The Community Reinvestment Act (CRA)![]() was enacted by Congress in 1977 to encourage depository institutions to help meet the credit needs of the communities in which they operate, including economically distressed neighborhoods, consistent with safe and sound operations. Quantifying the economic impact of the CRA on low- and moderate-income (LMI) communities in a particular city or neighborhood is challenging due to the lack of consistent reporting on community development lending and investment. A recent report

was enacted by Congress in 1977 to encourage depository institutions to help meet the credit needs of the communities in which they operate, including economically distressed neighborhoods, consistent with safe and sound operations. Quantifying the economic impact of the CRA on low- and moderate-income (LMI) communities in a particular city or neighborhood is challenging due to the lack of consistent reporting on community development lending and investment. A recent report ![]()

![]() from the Congressional Research Service notes the difficulty of determining the extent to which CRA incentives influence bank lending and investment in LMI markets relative to other financial and contextual factors. A comprehensive collection of essays

from the Congressional Research Service notes the difficulty of determining the extent to which CRA incentives influence bank lending and investment in LMI markets relative to other financial and contextual factors. A comprehensive collection of essays ![]()

![]() from the Boston and San Francisco Federal Reserve Banks provides commentary and empirical research on the topic.

from the Boston and San Francisco Federal Reserve Banks provides commentary and empirical research on the topic.

This article addresses two common questions from community development practitioners:

- Geographies: Where are banks motivated by the CRA to engage in community development?

- Tactics and tools: What common tactics and tools do banks use to meet CRA obligations?

Geographies

CRA assessment areas (AAs)![]() connect a bank's community development lending, investment, and services to specific geographic areas. In general, CRA AAs are the places where banks are motivated by the CRA to engage in community development. Each bank's community development priorities, strategies, and tactics result from the interaction of two factors: (1) the physical proximity or presence of its main office, branch, deposit-taking ATM, or concentrations of loans originated or purchased by the bank and its competitive position in that particular market and (2) defined characteristics of economic distress or LMI credit conditions.

connect a bank's community development lending, investment, and services to specific geographic areas. In general, CRA AAs are the places where banks are motivated by the CRA to engage in community development. Each bank's community development priorities, strategies, and tactics result from the interaction of two factors: (1) the physical proximity or presence of its main office, branch, deposit-taking ATM, or concentrations of loans originated or purchased by the bank and its competitive position in that particular market and (2) defined characteristics of economic distress or LMI credit conditions.

As such, CRA assessment areas consist of one or more contiguous political subdivisions, such as counties, cities, or towns (or census defined metropolitan statistical areas/divisions). AAs are continually in flux and there is no central source for up-to-date location data on current ones. Each regulated bank is responsible for choosing its AAs and must review and affirm that choice each year. Any given bank's current AAs are public information and are sometimes (but not always) listed on a bank's website.

At the outset of a CRA exam—which depending on the size and circumstances of the institution may occur every two to four years—a bank provides examiners with its AAs. During the exam process, examiners check to ensure that AAs do not arbitrarily exclude LMI areas. Then, within a bank's assessment areas, examiners determine the extent to which the bank's community development lending, investment, and services are geared to the community development needs defined in that particular local context. Regulators adopted a set of Questions and Answers ![]()

![]() in late 2013 to address community development activities outside a bank's assessment areas in a broader statewide or regional area. However, CRA is fundamentally a place-based tool focused on a bank's AAs.

in late 2013 to address community development activities outside a bank's assessment areas in a broader statewide or regional area. However, CRA is fundamentally a place-based tool focused on a bank's AAs.

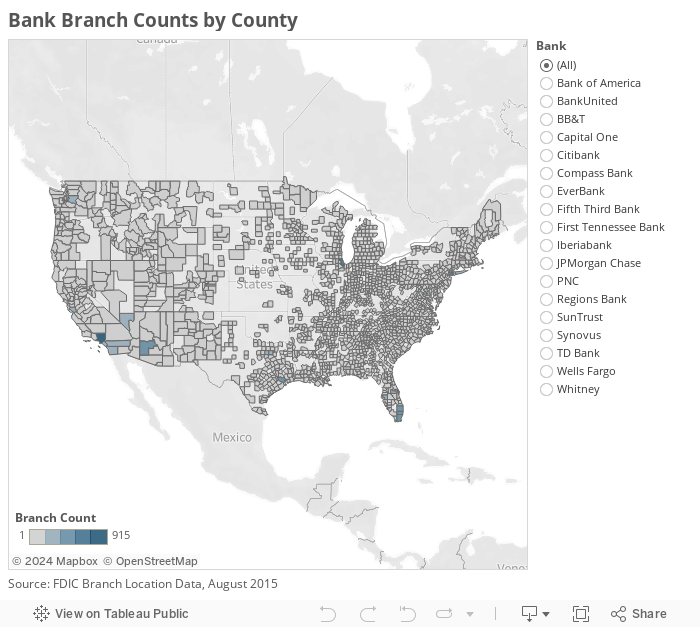

The mapping tool illustrates, generally, the geographies where a select group of banks are motivated to engage in community development. (These particular banks are those making up the top 20 in terms of deposit market share in the Atlanta Fed's Sixth District.) As previously discussed, AAs are geographic areas corresponding to the places where a bank has a business presence. Therefore, this tool illustrates the relative density of a bank's branch presence at the county level using FDIC branch location data from August 2015. These data approximate the geographies of CRA for a select group of banks.

Strategies and tactics

Next, within a bank's AA, examiners assess performance across three main activities: lending, investment, and services. For banks of all asset sizes, examiners consider the bank's retail lending performance relative to demographic data and the aggregate of all lenders in the market. For larger institutions (those over approximately $350 million in assets) examiners also consider the bank's community development lending, investments, and services using both quantitative and qualitative factors. For the largest institutions, retail services (including the geographic distribution of branches across geographies of all income levels) are also reviewed.

Based on a review of a convenience sample of 10 CRA public evaluations, drawn from 20 banks with the largest market share in the Atlanta Fed's Sixth District, these are the most common CRA-motivated activities:

- "Retail" lending for:

- Mortgages, small business, and farm loans to LMI borrowers and in LMI areas

- Community development service to:

- Nonprofit economic or community development entities

- Financial counseling agencies

- Other nonprofit or public boards or commissions

- Community development lending to:

- Community development financial institutions (CDFIs) for affordable housing development and small business loans

- Not-for-profit community development corporations or economic development corporations, usually for real estate acquisition or development

- Local and regional loan funds supporting small businesses or entrepreneurs

- Private developers of affordable housing

- Private developers of multifamily housing in cases where bank can justify need through performance context

- Qualified investments (with expectation of financial return) in:

- Residential mortgage-backed securities—Government and Federal National Mortgage Associations ("targeted")

- Low-income housing tax credits and new market tax credits (direct and through participation in funds)

- State-issued Federal Housing Administration and Housing and Urban Development bonds

- Private activity bonds, that is, municipal bonds for community development

- Small Business Administration 504 securities

- Small business investment corporations and small business loan pools

- Deposits in credit unions that serve LMI populations

- Qualified investments (grants; without expectation of financial return) in:

- Charitable foundations

- Community development corporations

- Nonprofits engaged in community development activities

- Training/capacity building

- Foreclosure prevention programs

- Financial literacy programs

The next article in this series will describe the approximate scale of CRA-motivated lending and investment in the Atlanta Fed's region. General resources on the CRA are available from the Federal Financial Institutions Examination Council (FFIEC![]() ) or through the regulatory agencies:

) or through the regulatory agencies: