The US Census Bureau recently announced some changes it plans to make this year to the Current Population Survey Public Use File (CPS PUF). Here at the Atlanta Fed, we use data from the CPS PUF to construct the Wage Growth Tracker, and one of the planned changes will significantly affect the tracker. Specifically, a person's usual weekly or usual hourly earnings, which are unrounded currently, will be rounded.

The Wage Growth Tracker bases its results on the median, or middle, observation in the distribution of percent wage changes for a sample of individuals linked between the current month and the same month a year earlier. The Wage Growth Tracker time series has yielded useful insight into the rapidly shifting dynamics of the labor market in the wake of COVID-19, especially as compositional effects have distorted wage data. It's also helped economists and policymakers understand which income levels were seeing the greatest growth and that job switchers were finding the most wage gains.

How will the rounding of wage data affect the Wage Growth Tracker? The announced CPS PUF rounding rules vary by wage level and are different if the earnings are reported on an hourly or weekly basis. (You can see more details here ![]()

![]() .) Most people in the CPS report earnings on an hourly basis, and most wage observations range from $10 to $99.99 an hour. Under the rounding rules those earnings will be rounded to the nearest dollar. So, for example, if someone reports making $14.50 an hour, that wage will be rounded to $15, while workers reporting a wage of $15.40 an hour will also have that wage rounded to $15.

.) Most people in the CPS report earnings on an hourly basis, and most wage observations range from $10 to $99.99 an hour. Under the rounding rules those earnings will be rounded to the nearest dollar. So, for example, if someone reports making $14.50 an hour, that wage will be rounded to $15, while workers reporting a wage of $15.40 an hour will also have that wage rounded to $15.

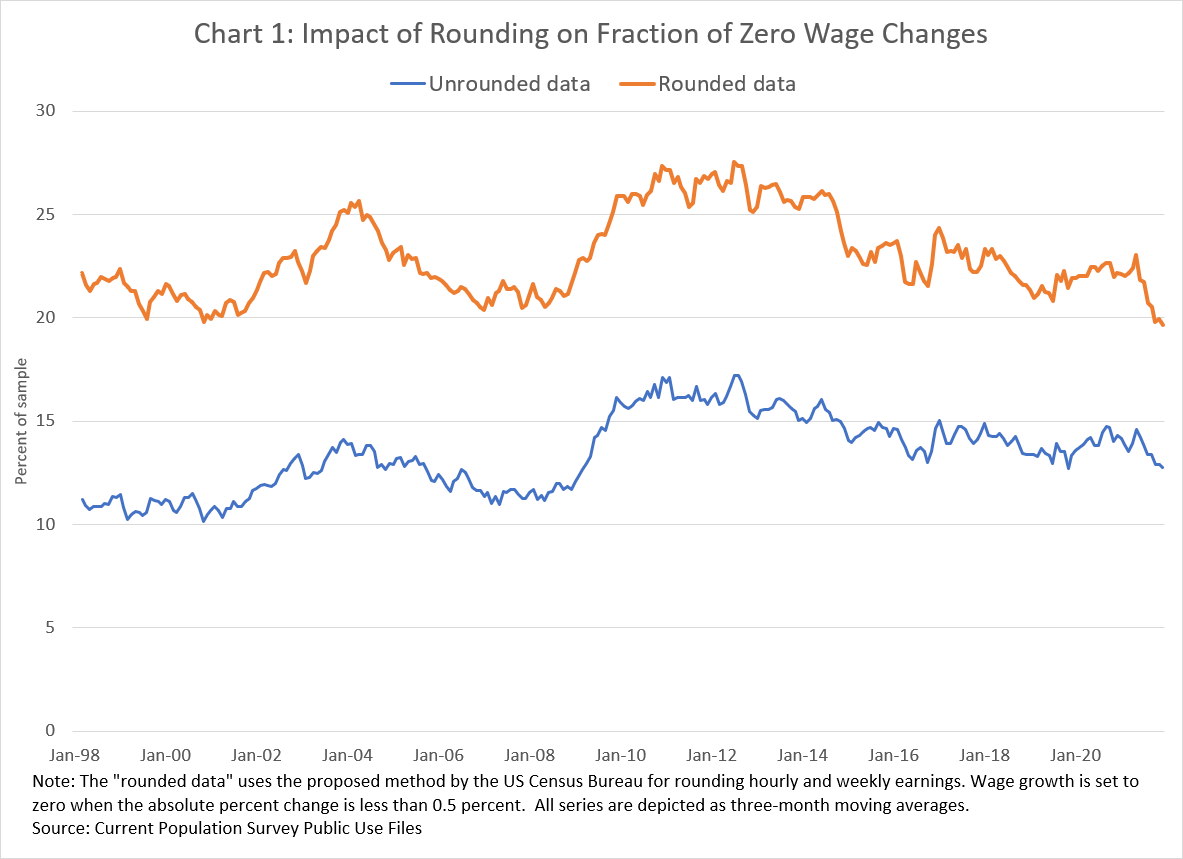

One implication of the rounding rules is that it will make no wage change appear more common than it currently is. To illustrate, suppose someone's pay went from $14.50 to $15.40 an hour. The rounding rules would show no change in the person's wage (both would be recoded as $15) even though that person's actual wage increased by 6.2 percent. Chart 1 shows what happens to the proportion of zero wage changes if the rounding rules were applied to the CPS PUF earnings data used to construct the Wage Growth Tracker from 1998 to 2021.

As you can see, during the Great Recession, when labor demand was especially weak, about 17 percent of wage growth observations based on unrounded earnings data were zero. But if the rounding rules had been applied back then, more than 25 percent of wage growth observations would have been zero.

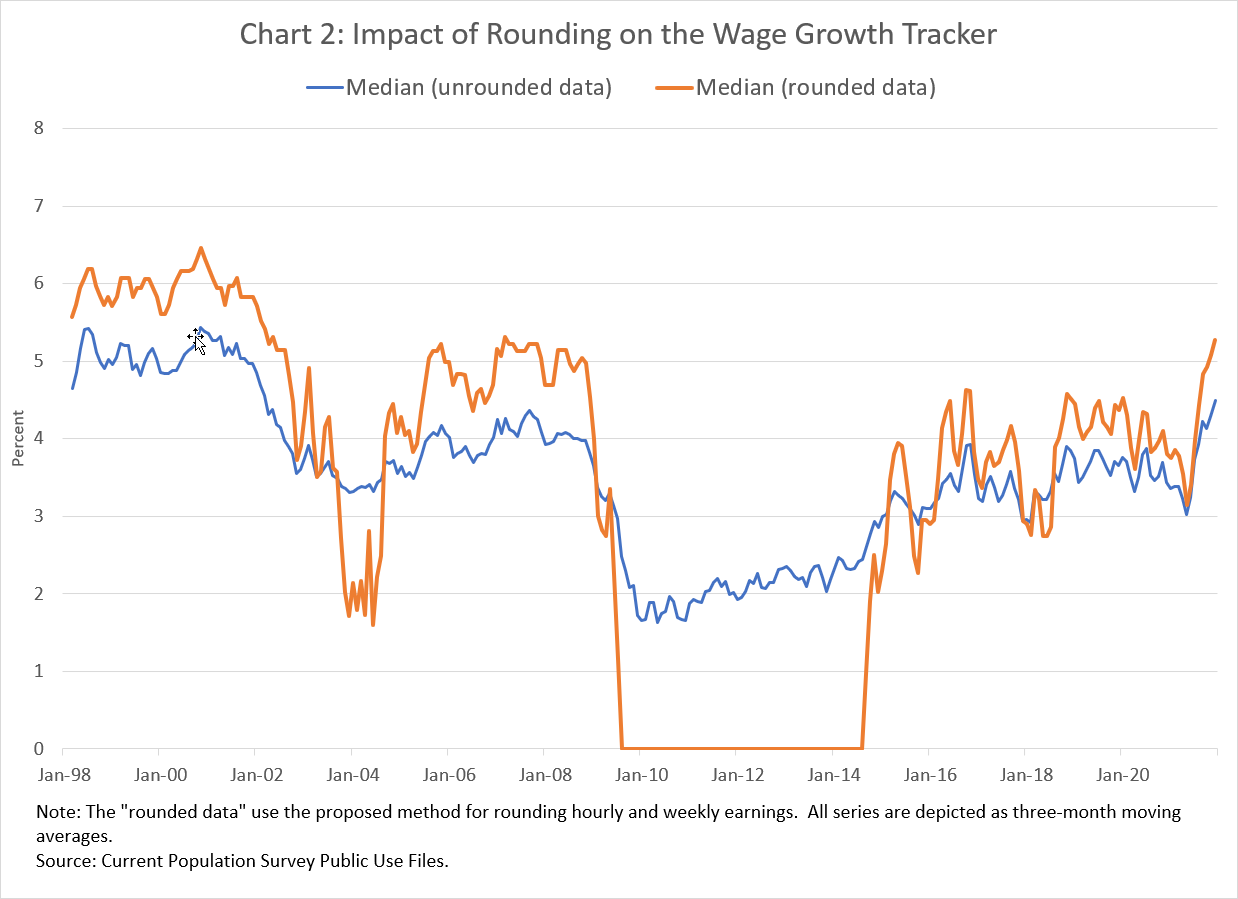

Obviously, this change is a big deal for the Wage Growth Tracker. When more than a quarter of the observations are zero near the middle of the wage change distribution, it is very likely that the median observation will also be zero. This effect is evident in chart 2, which compares the median Wage Growth Tracker series using unrounded earnings data with what it would have been if the rounded data had been used.

![]()

{kind=link}

Clearly, if the rounding rules had been in place in the past, the Wage Growth Tracker time-series would be a much less useful indicator of wage growth or labor market trends.

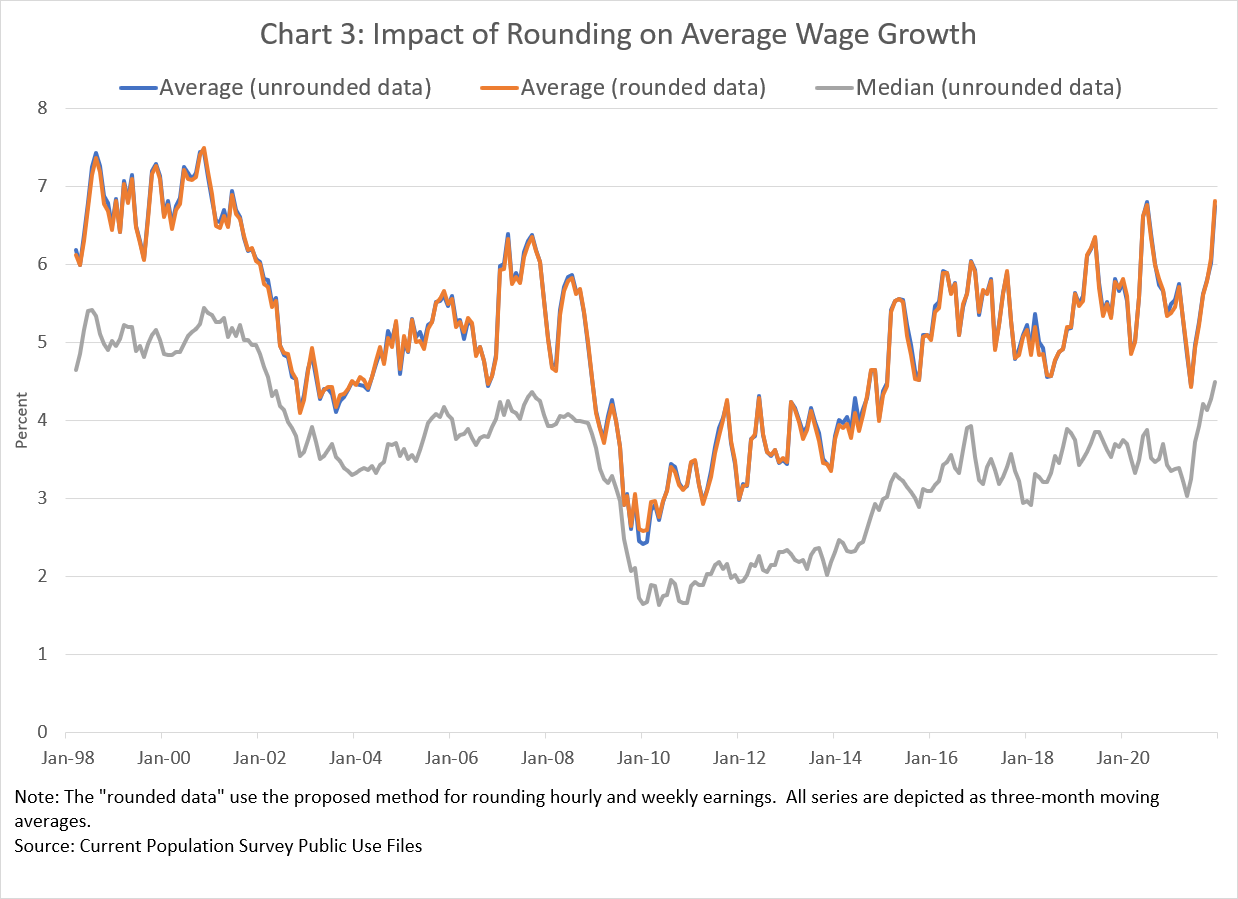

So, what to do? It turns out that the rounding rules don't affect all summary measures of wage growth as much as they affect the median measure. For example, as chart 3 shows, the mean—or average—wage growth comes out of the rounding changes essentially unaffected.

Unfortunately, not only is the average higher than the median, because wage growth varies greatly across individuals (the monthly sample standard deviation is typically around 25 percent), you can also see that both of the average wage growth series are much more variable month to month than the median series using unrounded data. Indeed, the robustness to variability in the underlying wage change data is a primary reason why the Atlanta Fed's Wage Growth Tracker is based on median rather than average wage growth.

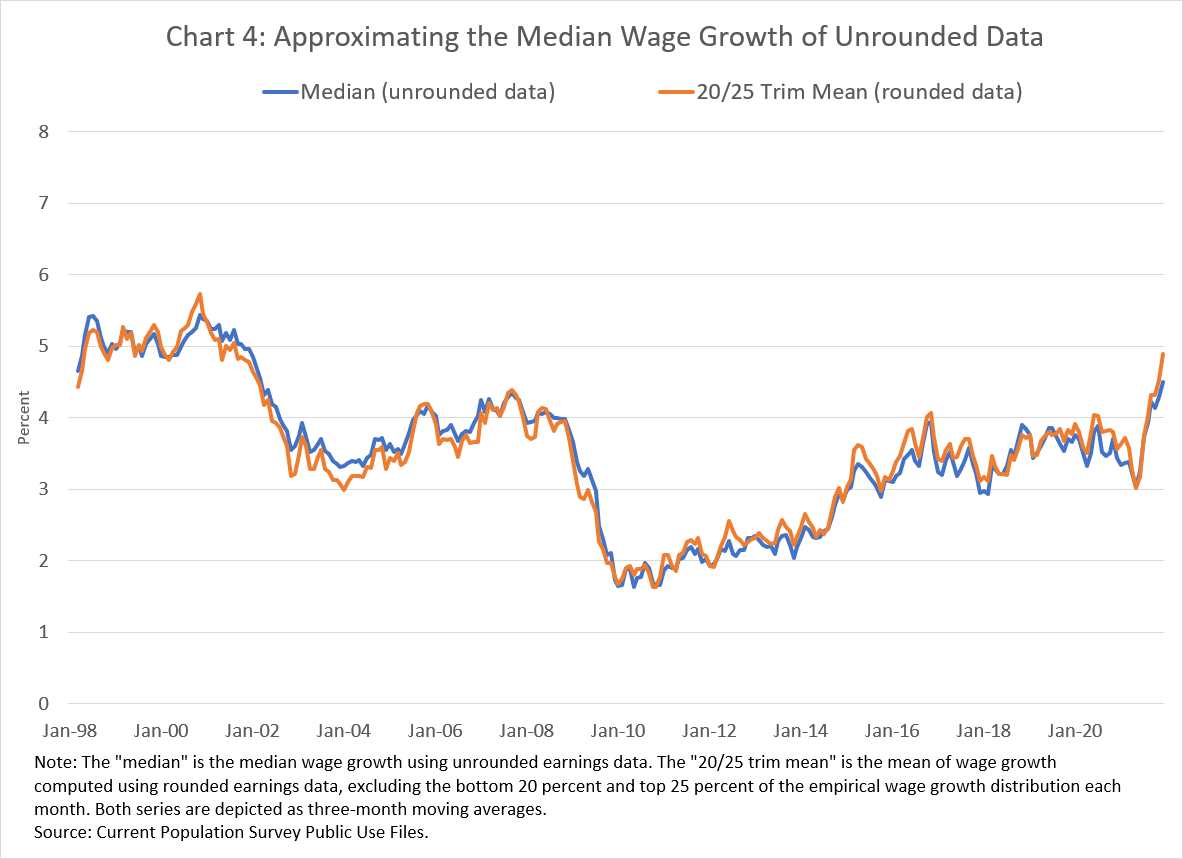

But there is potential solution. Borrowing from the research![]() on using trimmed means of price change data to construct measures of inflation that are robust to extreme price changes, I was able to construct a trimmed-mean wage growth series using the rounded data that has broadly similar properties to the (median) Wage Growth Tracker series constructed from unrounded data. Specifically, for each month's sample, I excluded the bottom 20 percent of wage growth observations (that is, the largest percent wage declines) and the top 25 percent (the largest percent increases) and computed the average of the remaining data. (Note that the trimming is asymmetric because more of the large wage changes tend to be increases than decreases, which is also why the average is higher than the median in the previous chart.)

on using trimmed means of price change data to construct measures of inflation that are robust to extreme price changes, I was able to construct a trimmed-mean wage growth series using the rounded data that has broadly similar properties to the (median) Wage Growth Tracker series constructed from unrounded data. Specifically, for each month's sample, I excluded the bottom 20 percent of wage growth observations (that is, the largest percent wage declines) and the top 25 percent (the largest percent increases) and computed the average of the remaining data. (Note that the trimming is asymmetric because more of the large wage changes tend to be increases than decreases, which is also why the average is higher than the median in the previous chart.)

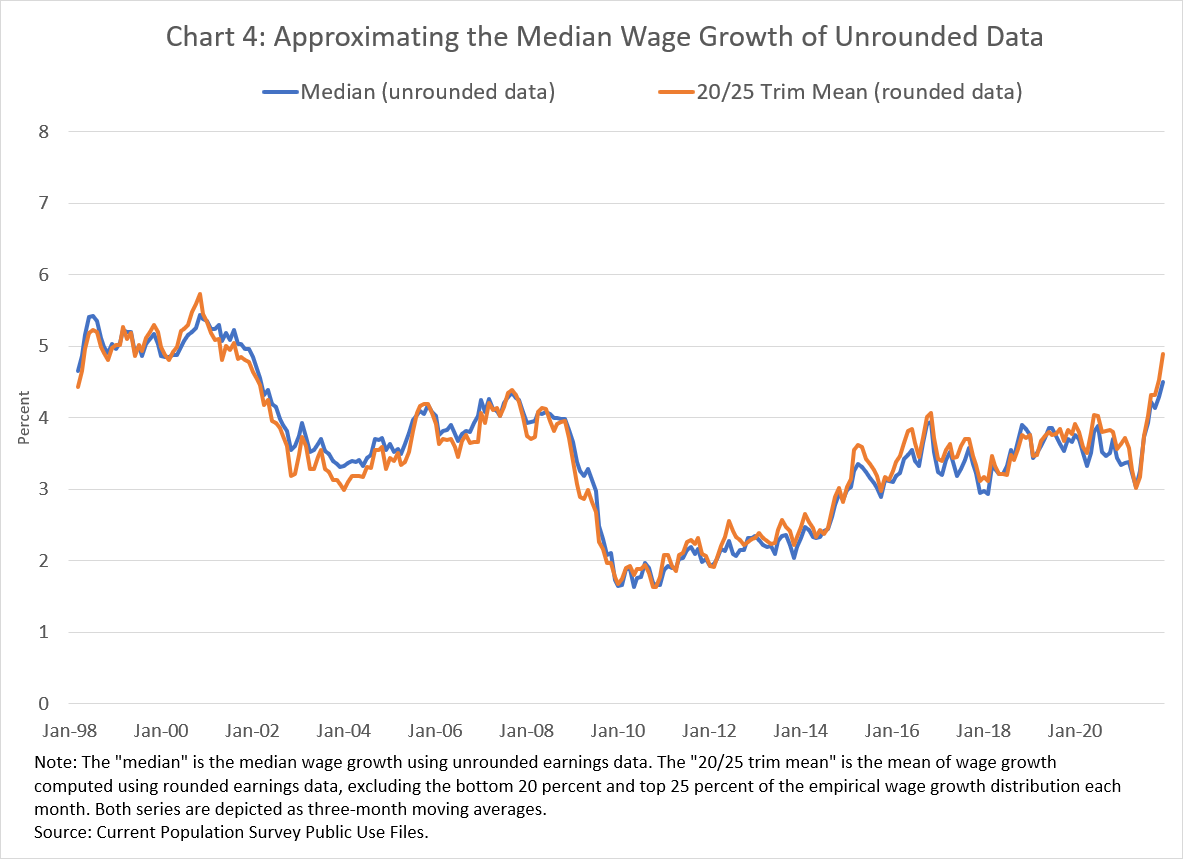

Chart 4 shows the trimmed-mean series constructed using rounded earnings data, along with the (median) Wage Growth Tracker series that uses unrounded data. I would describe this trimmed-mean series as a reasonable (though not perfect) approximation of the Wage Growth Tracker series (something we could have used if we only had rounded earnings data in the past).

{kind=link}

When the January 2022 CPS PUF data become available in February, we will produce the trimmed-mean version of the overall Wage Growth Tracker and add it to the Atlanta Fed's Wage Growth Tracker data set. We are currently exploring if a similar approach will produce useful alternatives to the Wage Growth Tracker for other ways to view the data, such as those for job switchers versus job stayers, or by average wage level. Watch this space for updates.

By John Robertson, a senior policy adviser in the Atlanta Fed's Research Department