Last month, we noted that employers expect working from home to triple after the pandemic as compared to the prepandemic situation. The large shift to working from home has prompted many to speculate about the demise of commercial real estate (CRE) and the demand for office space.

We also wonder what will happen. So, in our latest Survey of Business Uncertainty (SBU)—fielded from June 8 to 19—we asked firms this question: "After the coronavirus pandemic is over, how do you anticipate your firm's floor space needs will have changed, if at all?"

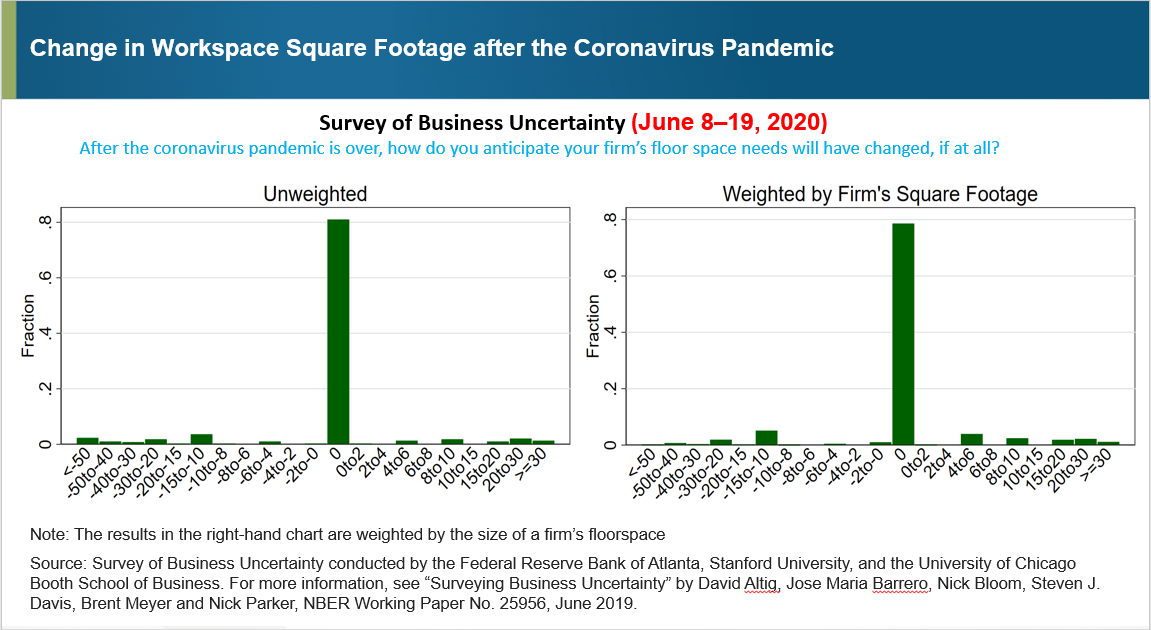

Before we dig into the results shown in the chart, we want to note a couple important caveats. First, we survey only continuing firms. Firms that went out of business in the wake of the pandemic aren't around to answer our survey questions, and we don't capture the reduction in their floor space needs. On the flip side, new firms aren't part of our sample frame, so we miss their new demands for space. Second, our survey yields data at the level of firms and not at the level of individual business facilities. For example, if the pandemic prompts a firm to shift its office workers from a high-rise building in the city center to a low-rise suburban office park with the same square footage, such a change is not captured by our survey.

As the chart shows, roughly 80 percent of our 390 respondents anticipate no change to their current floor space needs. Responses from the other 20 percent are highly dispersed, leading to long-tailed distributions. Some of the firms in our sample expect to either reduce or expand floor space by a third or more.

Although firms in our sample don't anticipate their overall square footage to change much, exactly how much change they expect depends on how we weight the sample responses. When we weight by firm size as measured by number of employees, overall demand for floor space is expected to shrink by 2.8 percent (with a standard error of 0.7 percent). When we weight by the firm's current floor space usage, overall demand for floor space is expected to rise by 0.4 percent (with a standard error of 0.6 percent). Either way, the expected change in the overall demand for commercial real estate is quite modest.

If we focus on firms in business services, information, finance, and insurance—industries that dominate the demand for office space—and weight by current floor space, we obtain an expected increase of 1.6 percent (with a standard error of 0.9 percent). One possible interpretation of these results is that new desires for social distancing will offset the impact of greater working from home on the overall demand for office space and CRE more generally.

While overall floor space needs aren’t expected to change materially, the long tails in chart 1 imply some reallocation of workspace across firms—that is, footprints will expand for some firms and shrink for others. To quantify this reallocation, we compute two quantities: the extra floorspace needed by firms that expect to expand their footprints, and the reduction in floorspace for firms that expect to shrink their footprints. Taking the minimum of these two quantities, we find that 1.7 percent of floor space will be reallocated across firms, according to our survey responses. This pandemic-induced reallocation of floor space across firms is quite modest.

Our results are consistent with early evidence from asset markets indicates that the COVID-19 shock has materially shifted the distribution of CRE values, improving the relative outlook for real estate devoted to data centers, cell towers, self-storage, and warehousing while worsening the relative outlook for real estate holdings in the hospitality and retail sectors.

To shed more light on the forces driving floor space needs, we performed a regression of the expected percent change in each firm's floor space needs on its expected growth rate of sales (or employment) and its share of full-time employees working from home. Although our regression model explains only a small fraction of expected firm-level changes in floor space, we find a statistically significant negative effect of the firm's current working-from-home share on its expected change in floor space needs. However, that effect is overshadowed by the effect of the firm's expected growth in sales (or employment). The takeaway here is that changes in square footage align more closely with expected growth than with the share of folks working from home.

To sum up, our survey evidence points to a very small impact of the pandemic on overall CRE demand. In fact, our data cannot reject a net effect of zero. Our results also suggest that the pandemic-induced reallocation of total space across firms will be quite modest. Of course, we might see firms change the mix of space—for example, shifting from office space in urban high-rise buildings to suburban office parks.

Finally, subject to the caveats listed above, our conclusion that overall business demand for floor space will be nearly unchanged does not bode well for a resurgence in the growth of nonresidential construction (which has overall been rather flat over the past several years). In terms of thinking about the pace of the recovery, it seems unlikely that the demand for office space will be a big positive or negative factor.

By David Altig, executive vice president and research director in the Atlanta Fed's Research Department,

By David Altig, executive vice president and research director in the Atlanta Fed's Research Department,

Jose Maria Barrero, assistant professor of finance at Instituto Tecnológico Autónomo de México Business School,

Jose Maria Barrero, assistant professor of finance at Instituto Tecnológico Autónomo de México Business School,

Nick Bloom, the William D. Eberle Professor of Economics at Stanford University,

Nick Bloom, the William D. Eberle Professor of Economics at Stanford University,

Steven J. Davis, the William H. Abbott Professor of International Business and Economics at the Chicago Booth School of Business and a senior fellow at the Hoover Institution,

Steven J. Davis, the William H. Abbott Professor of International Business and Economics at the Chicago Booth School of Business and a senior fellow at the Hoover Institution,

Brent Meyer, a policy adviser and economist in the Atlanta Fed's Research Department,

Brent Meyer, a policy adviser and economist in the Atlanta Fed's Research Department,

Emil Mihaylov, research analyst in the Atlanta Fed's Research Department, and

Emil Mihaylov, research analyst in the Atlanta Fed's Research Department, and