Metro Atlanta homebuilder Piedmont Residential raised its new home prices because of higher lumber costs. One of its best-selling homes, which is pictured, is now priced in the $300,000 range, up from the low $200,000 range two years ago. Photo courtesy of Piedmont Residential

Tarla Atwell and her husband want to buy a home in a good school district in metropolitan Atlanta’s suburban Gwinnett County but can’t find one in their price range. When their agent locates a good prospect, the house already has several offers on the table by the time they arrive to tour it.

“There has not been much available, and if something is available, you have to bid over the asking price because of the competition,” said Atwell, an attorney who has been looking for at least a year. “It is frustrating, and we’re trying to exercise patience.”

Atwell’s is not an isolated story. Many consumers looking to purchase a home are finding a similar situation. Historically low interest rates, a lean supply of available homes, and skyrocketing demand have brought dramatic changes to the housing market—one of those changes being upward price pressure. With house prices climbing at double-digit percentages in the past year, it’s becoming harder for many to realize the dream of home ownership.

“With the interest rates being at all-time lows, more people are able to become homeowners,” said Shantay Williams, a real estate agent in Birmingham, Alabama. “But the most desirable homes go fast.”

Atlanta Fed expert cites structural change

Domonic Purviance, a subject matter expert in the Atlanta Fed’s Supervision, Regulation, and Credit Division, attributes the current supply shortage to structural changes in the housing market. Fewer homes have been built since the Great Recession, and now, “so many people have refinanced their mortgages and locked into low rates, and there’s a disincentive for them to sell,” Purviance said.

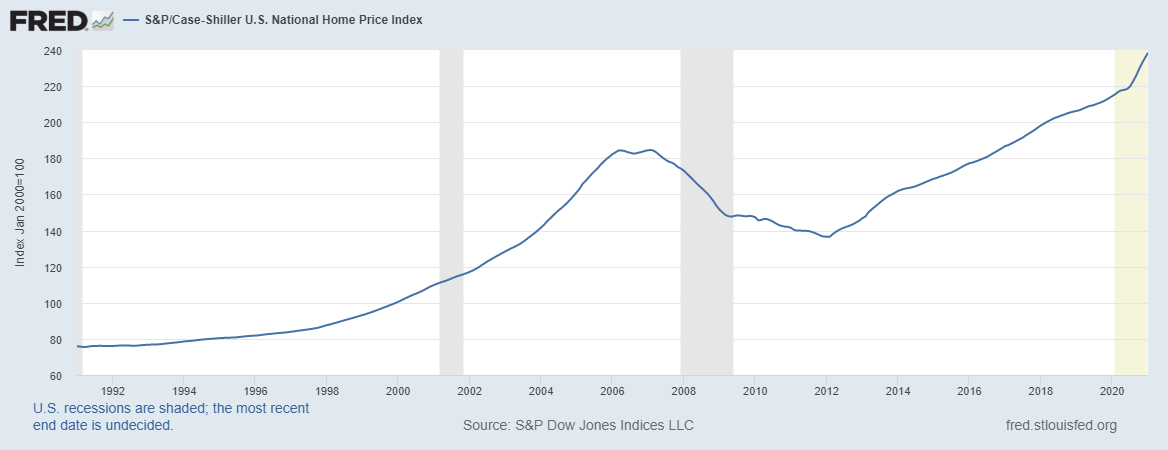

Other factors are also hindering people like Atwell and her husband in their home searches: the COVID-19 pandemic has fueled a desire for more spacious homes and millennials are beginning to exert their influence on homebuying (see the chart). “The confluence of all these factors together makes this upward trend in the housing cycle very unique,” Purviance said.

Last year, Purviance and other researchers at the Atlanta Fed unveiled the Home Ownership Affordability Monitor (HOAM) index, an interactive tool that measures the ability of a median-income household to manage the costs of owning a median-price home in a given metropolitan area. The index shows that houses in the six states of the Atlanta Fed’s coverage area—Alabama, Florida, Georgia, Louisiana, Mississippi, and Tennessee—are mostly affordable. Still, Purviance cautions that house affordability is declining in pockets of major Southeast metros because of home-price growth.

The Atlanta Fed’s Domonic Purviance. Photo by David Fine

“Atlanta, for instance, is one of those markets where you can find an affordable place to live if you are willing to drive farther out,” Purviance said. “But in the close-in markets where people want to work and send their kids to school—not so much.” The HOAM index shows that the least affordable metropolitan areas in the Southeast are in South Florida, including Miami, Fort Lauderdale, and West Palm Beach.

‘Crazy’ demand and activity

Against this backdrop, home builders are selling houses as fast as they can construct them. “The demand has been absolutely crazy,” said J.D. España, president of Piedmont Residential, a Woodstock, Georgia, construction company that builds in metro Atlanta.

España said that 2020 marked one of the company’s best financial performances since it began business in 2007, and sales this year are poised to exceed projections. Although families looking for homes account for the majority of buyers at his company, España also noted that sales have gotten a boost from investors seeking rental houses.

Williams, who has been a real estate agent since 2015, also uses the word “crazy” to describe the activity she sees in facilitating deals between home buyers and sellers. In the current market, even houses that need a good bit of repair are garnering elevated prices. Many sellers are holding out for multiple offers, and some are asking buyers to pay thousands above asking price to complete a sales contract, even if the property does not appraise for the higher amount, Williams added. “Many sellers are taking advantage of the opportunity to get top dollar for their houses,” she said.

New home prices also go up, up, up

These days, the median value for an existing home in the United States is about $315,000, and $340,000 for a newly built house, Purviance said. Although the typical effects of scarcity on price are partly at work, higher costs for materials such as drywall, cabinets, and particularly lumber are also fueling the increase.

“We wouldn’t have the price appreciation that we’re seeing right now if it weren’t for lumber,” España said, noting that the lumber package for the typical 2,000-square-foot house his company builds has more than doubled in the past year, rising to $18,000 from $6,700. The average price of that same home has ticked up to around $300,000 from the lower $200,000 range two years ago, he added.

España is concerned that rising home prices will shut out the median-income buyers his company caters to and is carefully watching materials costs. “As home prices go up, you’re pulling people out of the market,” España said. “So the base of buyers gets smaller.”

Similarly, Purviance is keeping a watchful eye on mortgage rates. The 30-year fixed rate fell below 3 percent last summer but has been rising above that level since the end of February. “Low interest rates have undergirded this market,” Purviance said. “If they start to go up, demand will dry up pretty quickly.”

Karen Jacobs

Staff writer for Economy Matters