The Atlanta Fed's Wage Growth Tracker (WGT) measure of year-over-year nominal wage growth has been elevated during the last couple of years. It was 6.1 percent in December 2022. Although this level is down from its high of 6.7 percent in June and July of last year, it is much higher than the 3.6 percent average seen in 2019, before the COVID-19 pandemic. At the same time, inflation has also been high. For example, the consumer price index (CPI) increased 6.5 percent from December 2021 to December 2022. As a result, the real or inflation-adjusted WGT for December 2022 was −0.4 percent.

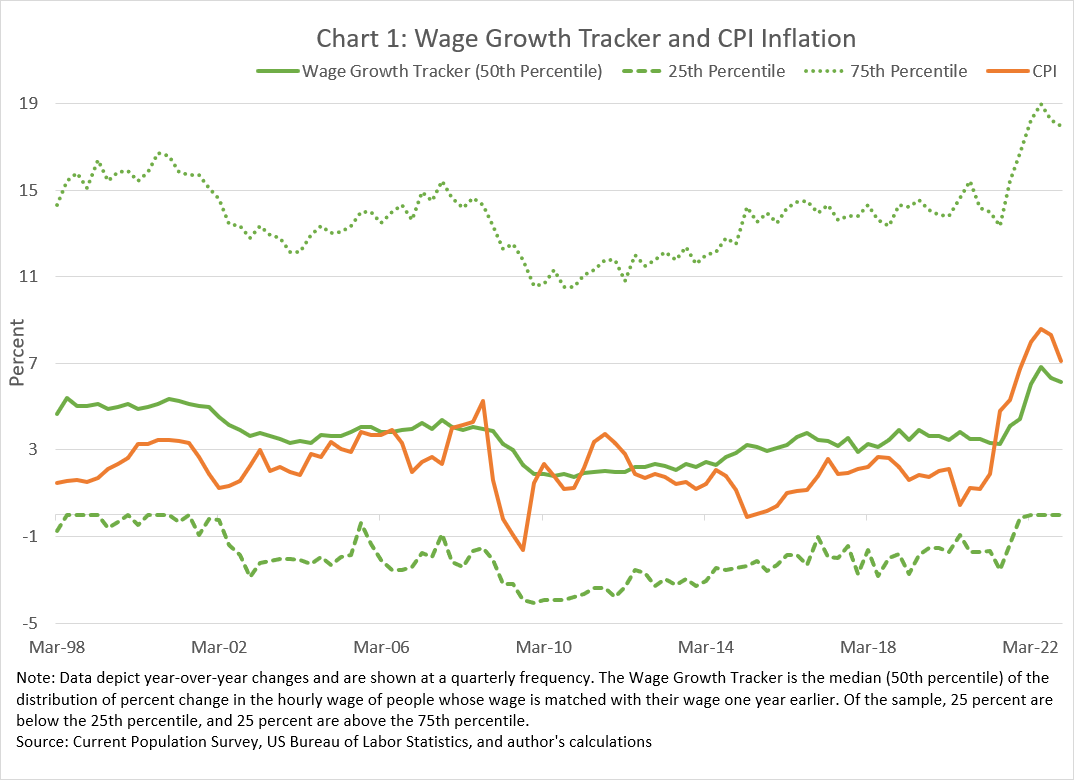

To see how the WGT has performed relative to inflation over time, chart 1 shows the time series of the Wage Growth Tracker (the solid green line) and the 12-month rate of change in the headline CPI (the solid orange line) since 1998.

{kind=link}

As you can see, the WGT, in terms of median wage growth, has been below the average rate of inflation for most of 2021 and 2022. Prior to that period, the last time the real WGT had been negative was during 2011—a short period when CPI inflation reached 4 percent while the WGT was hovering around 2 percent.

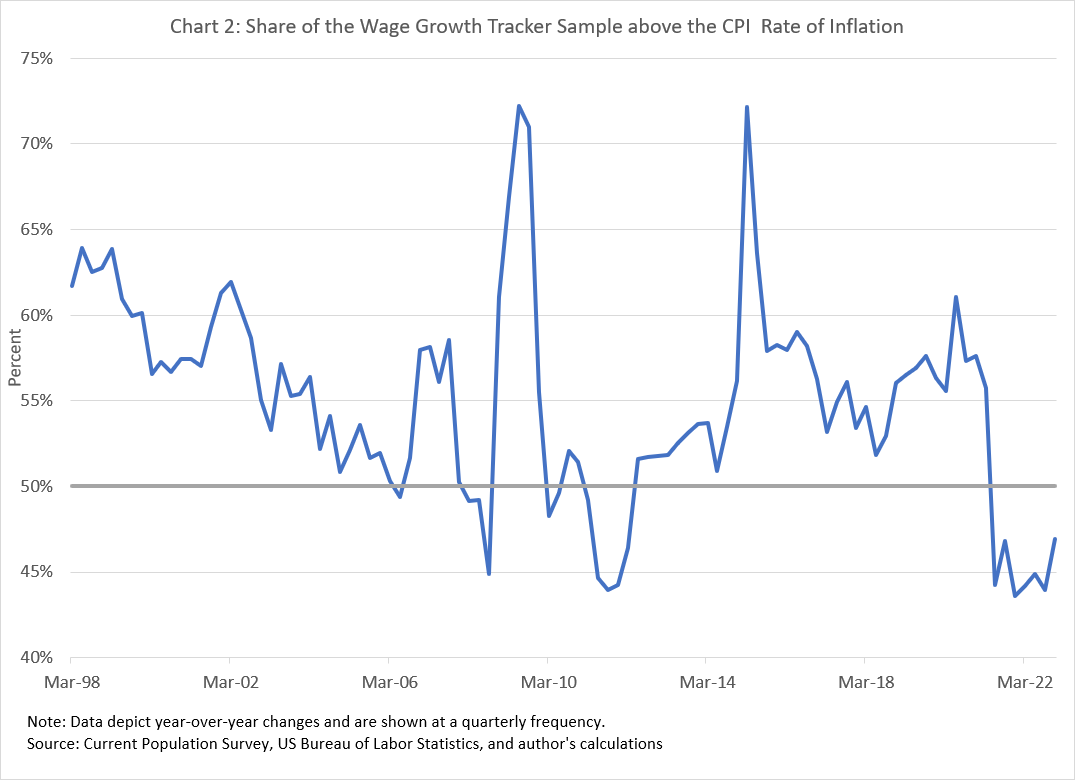

The fact that the real WGT is negative tells us that less than 50 percent of the people in the WGT sample had real wage increases, relative to the CPI. But as you can also see in chart 1, at any point in time the distribution of wage growth across individuals varies widely. For example, during 2022, around 25 percent of the sample reported nominal wage growth of more than 18 percent, while another 25 percent reported nominal wage growth at or below zero. As a result of this wide dispersion of wage growth across people, a significant minority of people experience real wage gains even when inflation is elevated, just as a significant minority experience real wage declines even when inflation is low. Chart 2 shows the percentage of the nominal wage growth sample that was above the prevailing rate of inflation in each quarter.

{kind=link}

For example, about 57 percent of the WGT sample had positive real wage gains during 2019, whereas during 2022, only 45 percent of people had positive real wage growth. Put another way, despite higher median nominal wage growth, the share of people with positive real wage growth between 2019 and 2022 due to higher inflation fell by 12 percentage points.

As a simple counterfactual, if the rate of inflation had stayed at its 2019 average level of 1.8 percent, then close to 63 percent of people would have had positive real nominal wage growth in 2022. That is, a tight labor market without high inflation would have resulted in a 6 percentage point gain in the share of workers experiencing real wage growth relative to 2019, rather than a 12 percent decline.

One thing to keep in mind when interpreting chart 2 is that it implicitly assigns the same CPI inflation to everyone's wage growth within a period. Recall that the CPI is an index of price changes for a representative basket of goods and services, but such a basket is unlikely to fully capture the cost-of-living experience for any individual. (The Atlanta Fed's myCPI tool will give you an idea of how CPI inflation varies among broad groups of people. Unfortunately, users cannot map myCPI inflation data to the individual-level data used to construct the WGT.)

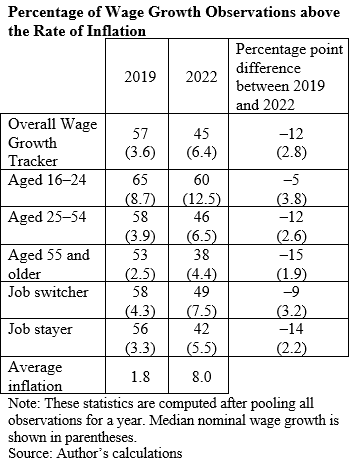

Not surprisingly, groups of workers with the highest (lowest) median wage growth are those with the highest (lowest) share of positive real wage growth. The table depicts these differences, comparing outcomes for 2019 with those for 2022 for a selection of worker types.

For example, in 2022, 60 percent of workers aged 16−24 had positive real wage growth versus 65 percent in 2019. However, the 5 percentage point decline in the share of people aged 16−24 with positive real wage growth is much smaller than the decline in the share of workers aged 25 and older who had positive real wage growth. In particular, the share of people 55 and older who saw positive real wage growth declined by 15 percentage points.

Some workers have seen their nominal hourly wage increase proportionately more than others because of the tight labor market during the last couple of years, which has blunted the impact of higher inflation on those workers. Older workers, as well as people staying in the same job, have seen the largest increase in the share of real wage losses in 2022 relative to before the COVID-19 pandemic. That said, nominal wage growth across individuals varies a lot, even within age and job mobility categories. Explaining that variation remains a challenge for economists who often attribute it factors such as differences in productivity growth at the individual and firm level. Your own wage growth experience might not look like that of your neighbors or your colleagues, and it might not resemble that of the person with median wage growth either. The median wage growth is a useful guide to shifts in the distribution of wage growth over time, but it doesn't fully capture the breadth of wage growth experiences across individuals.

By John Robertson, a senior policy adviser in the Atlanta Fed's Research Department