As the Fed discusses reducing its $120 billion in monthly purchases of Treasury and mortgage-backed securities, market pundits have begun to form opinions on whether such talk about tapering will roil markets as it did in 2013. Some believe that, given the size of the Fed's monthly purchases, such discussion will lead to similar market reactions. Others believe that markets today better understand the Fed's decision-making process around its asset purchases and interest rate policy. This market knowledge and experience may help mitigate the negative effect taper talk could have this time. In this post, we provide evidence that both perspectives are at least partially correct.

To be specific, we analyze the past and present discussions on tapering, including the effects that the Federal Open Market Committee's (FOMC) September 2013 meeting, often referred to as the "untaper" meeting because plans for tapering were delayed, and the June 2021 "talking about talking about tapering" meeting had on the market's expectations for the future path of the fed funds rate. We show that a market response similar to 2013 has already occurred in the sense that an increase in the 10-year Treasury rate coincided with market participants expecting an earlier liftoff from a fed funds rate of zero. Subsequent taper talk only marginally affected how the market expects the pace of rate hikes to proceed. In other words, the market responds to increasing Treasury rates by first pricing in a strong opinion about how much time will pass before the first rate hike. Subsequent discussions about tapering have little to no effect on the market expectations for future interest rate policy.

For our analysis, we use the Federal Reserve Bank of Atlanta's, Market Probability Tracker (MPT), to measure the market's expectations for the future course of monetary policy. The MPT is computed and reported every day on the Federal Reserve Bank of Atlanta's website and is described in detail in an Atlanta Fed "Notes from the Vault" post. The MPT uses options contracts on Eurodollar futures to estimate the market's assessment of the target ranges of future effective fed funds rate. Using derivative contracts on Eurodollars has one main advantage over studying the effective fed fund futures directly. Unlike the futures market for fed funds, the options on Eurodollar futures market is one of the most liquid in the world, with a wide collection of traded options. Moreover, Eurodollar futures deliver three-month LIBOR (or London Interbank Offered Rate), which bears a stable relation and high correlation with the effective fed funds rate in global overnight money markets. Together, these features allow the MPT to extract more confidently measures of market expectations of future effective fed funds target ranges.

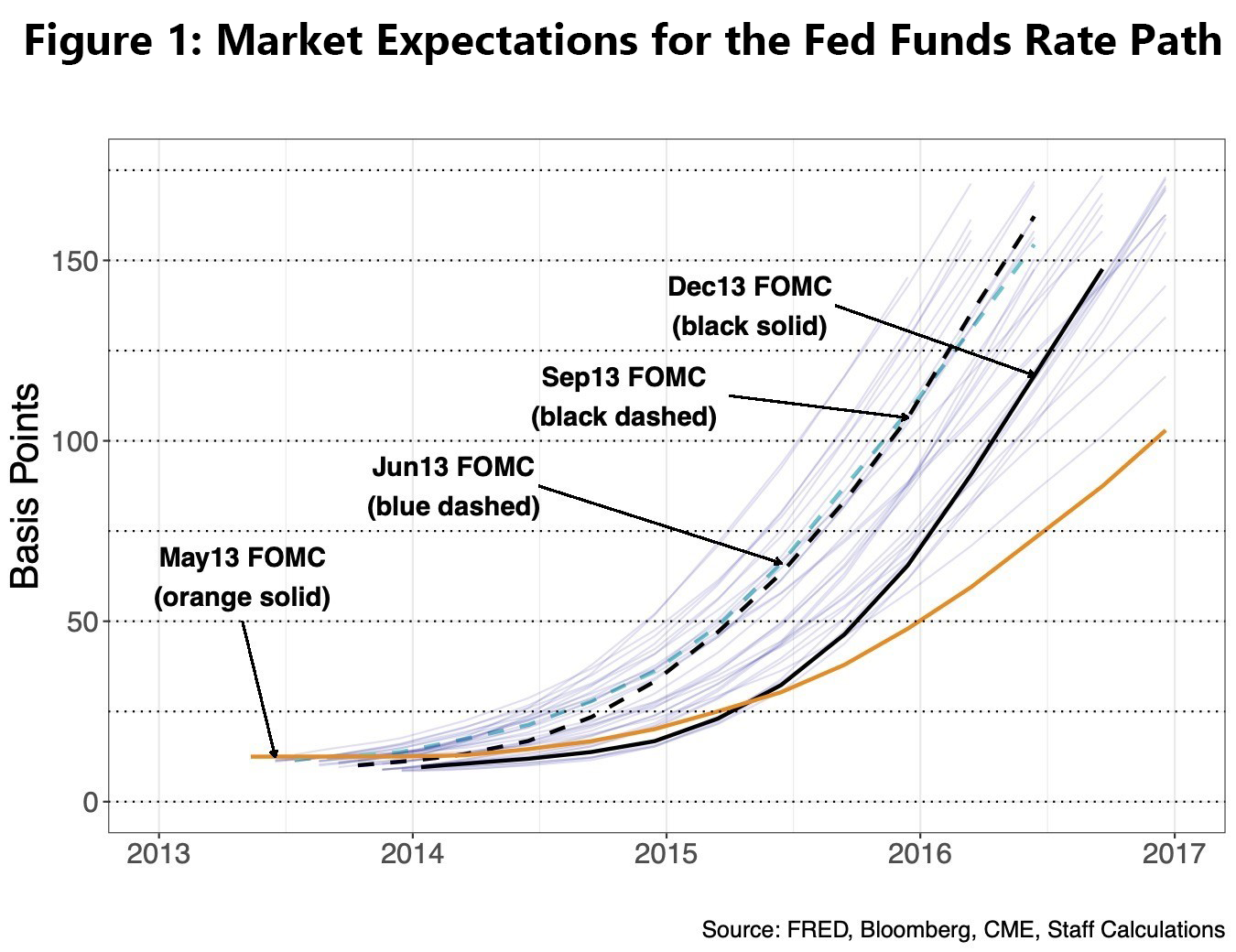

Turning our attention first to 2013, we look at how the market's expectations for the future path of rates changed as taper talk began to heat up. In figure 1, we plot several of the MPT's daily expected fed funds rate paths from before and after June 2013. Each unlabeled path in the figure is represented by a transparent blue line of the market expectations for the fed funds rate path as of Wednesday of that week. These weekly expected rate paths began on May 1, 2013, and ended on December 18, 2013, when the Fed announced it would begin paring down its asset purchases.

Note: Expectations computed daily with option data on Eurodollar futures contracts from May 1, 2013, to December 18, 2013. Each unlabeled line represents the market's expected path for monetary policy given the data as of Wednesday of the indicated week.

The orange line in figure 1 represents the market expectations as of May 1, 2013. At that time, no substantive discussion about the Fed shrinking its asset purchases had taken place. The FOMC had just released a statement that it would continue to purchase assets "until the outlook for the labor market has improved substantially in a context of price stability." Regarding its interest rate policy, the Committee stated that it "expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens." Given the Fed's policy, along with the state of the economy, the market expected the first rate hike to be in mid- to late 2015.

Between May 2013 and the next FOMC meeting on June 19, 2013 (the dashed blue line in figure 1), the market's expectation for future monetary policy began to price in an earlier rate hike sometime between late 2014 to early 2015 (see the sequence of transparent blue lines in figure 1 that move up and to the left from the orange to the dashed blue line). During this period between FOMC meetings, Ben Bernanke, then chairman of the Board of Governors, testified to Congress that the FOMC "could in the next few meetings...take a step down in our pace of purchases" (Bernanke Q&A congressional testimony, May 22, 2013).

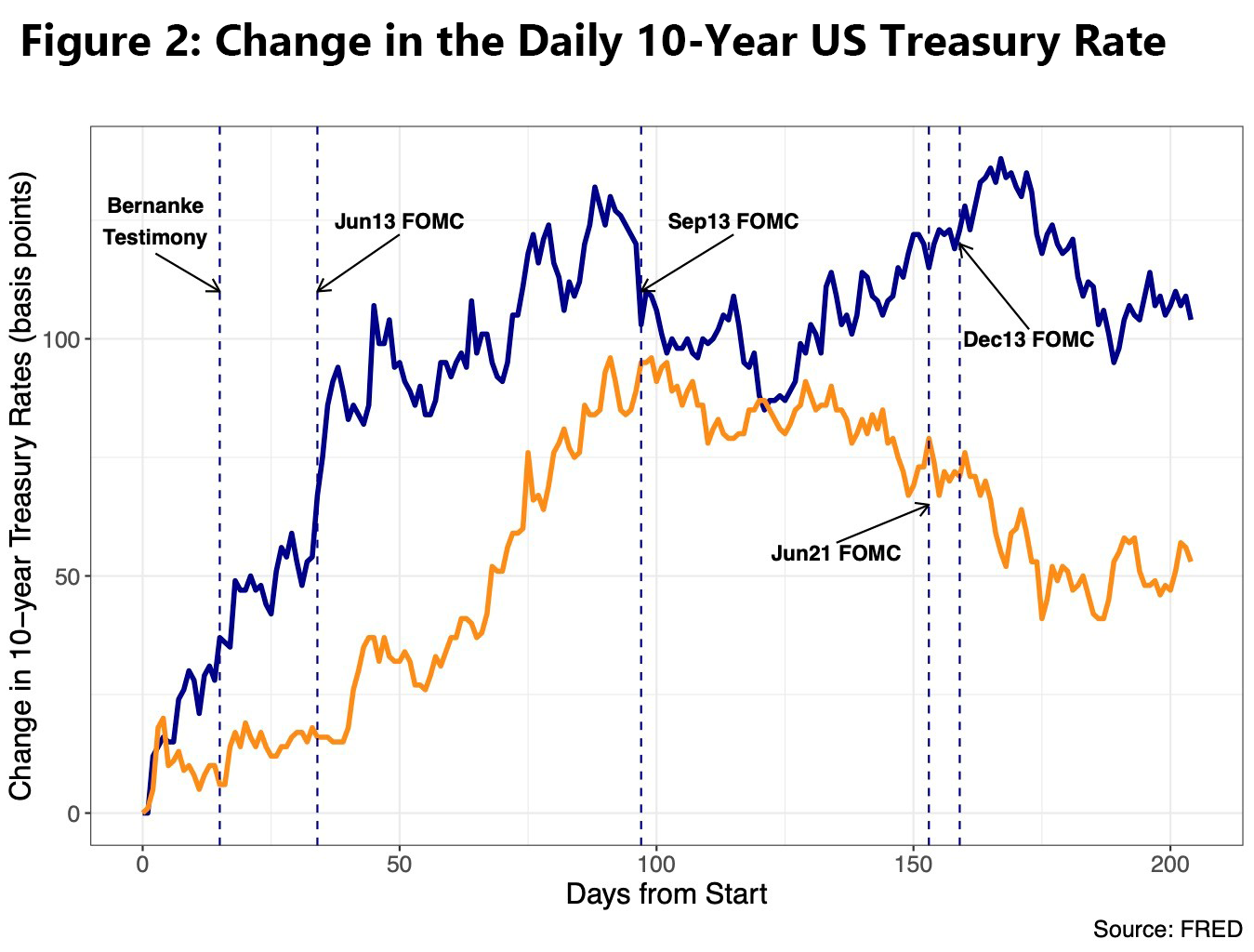

Bernanke's May 2013 testimony may have contributed to pulling forward market expectations for when the Fed would end its highly accommodative monetary policy since many expected the Fed's asset purchases to end before the fed funds rate was increased from its zero lower bound. The chair's testimony is also credited with setting off what is commonly referred to as the "taper tantrum" in the Treasury market. In figure 2, the blue line shows how much the 10-year Treasury rate had changed since May 1, 2013. According to this figure, Bernanke's testimony was certainly followed by an increase in the 10-year Treasury rate, but this increase continued a trend that began back in May 2013. And market participants had been pricing in an earlier and earlier liftoff date while the 10-year rate was increasing in May, not when the chair testified to Congress.

Note: The blue line represents the change from May 1, 2013, to February 24, 2015. The orange line represents the change from November 5, 2020, to August 27, 2021.

The Committee's June 2013 statement on monetary policy changed little from its May statement, but the expected path for the fed funds rate had already steepened (compare the dashed blue line with the orange line in figure 1). Notably, it was over the six days that followed the June FOMC statement that the 10-year Treasury increased by 40 basis points (see the blue line in figure 2). Many believe this increase in the 10-year rate was due to Bernanke's comments during the post-FOMC press conference when, in responding to a question about asset purchases, he said it would be appropriate to moderate purchases "later this year" and to end purchases "around midyear" 2014. However, for our purposes, we point out the muted impact Bernanke's answer had on the expected rate paths plotted in figure 1.

Over the next couple of months, changes in the fed funds rate path continued to be minimal even in response to Bernanke's attempt to calm other markets by assuring market participants the Fed was committed to a highly accommodative monetary policy. By the September FOMC meeting—a meeting sometimes referred to as the "untapering" meeting because the Committee decided to "await more evidence that progress will be sustained before adjusting the pace of its purchases"—the expected funds rate path was statistically indistinguishable from the June rate path (see the dashed black line in figure 1). However, the September announcement to delay the tapering of its purchases appeared to have caught bond investors by surprise. In figure 2, we see that the 10-year Treasury rate (the blue line) dropped by approximately 20 basis points over the coming weeks—all while the market's expectation for the timing of liftoff remained relatively constant.

Over the rest of 2013, the pace of the expected rate hikes stayed relatively stable. Figure 1 shows this stability by the similar curvature of the expected path lines from September to December. Interestingly, the December FOMC formal announcement that the Fed would begin to reduce its monthly purchases of Treasuries and mortgage-backed securities (MBS) by $5 billion each did not change the market's expectations for how long it would be before liftoff (see the solid black line in figure 1). We interpret this as market participants having formed their expectations about the future pace of interest rate hikes when the Treasury rates had increased and as policymakers were beginning to talk about tapering and not when the Fed announced the actual date and pace of its shrinkage in asset purchases.

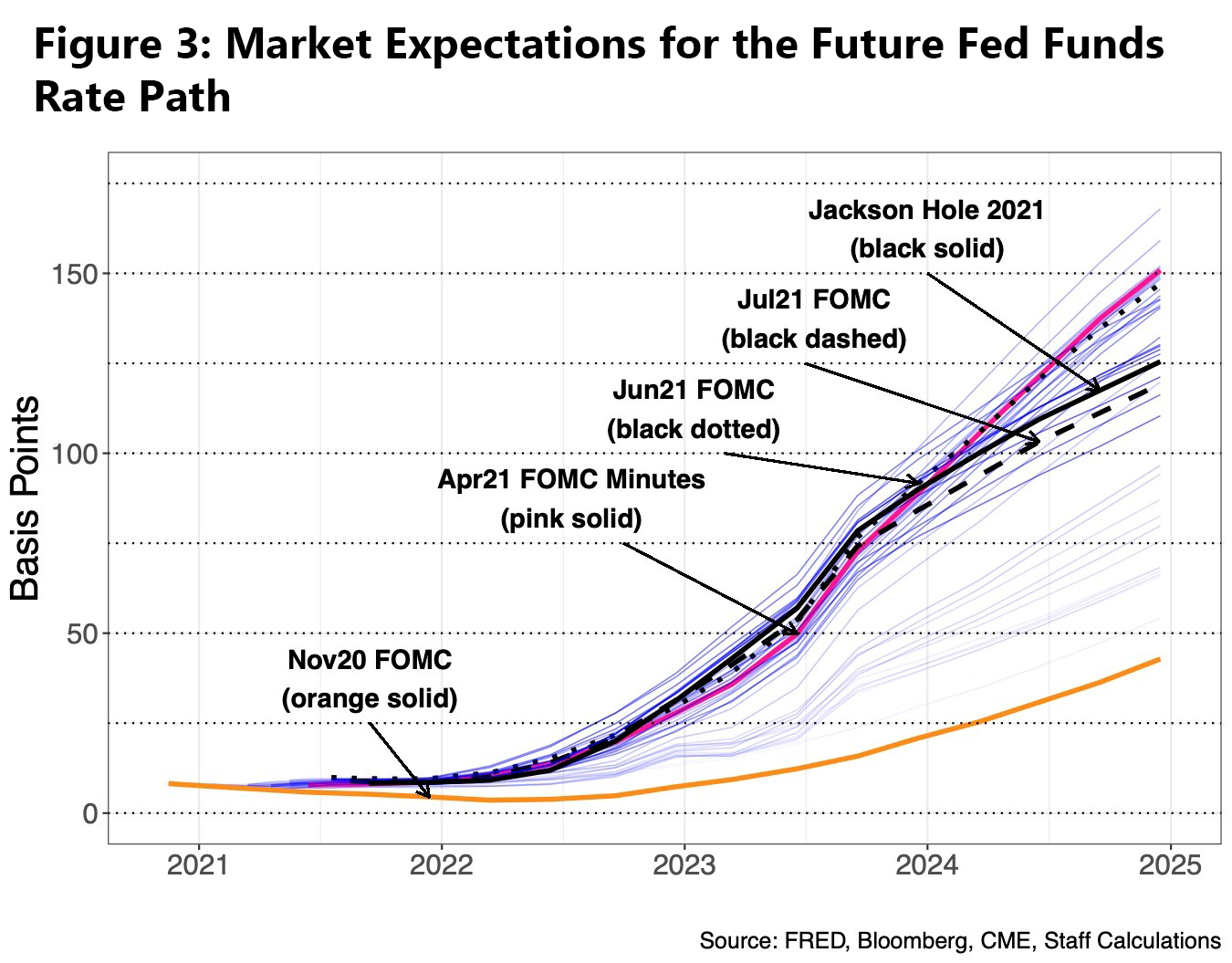

Now compare figure 1 to the sequence of expected rate paths plotted in figure 3 for the time interval of November 5, 2020, to August 11, 2021. Early in this time period, the orange line in figure 2 shows the 10-year Treasury rate increasing 95 basis points from November 2020 to the end of March 2021 (the high point of the orange line in figure 2). This increase in the 10-year rate was due in part to the improving economic conditions and optimism around the advent of COVID-19 vaccines. This time period also corresponds with a steepening in the market expectations for the fed funds rate path seen in figure 3. The "lower for longer" policy of the Fed can be seen in the flat November FOMC rate path (compare the orange rate paths in figures 1 and 3). But as in figure 1, the expected rate paths in figure 3 gradually steepen while the 10-year rate is increasing.

Note: The fed funds rate path was computed from daily option data on Eurodollar futures contracts from November 5, 2020, to August 27, 2021. Each unlabeled line represents the market's expected path for monetary policy given the data as of Wednesday of the week

The minutes from the April FOMC were released to the public on May 19, 2021 (see the pink rate path in figure 3). These minutes describe several participants suggesting that "it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases." Discussion about shrinking the monthly purchases of assets continued into the June 2021 FOMC meeting. Importantly, at the June FOMC press conference, Fed chair Jerome Powell responded to a question about the timeline for reducing asset purchases by saying that people can think of the June meeting as the "talking about talking about" meeting.

The market's expectation about the fed funds rate path to this taper chatter was muted. Market expectations for the first rate hike had already moved up from the middle of 2024 to the first half of 2023. Given the similarity in the paths at the FOMC meetings in June (see the dotted black line in figure 3) and July (the dashed black line in figure 3), and after Chair Powell's Jackson Hole speech (the solid black line), market participants did not alter their expectations about liftoff. Not even the June FOMC's hawkish Summary of Economic Projections affected the views of market participants on the future course of interest rates.

Comparing the sequence of 2013 and 2020–21 rate paths plotted in figures 1 and 3, we might believe that those who think tapering in 2021 will lead to a similar market reaction as in 2013 are right—but only in the sense that both events corresponded to a sizeable increase in the 10-year Treasury rate and not the actual taper.

That being said, after the rate paths in figures 1 and 3 steepened, the limited impact that taper talk had on the rate paths lends support to those who expect tapering to be a nonevent. The relatively constant pace of expected rate hikes found in 2013 and 2021 suggests that a formal announcement by the Fed on reducing its purchases of Treasuries and agency MBS will likely have a limited effect on the market expectations for the pace of future rate hikes. This is especially true for the 18- to 24-month time horizon of the rate paths.

Regardless of whether we believe that there will or will not be a "taper tantrum" similar to the one in 2013, the market expectations calculated from the Eurodollar futures market clearly show two common effects from the events of 2013 and 2020–21. The first is that as the 10-year Treasury rate begins to rise, market participants expect the Fed to start raising the fed funds rate earlier than before. The second effect is that after the first effect, the expected pace of future rate hikes does not appear to be very responsive to taper talk. Hopefully, knowledge of these tapering-related empirical regularities will help market participants form more accurate predictions about future interest rate policies.

By Mark Jensen, a vice president and senior economist in the Atlanta Fed's Research Department and

Brian Robertson, a quantitative financial markets adviser, also in the Atlanta Fed's Research Department