A new paper ![]()

![]() from the Kansas City Fed asks the question, why are U.S. card fraud rates higher than those of other developed countries? Economist Fumiko Hayashi found that even after EMV migration in 2015, the U.S. had a significantly higher in-person card fraud rate than did Australia, France, and the United Kingdom. In all three years studied—2012, 2015, and 2016—the U.S. in-person fraud rate was more than three times higher than that of the other countries (see the chart).

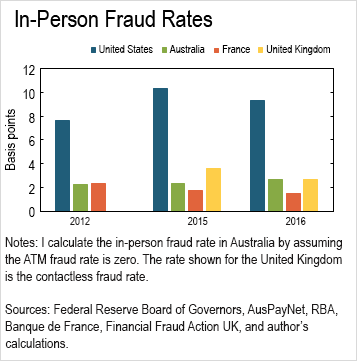

from the Kansas City Fed asks the question, why are U.S. card fraud rates higher than those of other developed countries? Economist Fumiko Hayashi found that even after EMV migration in 2015, the U.S. had a significantly higher in-person card fraud rate than did Australia, France, and the United Kingdom. In all three years studied—2012, 2015, and 2016—the U.S. in-person fraud rate was more than three times higher than that of the other countries (see the chart).

She attributes these differences to three factors:

- The United States had a smaller share of chip transactions. EMV migration in the United States didn't really begin until 2015, compared to years (even decades) earlier for the other countries. According to the Federal Reserve Payments Study, 2 percent of in-person general-purpose card payments used chip authentication in 2015; that share increased to 57 percent in 2018.

- The other three countries use the multi-factor chip-and-PIN verification, which is a stronger method than what U.S. networks use: most chip transactions are chip only. For in-person general-purpose card payments in the United States in 2018, the Federal Reserve Payments Study found that 21 percent (17.8 billion payments) used chip-and-PIN.

- U.S. cardholders are more likely to use credit cards, which typically have higher fraud rates than debit cards.

Hayashi's paper gives a snapshot of the four countries at three points in time. Another approach to doing a country-to-country comparison would be to make a moving picture depicting the aftermath of the adoption of EMV chips for in-person payments. My Retail Payments Risk Forum colleague Doug King, in a paper published ![]() in June 2019, looked at the change in in-person fraud for Australia, France, and the United Kingdom and found that fraud rates for in-person transactions dropped after chip-and-PIN implementation. You can see in the figure above that U.S. in-person card fraud rates declined from 2015 to 2016, over the time of EMV implementation here.

in June 2019, looked at the change in in-person fraud for Australia, France, and the United Kingdom and found that fraud rates for in-person transactions dropped after chip-and-PIN implementation. You can see in the figure above that U.S. in-person card fraud rates declined from 2015 to 2016, over the time of EMV implementation here.

Keep in mind that this post is a simplification of two complex papers. For example, Hayashi also analyzed remote card fraud rates. And Doug included some data from other nations. If you want more information, the Federal Reserve Payments Study has reported details on fraud for noncash payments ![]()

![]() in the United States, cards included, and also authorization methods for in-person general-purpose card payments (see figure 6 in the 2019 Federal Reserve Payments Study

in the United States, cards included, and also authorization methods for in-person general-purpose card payments (see figure 6 in the 2019 Federal Reserve Payments Study![]() ). I invite you to read these reports.

). I invite you to read these reports.

By Claire Greene, a payments risk expert in the Retail Payments Risk Forum at the Atlanta Fed

By Claire Greene, a payments risk expert in the Retail Payments Risk Forum at the Atlanta Fed