In 2021, the five major firms offering buy now, pay later (BNPL) loans originated approximately 180 million loans, with a total value of $24.2 billion and an average value of $135. That's according to a long-awaited report ![]()

![]() on the US BNPL industry from the Consumer Financial Protection Bureau (CFPB). This report resulted from an increasing number of consumer complaints about BNPL, primarily about fee disclosures and problems with merchandise returns, and requests from some congressional figures. (Read my August 1, 2022, post on BNPL for a refresher on what led to the report.)

on the US BNPL industry from the Consumer Financial Protection Bureau (CFPB). This report resulted from an increasing number of consumer complaints about BNPL, primarily about fee disclosures and problems with merchandise returns, and requests from some congressional figures. (Read my August 1, 2022, post on BNPL for a refresher on what led to the report.)

The full report provides detailed information about the state of the BNPL industry in the United States over the 2019–21 period. Here are some other findings in the report that I found interesting:

- While the apparel and beauty sectors still dominate the markets that BNPL lenders serve, their share dropped from 80 percent in 2019 to 59 percent in 2021. Personal effects—which include electronics, fitness and sporting equipment, games and hobbies, and jewelry—made up the second largest segment, at 11 percent of the market.

- From an underwriting standpoint, 73 percent of the BNPL offers in 2021 were approved, with a charge-off rate of 3.8 percent, up from 2.9 percent in 2020.

- By the end of 2021, three of the five lenders were imposing late payment fees, which were in the $7 to $8 range. A fourth lender had charged late fees for most of 2021 but discontinued them in the fourth quarter. For the three firms still charging late fees at the end of the year, about 12 percent of borrowers incurred at least one late fee in 2021, and 7 percent of loans incurred at least one late fee.

- Late fees represented on average 0.28 percent of the BNPL firms' gross merchandise sales.

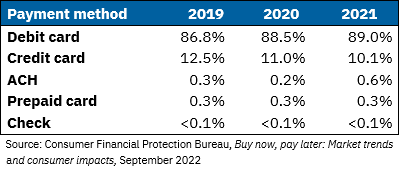

- As the chart shows, debit card dominates the payment methods, while check, at less than one-tenth of 1 percent, is the least frequent choice.

- In 2021, only 60 percent of the dollar value of the merchandise value returned or disputed was refunded, up from 45 percent in 2019. This has been a major source of customer complaints.

- Discount fees paid by merchants have dropped steadily since 2019 as additional BNPL firms have entered the market. In 2019, the average discount fee was 3.39 percent. It was 2.91 percent in 2020 and 2.49 percent in 2021.

We will report on the business trends cited in the report as well as the CFPB's planned next steps in our next post on this subject.

By David Lott, a payments risk expert in the Retail Payments Risk Forum at the Atlanta Fed