National affordability

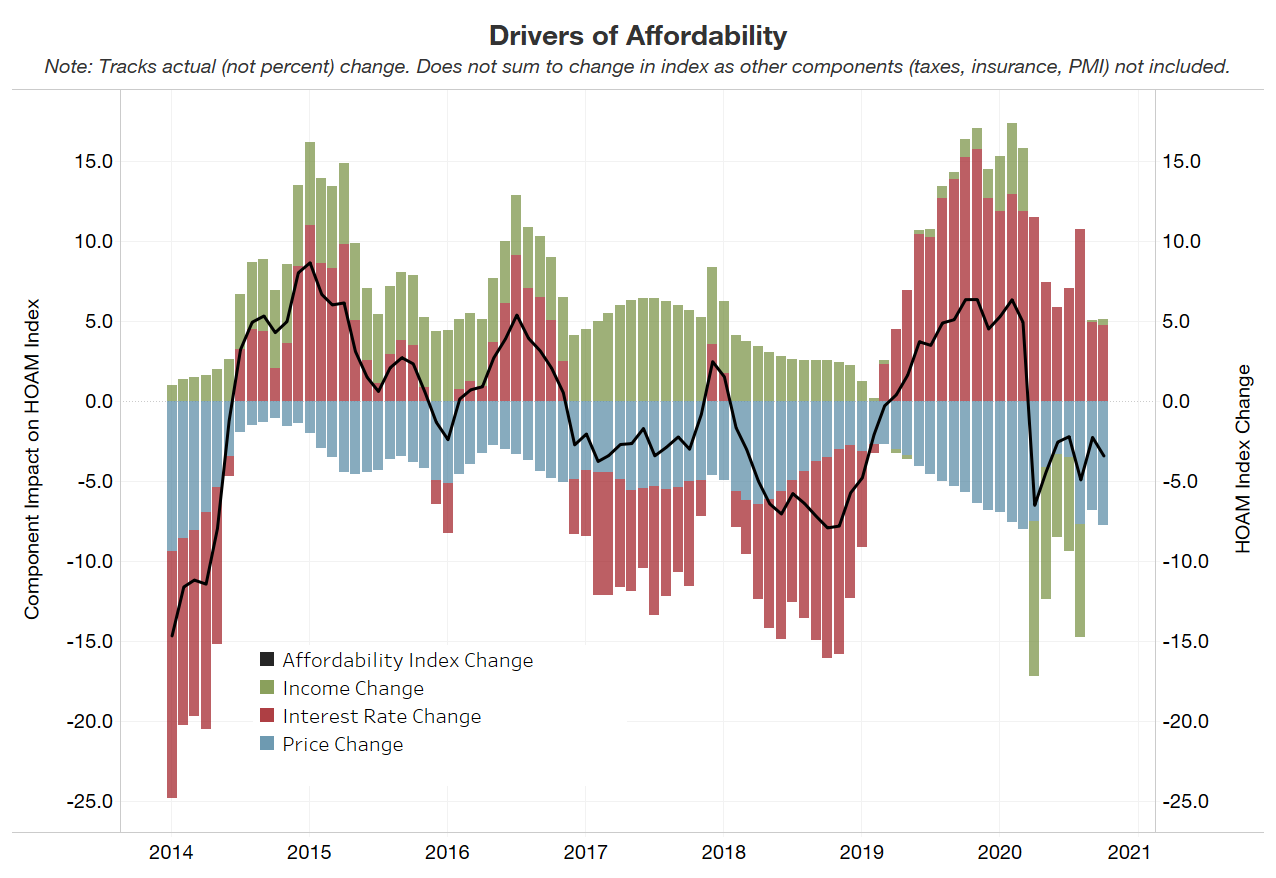

Higher prices continued to make owning a home less affordable in the United States during October 2020, according to the Federal Reserve Bank of Atlanta’s Home Ownership Affordability Monitor (HOAM) index. Despite historically low interest rates, a spike in house prices as well as the strain on household incomes created by the COVID-19 recession continued to box the average income household out of owning a home.

A HOAM index below 100 indicates that the median-priced home is unaffordable to the median-income household given the current interest rate. In October, the HOAM index dropped to 93.4 from a revised 94.8 in September, indicating that the median-priced home remained too expensive for the median-income household. The HOAM index was also below its 100.52 reading a year earlier. Home ownership costs in October (as measured by principal and interest, taxes, and insurance) accounted for 32.1 percent of the annual median income of U.S. households, which is above the 30 percent affordability threshold set by the U.S. Department of Housing and Urban Development. October marked the seventh month in a row that the national HOAM index was below 100.

Declining interest rates remain a positive for home ownership affordability. The 30-year fixed mortgage interest rate ended the month of October at 2.8 percent, a drop of six basis points (bp) from September and an 86 bp decline from October 2019. However, the strain on household incomes and steadily rising prices have been more than enough to offset any positive effects on home ownership affordability from lower rates. With the COVID-19 pandemic still weighing on the economy, the estimated median household income in the United States in October ($59,532) was down 5.4 percent from a year earlier. Meanwhile, the national median existing home price (three-month moving average) rose to $300,002 in October, up 2.6 percent to from a revised $292,502 for September. However, compared with a year ago, home prices were up a sharp 12.2 percent in October. Prolonged inventory shortages in many markets are exerting steady upward pressure on home prices, which continue to reach record levels.

Regional affordability

Just over 22 percent of metro areas in the United States had a HOAM index below 100 in October, indicating that they were unaffordable to median-income households. By contrast, 78 percent had an index above 100 and were considered affordable. Even so, 57 percent of metro areas experienced a decline in affordability from September to October as rising home prices and lower incomes took their toll. In general, high-cost metro areas on the West Coast as well as in the Northeast and South Florida were among the least affordable, while metros in the middle of the country, particularly in the Midwest, tended to be the most affordable.

Among the nation’s largest metro areas (those with populations greater than 500,000), San Jose-Sunnyvale-Santa Clara, California, was the most expensive in October with a median existing home price of $1.19 million. The median price in San Jose rose 15 percent from October 2019. Meanwhile, San Francisco-Oakland-Hayward, California, was the nation’s least affordable large metro in October with a HOAM index of 55.3. Even though homes in San Jose were more expensive, household incomes there were generally higher than in San Francisco ($131,218 for San Jose compared with $113,918 in San Francisco), making San Jose slightly more affordable.

With a median existing home price of $1.18 million, the annual share of income needed to own a home in San Francisco was 57 percent, the highest home ownership cost among large metros and well above the 30 percent that is considered affordable. Still, rising home prices continue to be somewhat offset by falling interest rates and stable household incomes, which led to a modest improvement in overall home ownership affordability in San Francisco compared with the previous month.

The least expensive large metro area in October was Youngstown, Ohio, where the median sales price was $141,000. Home prices there rose 4.9 percent over the past year. Youngstown also remained the most affordable large metro in the nation in October with a HOAM index of 155.8. The area’s estimated median household income in October was $48,996, and, on average, households there spent 19 percent of their annual earnings on housing. This percentage represents the lowest home ownership cost among large metros. Despite rising home prices, lower interest rates helped to keep home ownership affordability relatively high in Youngstown.

With a median existing home price of $830,063, a median household income of $89,413, and a HOAM index of 53.0, Santa Cruz-Watsonville, California, was both the most expensive and least affordable small metro area in the United States (metros with populations below 500,000) in October. On average, households in Santa Cruz spent 57 percent of their incomes on housing. Meanwhile, the least expensive small metro during the month was Danville, Illinois, where the median existing home price came to $97,438 in October. Kokomo, Indiana, remained the most affordable small metro with a HOAM index of 191.5. Its median home value was $152,797, and its median household income was $57,642. Households in the region only spend 15.2 percent of their income on housing, on average.

In metro areas with populations above 500,000, Spokane, Washington; St. Louis, Missouri; and Pittsburgh, Pennsylvania, had the greatest improvement in affordability from September to October. In Spokane, affordability rose by 9.4 percent from September to October, while affordability in St. Louis and Pittsburgh rose by 5.8 percent and 3 percent, respectively. Home prices in all three metro areas declined sharply from September to October, although they were higher on a year-over-year basis. These price drops, combined with declining interest rates, aided home ownership affordability in these regions.

Meanwhile, the metro areas of New York, New York; Cape Coral, Florida; and North Point-Sarasota-Bradenton, Florida, saw the sharpest falloff in home ownership affordability. Although modest—1.76 percent, 1.75 percent, and 1.74 percent, respectively, from September to October—the declines in affordability in these regions was driven by rising home prices, as values rose more than 3 percent in all three regions. For example, the median home price in New York climbed by 3.4 percent from September to October. The increase in home prices was more than enough to offset the positive effects of lower interest rates, creating a drag on affordability.

COVID-19’s impact

Despite the decline in overall affordability, demand for housing remains exceedingly strong, as relatively low interest rates continue to fuel home sales. Existing home sales rose 26.6 percent in October from the year earlier, offsetting any losses in annual sales experienced at the onset of the pandemic earlier this year, according to the National Association of Realtors. However, existing home inventory dropped by 19.8 percent over the same period. As such, existing home supply has not kept up with the pace of sales, and the overall supply of existing home inventory stood at a very low 2.5 months in October. Considering that a supply of four to six months is considered balanced, the market is currently seeing a significant shortage of inventory. As a result, home prices continue to climb, creating a steady hurdle for potential home buyers.

The lack of supply continues to fuel demand for residential construction, boosting optimism in the new home market. However, although sales for new homes are strong, higher lumber prices and constraints on labor have caused construction costs to rise. These factors, combined with pressure on builders to keep pace with demand, are pushing up new home prices. In the months ahead, although low interest rates will help support gains in purchasing power for many households, rising existing and new home prices are expected to continue to suppress affordability.

Finally, the number of mortgage loans in forbearance has held steady at around 5.6 percent over the past few months, according to data provided by Black Knight. Still, delinquencies remain elevated, particularly in regions that have significant exposure to industries that were hard-hit by the pandemic such as transportation and leisure and hospitality. FHA and VA mortgages tend to have higher delinquency rates compared with conventional mortgages and, according to Black Knight, a higher share of these loans remain in forbearance—9.5 percent. As forbearance programs expire in the months ahead, elevated levels of mortgage debt could raise the possibility of higher defaults, which would have a significant impact on the housing market.

For more details, including metro level analysis, please visit the interactive Home Ownership Affordability Monitor tool.

Domonic Purviance

Senior financial specialist in the Atlanta Fed's Supervision, Regulation, and Credit Division