The COVID-19 pandemic has strained the American economy. The CARES Act (short for the Coronavirus Aid, Relief, and Economic Security Act), which was passed in late March 2020, offers targeted relief to many of the hardest-hit areas of the economy. One type of assistance the CARES Act made available is mortgage forbearance, which permits homeowners with a federally backed mortgage (that is to say, the vast majority of outstanding mortgages) to request a payment holiday on their mortgage, typically for up to six months with the possibility of extension. In July, the Atlanta Fed blogged about the details of mortgage forbearance policies, remarking that the latest reports at that point showed about 8.5 percent of borrowers were in forbearance programs, either as a result of the CARES Act or from servicers of mortgages not backed by the government electing to follow suit with the CARES Act. The blog also showed that Ginnie Mae and private loans have consistently trended above the whole-market forbearance rate, and Fannie Mae and Freddie Mac loans have generally had forbearance rates below the whole-market average. A recent report by Black Knight![]() showed the active forbearance rate at the end of December 2020 to be 5.3 percent, or more than one in 20 U.S. mortgages.

showed the active forbearance rate at the end of December 2020 to be 5.3 percent, or more than one in 20 U.S. mortgages.

While we have solid insights into mortgage forbearance![]() at the national level by investor type, we are somewhat lacking in more granular insights on forbearance usage. What do we know about the borrowers in forbearance programs? This question led us to develop a new interactive tool, called the Mortgage Analytics and Performance Dashboard (MAPD), which has been freshly updated with the most recently available data from October 2020. Using the tool, we can focus on month-by-month forbearance usage as a fraction of all mortgages in each state, county, and ZIP code in the entire country.

at the national level by investor type, we are somewhat lacking in more granular insights on forbearance usage. What do we know about the borrowers in forbearance programs? This question led us to develop a new interactive tool, called the Mortgage Analytics and Performance Dashboard (MAPD), which has been freshly updated with the most recently available data from October 2020. Using the tool, we can focus on month-by-month forbearance usage as a fraction of all mortgages in each state, county, and ZIP code in the entire country.

For the purposes of this Macroblog post as well as in MAPD, we will refer to mortgages as being "delinquent" if they have missed a payment and are not using forbearance. Mortgages "using forbearance" are those that have missed a payment and are, according to our best guess, in a forbearance program. "Nonpayment" is the sum of forbearance usage and delinquency, and we count a mortgage as a nonpayment if the borrower missed a payment, regardless of forbearance status.

MAPD estimates forbearance usage, not enrollment, an important distinction in light of indications from Black Knight![]() that many borrowers in forbearance at the beginning of the pandemic made full payments. Estimating forbearance usage also means that we cannot explicitly observe or identify it in the data. Only a handful of clues in the dataset allow us to make an educated guess at whether a loan is in forbearance and using it. (The specific procedure for deciding whether or not a loan is in forbearance is laid out on the MAPD webpage, under the heading "Data Definitions and Sources.")

that many borrowers in forbearance at the beginning of the pandemic made full payments. Estimating forbearance usage also means that we cannot explicitly observe or identify it in the data. Only a handful of clues in the dataset allow us to make an educated guess at whether a loan is in forbearance and using it. (The specific procedure for deciding whether or not a loan is in forbearance is laid out on the MAPD webpage, under the heading "Data Definitions and Sources.")

First, a few caveats: MAPD focuses only on owner-occupied homes. It excludes the rental market because the only rental data we have from MAPD's data source are for investor-owned homes with mortgages, which is an incomplete representation of the entire rental market. Also, the dataset is lagged by about 90 days, and many small geographies (for example, some very sparsely populated rural ZIP codes) lack sufficient data for accurate reporting.

We invite you to explore MAPD, and we offer a few of our own observations. First, delinquencies and forbearances seem to have an inverse relationship in most places. Second, mortgage performance trends in urban areas differ substantially from those in rural areas. Third, mortgage performance trends in lower-income areas are notably different from those in higher-income areas. Finally, economies heavily reliant on tourism have some of the highest rates of forbearance in the United States. Let's examine these observations one by one:

- Forbearance and delinquencies vary inversely, even at a small scale.

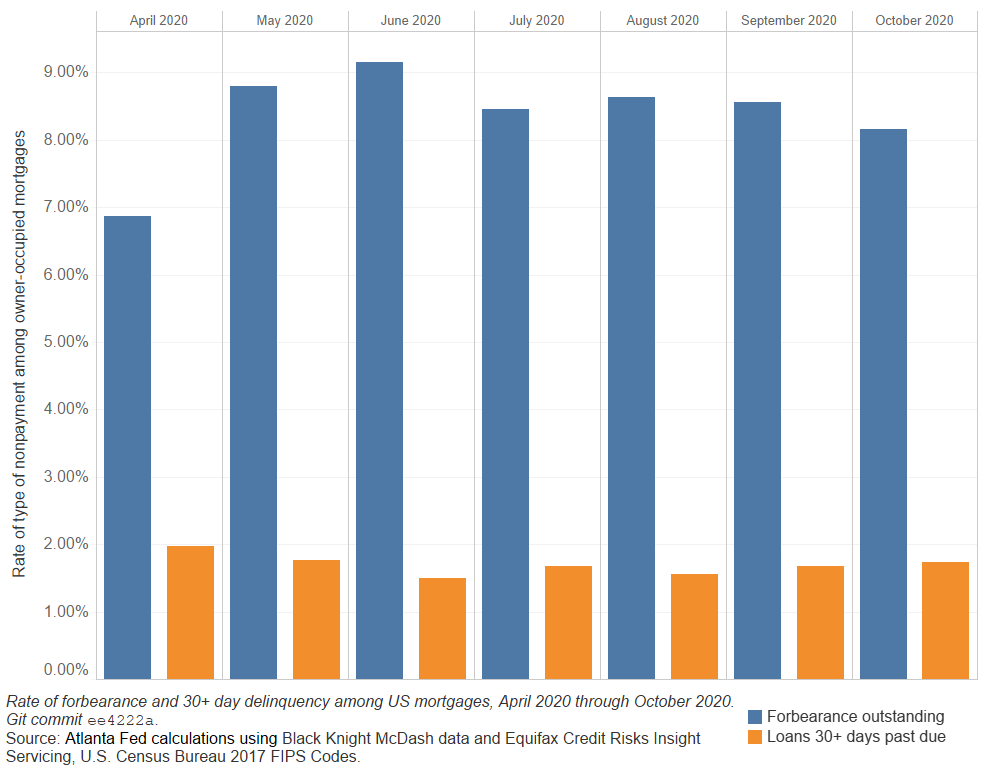

Looking at any of the state, county, and ZIP code-level maps in MAPD makes it clear that declines in estimated mortgage delinquency rates happened alongside increases in usage of forbearance. We can clearly identify this inverse relationship at the national level using the time-series bar charts in MAPD. To illustrate this observation, we have combined these data into a single chart.

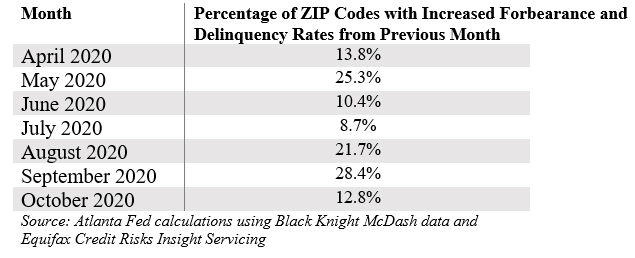

The underlying data also show us that the national trends tend to translate to the small scale by revealing how often, in a given month, a ZIP code has simultaneous increases in both delinquency and forbearance rates. In fact, in any given month, our data show that only between about a tenth to a quarter of U.S. mortgages experienced an increase in both the forbearance and delinquency rates in their ZIP code (see the table).

It does appear that August and September 2020 showed simultaneous and substantial upticks in forbearance and delinquency, so it will be interesting to monitor the data to see if October's reduction persisted in subsequent months. - Urban areas have higher forbearance rates than nonurban areas.

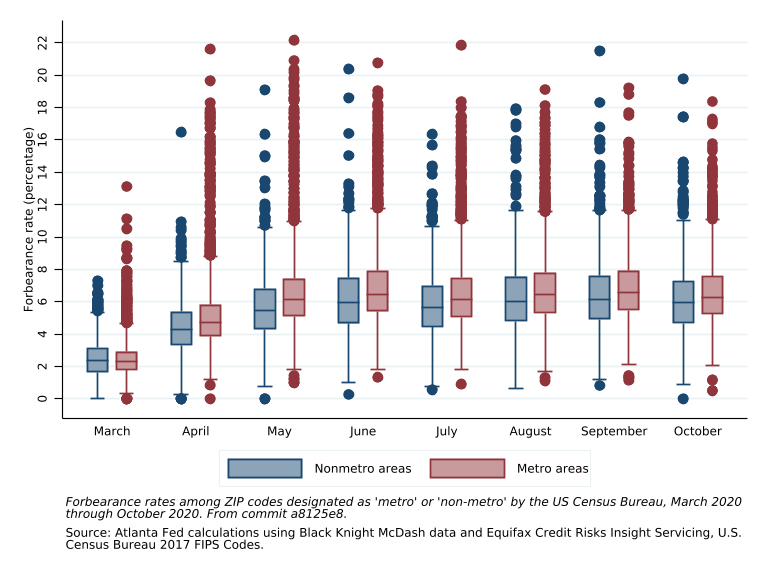

Looking at the underlying county data in MAPD, we can see that in October 2020, the average rate of forbearance in counties designated as "nonmetro" by the U.S. Census Bureau tends to be slightly lower than in urban areas. Notably, the Census Bureau's definitions of "metro" and "nonmetro" are handy, but they tend to apply the "metro" distinction more broadly than most people might assume. Its definition means a population center, plus all surrounding areas that have a "high degree" of social and economic integration with that center, which normally includes suburbs and exurbs. By looking at the county and ZIP code maps, we can see that even within a metro area (available for the user to select from the drop-down menu), counties close to the urban core have higher forbearance rates than the surrounding areas (see the chart).

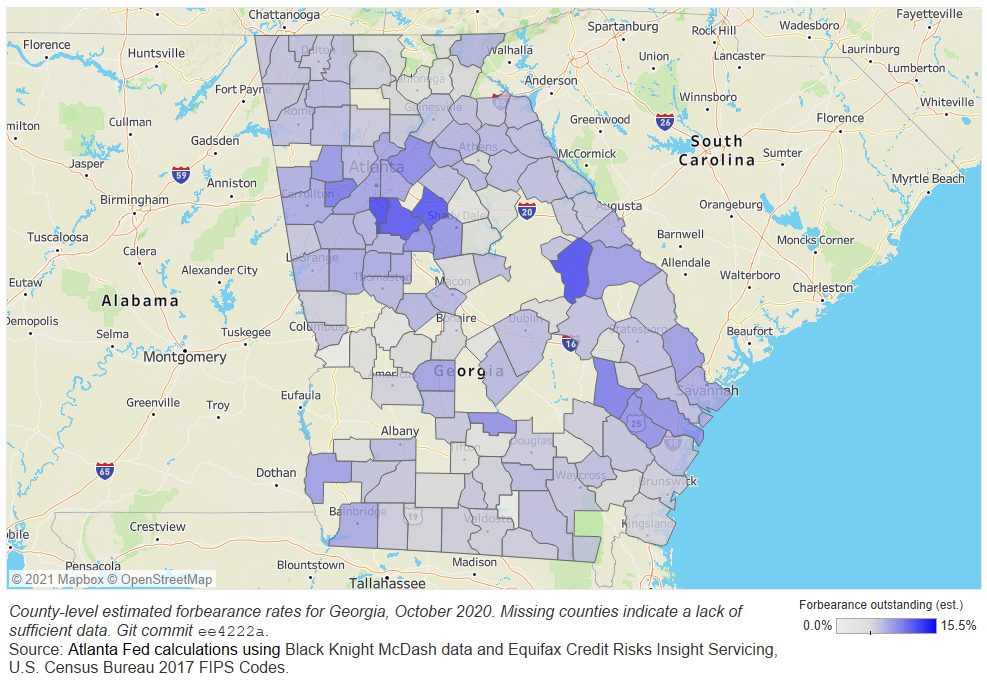

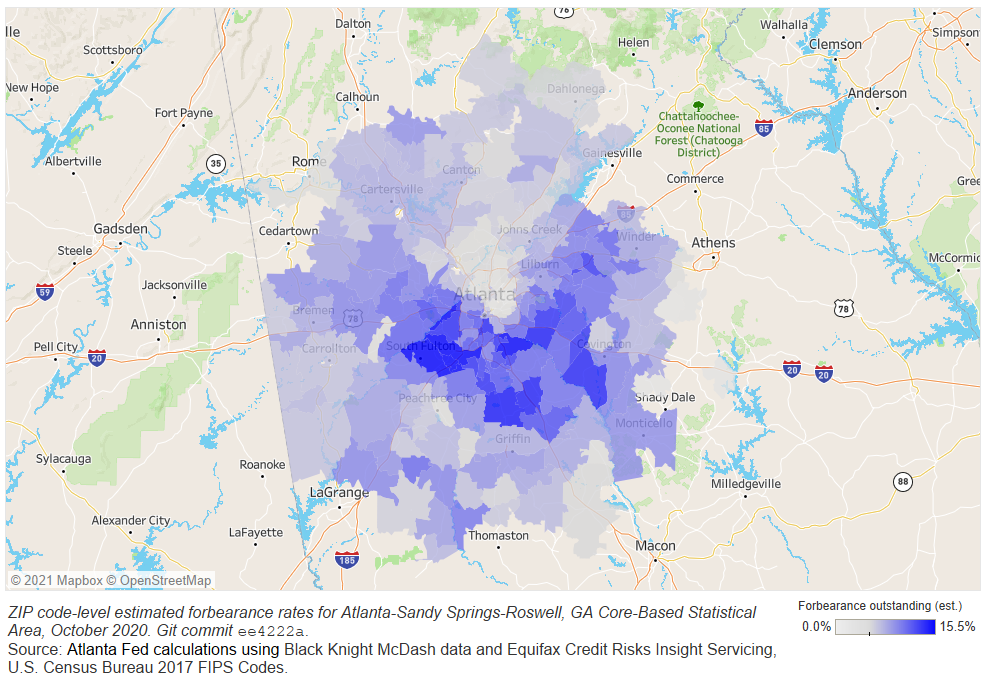

Taking Georgia as an example, the MAPD tool shows us that higher forbearance rates (darker blue) tend to occur in more urban counties (most notably around Atlanta; see the map).

Using the ZIP code view within Atlanta, we also see the trend that areas closer to the urban core experience higher rates of forbearance, though this could also be reasonably linked to income. I explore this topic in the next section.

- Lower-income areas have more forbearance.

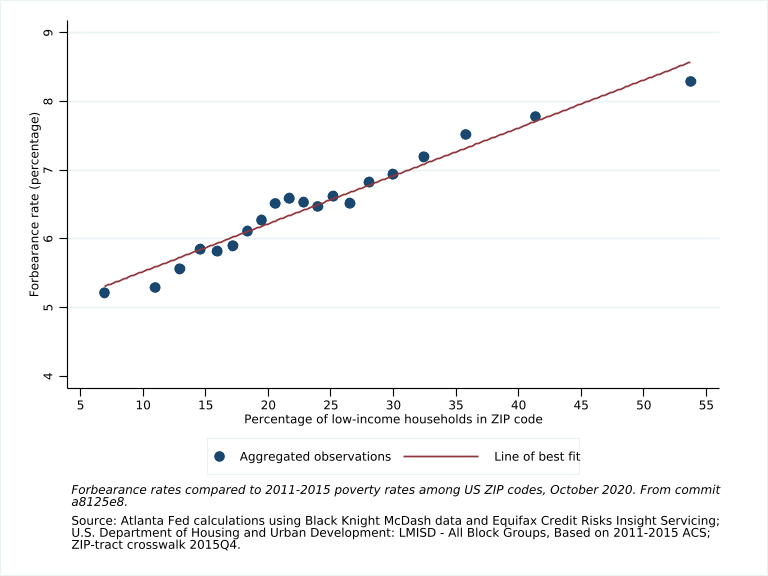

Looking at the ZIP code-level map makes it plain that lower-income areas of most major cities have estimated forbearance rates substantially greater than rates in higher-income areas. Keeping in mind that MAPD estimates the rate of households actually using forbearance (for example, in forbearance and having missed at least one payment), so we may reasonably infer that households in lower-income ZIP codes are using forbearance at a higher rate than households in high-income areas (see the chart).

From a public policy perspective, this is good news: the owner-occupied households less likely to be able to withstand an income shock without defaulting on their mortgage are receiving economic assistance through forbearance. This is not to say, however, that all needs of low-income communities are being met. Rather, forbearance is helping address their needs at a higher rate than in higher-income areas. - Economies dependent on leisure and hospitality have high rates of forbearance.

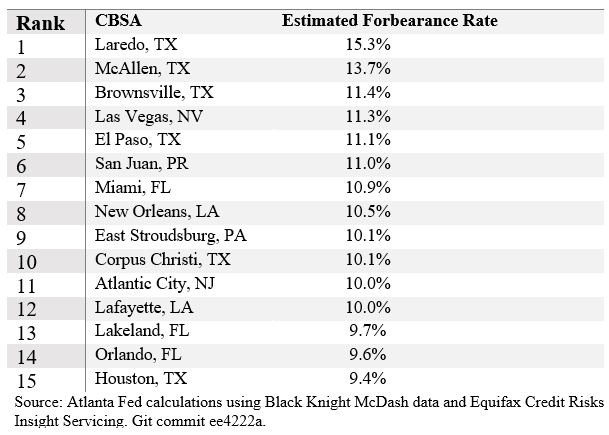

A final observation is that areas economically exposed to the pandemic are using forbearance at a high rate, and this is particularly true for areas heavily reliant on leisure and hospitality. In fact, among the core-based statistical areas (CBSAs, also known informally as "metro areas") that had the highest forbearance usage rates in October 2020, six of the top 15 CBSAs (with more than 10,000 mortgages) are popular tourist destinations: San Juan, Miami, Las Vegas, Atlantic City, New Orleans, and Orlando. (We can also see that four of the top five in this list are metro areas in Texas that share a border with Mexico; cross-referencing a 2015 map of the low-income, unincorporated colonias settlements in these areas seem to overlap with what MAPD reports as the highest ZIP code-level rates of forbearance in Laredo, McAllen, Brownsville, and El Paso.)

seem to overlap with what MAPD reports as the highest ZIP code-level rates of forbearance in Laredo, McAllen, Brownsville, and El Paso.)

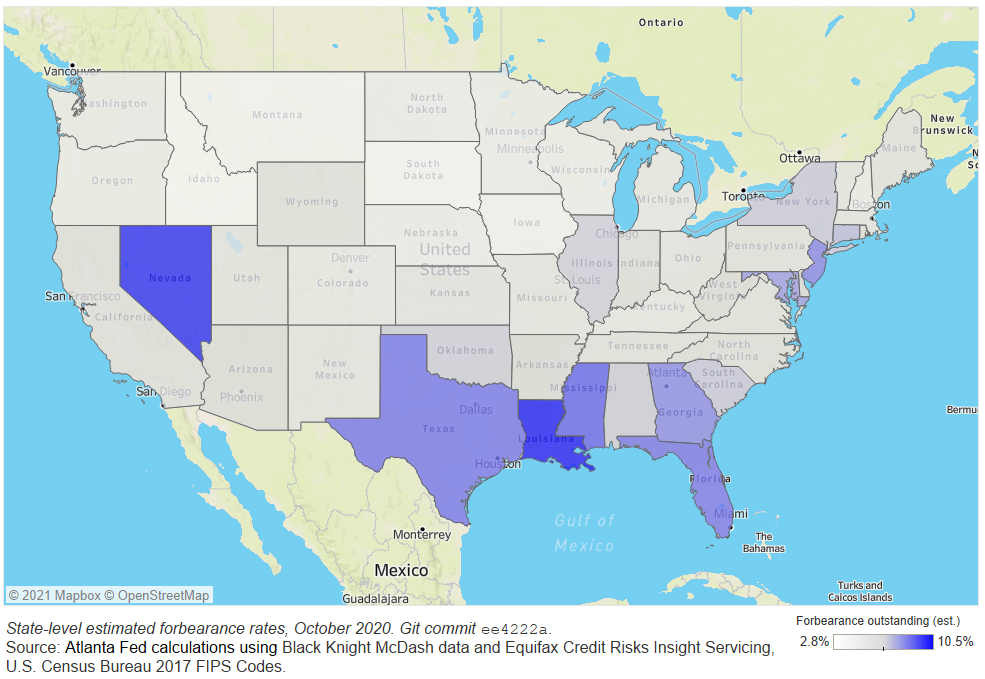

Using the state view in MAPD, we can clearly see how erosion in the leisure and hospitality sector has affected forbearance rates: Florida, Nevada, New Jersey, and Louisiana are among the states with the highest overall forbearance rates (darkest blue in the map).

Policymakers have important questions to consider. For example, what size will the arrears be when borrowers exit forbearance? (Typically, forbearance programs allow arrears to be rolled into a separate, interest-free loan, placing the risk on the mortgage servicer.) And how consistent have the payments of those in forbearance been just before forbearance expires? As forbearance programs begin to expire, understanding patterns of nonpayment leading up to forbearance expirations will likely serve as a good predictor of distressed borrowers' ability to meet future mortgage obligations.

Taking one further step back, the U.S. Bureau of Labor Statistics' December jobs report showed a loss of 140,000 jobs, the first monthly decline since the beginning of the pandemic early last year. Those lost jobs, and the jobs lost and regained during the tumult of 2020, are not dispersed randomly throughout the economy; certain industries were severely hurt even as others benefited. While MAPD data cannot paint a perfect picture of the assistance that mortgage holders are receiving, it does allow the user to gather quick insights about the degree to which certain areas have received economic relief—and opportunities for outreach to those that have not.

By

Daniel Sexton, a quantitative research analysis specialist in the Atlanta Fed's Research Department