps to manage personal finances without a traditional bank account. Staff in the Risk Forum have begun work on a research paper meant to spur conversation and further research on redefining financial inclusion.

Payments innovation nothing new for the Fed

The pursuit of safer payments innovation is timely but not new for the Fed. Central bankers and other policymakers have long sought to help balance financial innovation and the safe, efficient operation of the financial and payments system.

Indeed, before Congress established the Federal Reserve in 1913, check clearing fees—and banks' efforts to avoid them—often led to circuitous check routing, resulting in people and firms facing long, unpredictable delays in receiving their money. When they did eventually get funds, fees had often sliced off a chunk.

In extreme instances, the contortions banks used to avoid clearing fees led to checks moving from city to city before eventually landing at their destination. Those inefficiencies were one of the reasons the Congress created the Federal Reserve. In its earliest days, the Fed helped to halve the average time it took to clear checks from 5.3 days in 1912 to 2.4 days six years later, according to research by Atlanta Fed economist Will Roberds ![]() and others.

and others.

More recently, the Fed played a major role in digitizing the processing of paper checks. For several days after the September 2001 terrorist attacks, the nation's airplanes were grounded, preventing paper checks worth billions of dollars from moving across the country for settlement.

That disruption of the payments routine heightened the urgency to automate the check handling system. In response, Fed officials in Atlanta and elsewhere helped shape the Check Clearing for the 21st Century Act, which was enacted in 2003 and took effect in 2004. Also known as Check 21, the law allows a properly prepared substitute check—a copy of an original paper check—to hold the legal equivalence of that original paper check. This change enabled banks to handle more checks electronically, making check processing faster and more efficient. As the number of paper checks written rapidly declined since 2004, the Federal Reserve shrank its paper check processing apparatus from 45 facilities to only one, saving costs and streamlining the payments system.

Then in 2016, the Fed helped to introduce same-day ACH processing. This allowed transactions such as direct paycheck deposits, retail payments, and vendor payments to clear and settle the day they are initiated, allowing recipients quicker access to their money.

Another innovation is coming soon in the form of FedNow. FedNow is the Federal Reserve System's new round-the-clock real-time payment and settlement service. The service will be available in 2023 or 2024, allowing financial institutions of every size, in every community across America, to provide safe and efficient instant payment services.

In addition, the Atlanta Fed is evaluating ways to employ fintech to serve the public and financial institutions that use its payment services. The RPO is studying artificial intelligence, machine learning, and distributed ledger technology to, for example, help pinpoint transactions that might be fraudulent.

While the Fed has always monitored technological developments in payments, the RPO is more purposefully approaching outside groups such as fintech and other technology firms. A key in the Fed's adapting to technological evolution is to ensure that the rules for payments fit the new processes, said Nell Campbell-Drake, vice president in the RPO. The Fed has long played a pivotal role in shaping the adoption of payments technology. Of course, the payments system has evolved enormously since the early 1900s, alongside improvements in communications and computing technologies. Today, payments are one of the most important areas of innovation in the broad universe of fintech. The Fed will continue to play a role, as it has for more than a century.