Housing plays a critical role in the U.S. economy. For individuals, owning a home may be their most valuable asset. Home ownership helps meet the basic need of shelter and can support economic mobility (through wealth accumulation) and resilience (stability). However, rising home prices and rents have also led to concerns about housing affordability.

Several tools have been developed to provide insight into the extent of the affordable housing challenge. The Atlanta Fed's Southeastern Rental Affordability Tracker provides a point-in-time assessment of the number of households by income category and available rental units by price point to estimate the number and share of cost-burdened renter households and available and affordable units. Other tools show measures of housing affordability over time.* No tool is all-encompassing; there is always a trade-off between the level of detail (both the comprehensiveness of data and its granularity) provided and the frequency of update.

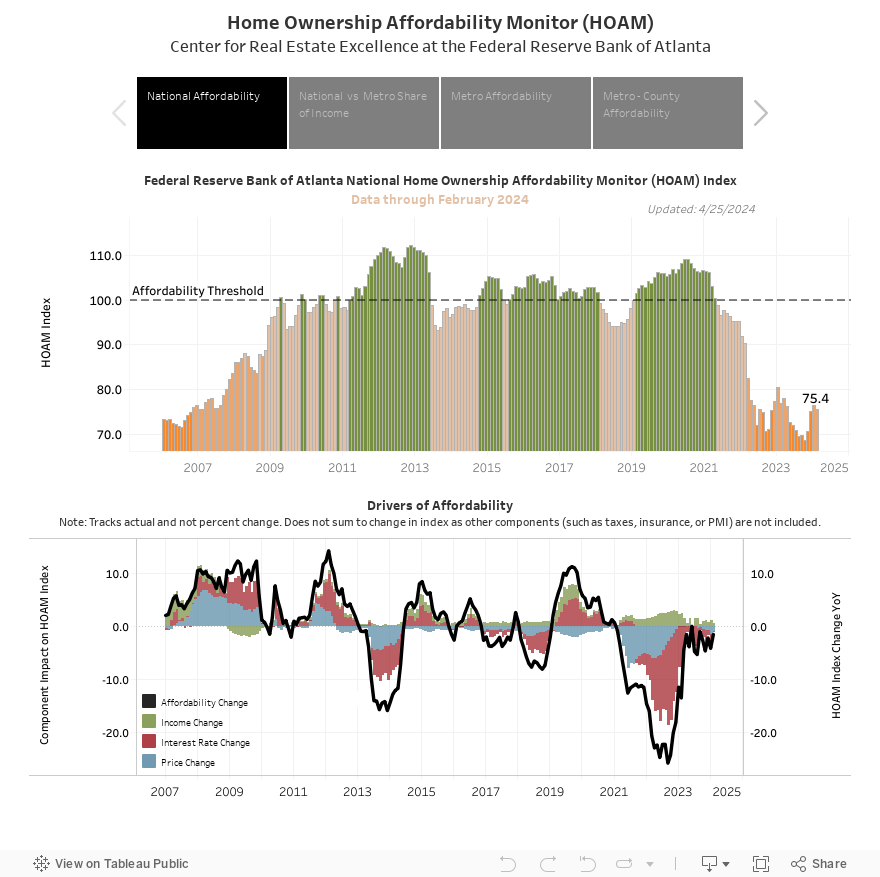

To help business economists and analysts track the relative changes in home ownership affordability at a higher frequency and more granular level of geography, the Atlanta Fed developed an interactive home affordability tool, the HOAM (Home Ownership Affordability Monitor) Index, which measures the ability of a median-income household to absorb the estimated annual costs associated with owning a median-priced home. Using the HUD standard 30 percent share of income threshold to measure affordability, this tool presents a national view of affordability for the median home owner from January 2006 through the most current data as well as metro-level and county-level (within metropolitan areas) views of affordability for the median home owner from January 2014 through the most current data.

The contribution of this tool lies at the intersection of three important factors: (1) it provides a view of the costs associated with home ownership (2) at a higher frequency (monthly), and (3) at finer levels of geography (down to the county level within metropolitan areas).

Stay informed of all HOAM updates by subscribing to our mailing list, subscribing to our RSS feed ![]() , or following the Atlanta Fed on Twitter.

, or following the Atlanta Fed on Twitter. ![]()

* Examples include the widely cited National Association of Realtors' Housing Affordability Index, the affordability map produced by the Joint Center for Housing Studies of Harvard University, the Urban Institute's Housing Affordability for Renters Index, the National Association of Home Builders/Wells Fargo Housing Opportunity Index (HOI), the HUD Exchange Location Affordability Index, the Center for Neighborhood Technology's Housing and Transportation Affordability Index, the U.S. Home Affordability Heat Map produced by ATTOM Data Solutions, and the RealtyHop Housing Affordability Index, to name a few.