Small Businesses Meet Big Dreams: Entrepreneurs Stride Varied Paths toward Goals

Across the Southeast, the small business landscape is a tapestry of different stories that tell different experiences.

Businesses with fewer than 500 employees entered 2019 with the tailwind of a strong 2018, as consumer spending picked up, corporate profits climbed, and the U.S. economy grew nearly 3 percent, as measured by gross domestic product. Against this favorable backdrop, 72 percent of small firms that responded to the Federal Reserve's Small Business Credit Survey in 2018 cited optimism that revenue would increase in 2019. Enthusiasm for entrepreneurship appears to be building, with business applications ticking up in recent years, according to U.S. Census Bureau statistics.

At the same time, challenges are visible. A tight labor market means that finding qualified workers has become difficult for companies across the Federal Reserve Bank of Atlanta's coverage area, which includes the states of Georgia, Alabama, and Florida and parts of Louisiana, Mississippi, and Tennessee. Many small businesses are hard pressed to manage their cash flow. Rising overhead (including health care costs) poses hurdles, as does regulatory compliance. Federal Reserve reports show that firms owned by minorities and companies in which the business owners are the sole workers have a hard time obtaining loans and turning a profit.

Although some small companies are optimistic and look to expand next year, others are less certain about the future. Concerns about the prolonged economic effect of trade and political disputes are tempering some businesses' optimism.

Tariffs are "not helping us," said Jamie van den Bergh, chief executive of Clarity Products LLC in Chattanooga, Tennessee. The company designs amplified telephones, alarm clocks, and other alerting devices for elderly and deaf people. In the wake of recent tariff disputes between the United States and China, Clarity has had to pay a 15 percent tariff on those products.

"We've had to pass most of that cost on to our customers, and we think that will have some impact on demand," van den Bergh said. While he hopes a resolution to the dispute will end the tariffs, he is also concerned things could get worse. "I'm worried about the tariff going from 15 to 25 percent, which would be really problematic for us," he said.

Challenges accompany a healthy labor market

To be sure, low unemployment has produced economic advantages. But it has also brought difficulties for small business owners. Jeff Patterson, who is responsible for lender relations and economic development at the Georgia office of the Small Business Administration, said finding qualified staff is perhaps the biggest problem small firms face today. "The number one thing we hear as an obstacle is businesses can't find good people to come to work, and that's everybody from the worker on the floor to C suite–level people," he said.

To address this issue, companies have beefed up training to existing employees, cast a wider net in searches for workers, relaxed job requirements, and raised pay, even for lower-skilled workers. But in an era of less than 4 percent national unemployment, none of those actions are silver bullets.

Some sectors seem to be having a harder time filling positions than others. In the Southeast, manufacturing and service industries have been particularly hard hit by the shortage of qualified labor. Van den Bergh said two people left his company in the last four months for better opportunities elsewhere.

The shortage of service industry workers is especially acute in urban markets such as Nashville, Memphis, and Birmingham, said Clint Gwin, president of Pathway Lending, a community development financial institution (CDFI) that provides financing to small businesses in Tennessee and Alabama.

"If you're in the restaurant business and you need a dishwasher, you used to be able to pay $8 to $11 an hour," Gwin said. "Now, you're paying $18 to $19 an hour, and you hope they show up to work." Businesses such as restaurants, entertainment venues, even dry cleaners are struggling to retain employees at a pay level that is sustainable, Gwin added.

Bobby Holland, owner of Holland's Paint & Body in Robertsdale, Alabama, has added three people to his staff over the last four years and now employs eight. He said he would like to hire another person to reduce the shop's backlog, but he acknowledges the challenge in finding people trained in auto body and vehicle repair—skills in high demand. "Most skilled technicians are already making top pay," Holland said.

Owner Bobby Holland employs eight people at his auto body shop in Robertsdale, Alabama. His shop is decorated with some vintage touches. Photo courtesy of United Bank

Owner Bobby Holland employs eight people at his auto body shop in Robertsdale, Alabama. His shop is decorated with some vintage touches. Photo courtesy of United BankFed reports show mixed picture across firm types

Federal Reserve reports published this year show mixed results across the small business universe on a number of measures.

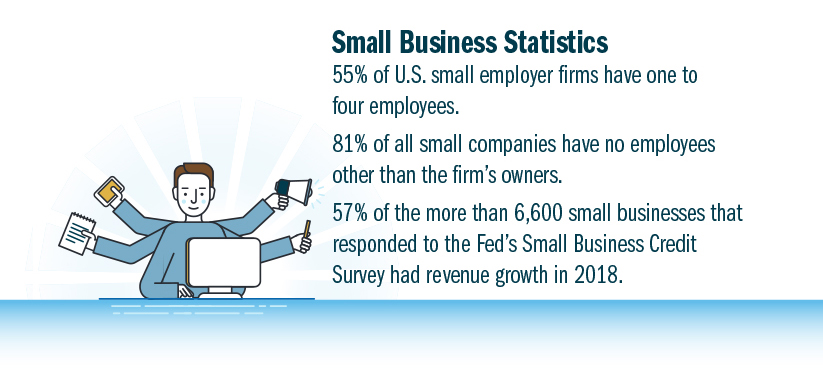

Among respondents to the Fed's Small Business Credit Survey, 57 percent of firms saw revenue growth last year, and 43 percent of firms applied for new capital. But the picture is not rosy for all companies. Businesses with no workers other than the firms' owners, known as nonemployer firms, are not faring as well as their larger counterparts, as data show that 55 percent of these companies either produced no profits or just broke even during 2017. Additionally, racial disparities in access to funding continue to be an issue: an analysis of the Federal Reserve credit survey findings shows small businesses owned by Blacks are less likely to be approved for financing than are White-owned firms.

Firms that have no employees besides the business owners represent 81 percent of all small businesses, a summer 2019 report from the Fed notes. The ranks of these businesses came to more than 25.7 million in 2017, up about 66 percent from 1997, according to Census Bureau statistics.

The Fed's report found that nearly two-thirds of nonemployer firms are the main source of income for their owners but face tough times acquiring capital, as more than half of them have financing shortfalls. One in five of these companies came into existence because the owner lacked other employment options. Among these companies, African American– and Hispanic-owned firms reported the largest funding gaps and were much more likely to be operating at a loss than at a profit.

Although the ranks of the self-employed have grown in recent years, many are finding that entrepreneurship is not easy, Patterson said. The Small Business Administration offers workshops to educate potential business owners on the nuts and bolts of running a company. "There are a lot of questions we ask the entrepreneurs," Patterson said. "One of those things is, ‘Can you maintain your lifestyle?' It's hard to do, and a lot of them aren't doing so well," he said.

Minority-owned firms face financing headwinds

The problems faced by minority businesses are significant because these firms can be an important vehicle of employment and wealth creation for their communities, said Mels de Zeeuw, a senior research analyst in the Atlanta Fed's Community and Economic Development Department.

He has cowritten a report that discusses differences in the financing experiences of minority- and White-owned firms. His analysis of Fed small business credit survey data found White-owned firms were more likely to be approved for bank loans than black-owned firms. The report also noted that Asian-, Black-, and Hispanic-owned businesses were more likely than White-owned ones to report not having sufficient levels of financing in general. Black-owned companies in particular have a harder time, with a smaller share attaining profitability compared with White-owned firms.

"If we value economic outcomes in certain communities and equal outcomes for Whites and minorities, then we should want to make sure that access to capital is the same regardless of the race or ethnicity of a firm's ownership," de Zeeuw said.

Because of the connection between small business ownership and community wealth building, minority firms' struggle to thrive can help explain different economic outcomes in White and minority communities.

"There is a link between race and ethnicity in terms of firms' ownership and their hiring policies, so Black-owned firms on average tend to hire more Blacks," de Zeeuw added. "Having a greater share of employer firms that are owned by minorities can go a long way toward decreasing disparities in unemployment between Whites and minorities."

Though the Fed report doesn't delve into the causes of disparities in financing for minority and White-owned small businesses, de Zeeuw noted that minority-owned firms tend to lack networks and relationships with small banks that could help in the loan approval process.

De Zeeuw's analysis found that some minority business owners have had better luck securing financing from nontraditional lenders such as online banks and community development financial institutions, or CDFIs. For instance, 17 percent of Black-owned companies that apply for credit turned to a CDFI, compared with 5 percent of White-owned firms, the Fed data showed.

John Kimbrough, an Atlanta-area business owner, knows firsthand the difference support from a CDFI can make for a small firm. These institutions, which can include credit unions, venture capital funds, and banks, partner with government and other entities to meet the financial needs of underserved markets.

Kimbrough and his wife, Juanisa, operated a daycare in their home for nearly five years, initially providing services for six preschool children and two after-schoolers. Eventually, they moved to another building and paid more than $4,000 a month in rent. Looking to buy their own business property, the couple applied for a loan at a bank with which they had a 20-year relationship. The bank wanted documentation of $250,000 in revenue, and the Kimbroughs verified $219,000. Their loan application was denied.

Co-owner Juanisa Kimbrough accompanies children during recreational activities at Ms. Niecy's Home Away from Home Learning Center. Photo courtesy of Access to Capital for Entrepreneurs

Co-owner Juanisa Kimbrough accompanies children during recreational activities at Ms. Niecy's Home Away from Home Learning Center. Photo courtesy of Access to Capital for EntrepreneursA friend suggested they approach community development investors, so the Kimbroughs applied to Access to Capital for Entrepreneurs (ACE), a Georgia-based CDFI. ACE examined the daycare's books and other information and approved a loan that allowed the Kimbroughs to acquire the property that is now home to Ms. Niecy's Home Away from Home Learning Center.

"Without ACE, we would not have grown," John Kimbrough said. "ACE looked at us differently" than the bank. To date, ACE has made three loans to the Kimbroughs, allowing them to acquire additional buildings. Their learning center now accommodates 160 children. "In six years, we have bought three properties and grown the business tremendously," Kimbrough said.

The growth has enabled the Kimbroughs to have a positive effect on the community by providing a needed service and jobs to at least 18 people. "We have six or seven employees that live in this area. They're able to help their families," Kimbrough said.

To be sure, the boost given by CDFIs helps entrepreneurs make their ideas flourish, as ACE did for the Kimbroughs. And while CDFIs provide important financial help, it's still the entrepreneurs who provide the vision, the drive, and the elbow grease that always undergird small business success stories.

"Entrepreneurs are great fighters," said Gwin. "They are very determined to be successful and to get to the other side."

Karen Jacobs

Staff writer for Economy Matters