Selling goods and services abroad can offer small businesses the opportunity to reach new markets and expand their base of customers. This can boost a firm's revenues and profits, which can necessitate expansion and job growth. Encouraging export businesses can thus be an effective part of a region's economic development strategy, and it can boost economic growth. However, having adequate access to financing is often necessary for small businesses that aim to expand their operations, including firms that want to expand their global reach.

This article presents data from the Federal Reserve System's 2017 Small Business Credit Survey1 (SBCS) that offers insights on small exporting firms and their experiences in the market for credit.2 The survey includes responses from 8,169 employer firms, 1,018 of which are exporters, and it polls 5,553 nonemployer firms (firms that do not have employees), 302 of which identify as exporters. As such, exporting firm respondents are overrepresented in the SBCS when compared with the general population of U.S. businesses, though the survey's weighting structure reduces that bias.

Small exporting firms

In 2017, the U.S. Census Bureau identified 284,168 U.S. firms as exporters. In 2016, just over 166,000 exporters were small businesses that employed between one and 499 workers. Such small employer exporters make up only about 3.2 percent of the country's 5.1 million small firms.3

An additional 114,000 exporting businesses were self-employed, had missing employment data, or had no employees on payroll at some point in 2016. Together, small employer and nonemployer export firms contributed about 35.7 percent of the known value of all export firms, some $461.3 billion in 2017, with most of these businesses operating in the manufacturing (24.8 percent) and wholesale (33.4 percent) industries.4 While small (57.8 percent) and nonemployer businesses (39.7 percent) make up the vast majority of exporting firms, large firms actually make up a relatively large share of exporters (2.5 percent) compared with their share of all U.S. firms (0.4 percent).

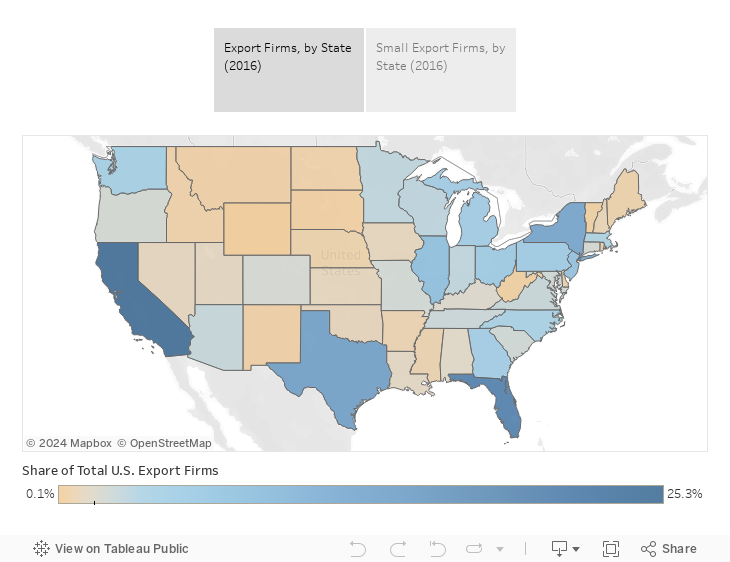

Export firms tend to cluster in certain areas of the country. In fact, just four states, California, Florida, Texas, and New York, house over two-thirds (69.8 percent) of all small exporting firms, and a slightly lower share of all U.S. export firms (see Tableau map and table 1 in the Appendix, download here). Other states with relatively large shares of exporting firms (compared with their share of the U.S. population) include Illinois, New Jersey, Michigan, Washington, and Ohio.

Export firms' profitability

Based on SBCS data, small exporting businesses were more likely to indicate they were profitable than small firms that do not export. This is particularly the case among firms with employees. Sixty-four percent of exporting employer firms were profitable at the end of 2016, compared to 57 percent of nonexporters (see chart 1). A similar difference exists between exporting and nonexporting firms that do not have employees. Fifty-two percent of nonemployer firms that export report they were profitable, compared with 43 percent among those that didn't export.5

Credit market experiences of small exporting firms

As previously noted, additional capital in the form of financing or cash is often necessary for firm growth. Also, certain specialized credit products offered by financial institutions are important to mitigate the risks involved when firms engage with foreign partners. One estimate shows that globally, 36 percent of trade was financed by bank-intermediated credit or credit insurance in 2009.6 The Bank of International Settlement's Committee on the Global Financial System similarly estimates this at about a third of global trade.7 However, in a 2010 survey U.S. businesses cited obtaining financing as one of the most burdensome impediments to trade, and this was particularly the case among small and medium-sized enterprises. Over 40 percent of small firms cited financing as a burdensome impediment, compared with just around 10 percent of large firms.8 Although the Great Recession may have affected the survey findings, the differential between small and large firms is notable.

For exporters in the United States, letters of credit and documentary collections are the predominant bank-intermediated finance vehicles to finance trade. These covered about $153 billion, or 10 percent of U.S. exports in 2012 (Niepmann and Schmidt-Eisenlohr, 2014).9 While the SBCS does not inquire about these products in particular, the survey does ask broader questions that provide a clearer indication of what export firms experience when applying for financing.

Financing application rate and personal funds

A somewhat larger share of exporting employer firms reported they applied for credit than those that do not export: 43 percent compared with 39 percent. The overall share of firms that applied for credit across the United States was 40 percent.10 Additionally, export firms are less likely to rely on the owners' personal funds: just 14 percent of exporting firms do so, compared to 19 percent among nonexporters. There is no substantial difference in the share of firms that applied for financing between exporting and nonexporting businesses that have no employees: about 25 percent and 24 percent, respectively.

Financing amount

Based on SBCS responses, export firms seek significantly larger amounts of financing. About 28 percent of export firm applicants applied for between $250,000 and $1 million in financing, and 13 percent applied for over $1 million, compared with 16 and 7 percent, respectively, among nonexporting applicants (see chart 2). Of nonexporting applicants, 22 percent applied for less than $25,000 in financing, and 35 percent applied for between $25,000 and $100,000, compared with 10 and 28 percent, respectively, among export firms. As a result, exporting firms, including those that did not apply for financing in the previous year, report significantly larger amounts of outstanding debt. About 14.5 percent of small exporters have over $1 million in outstanding debt, while only 7.6 percent of small nonexporters do.

There are similar trends among self-employed exporters. For example, about 16 percent apply for between $250,000 and $1 million in financing, compared with just 7 percent of nonexporting nonemployer firms. Just 27 percent apply for less than $25,000, compared with 48 percent of nonexporters. Finally, outstanding debt amounts among exporting nonemployer firms are significantly greater as well.

Sources of financing

There are significant differences in the type of lenders export firms turn to. These businesses less frequently turn to smaller banks to obtain financing, and similarly less frequently apply to community development financial institutions (CDFIs). For instance, 54 percent of exporting applicants turned to large banks, compared with 48 percent of nonexporting firms;11 just 41 percent applied at a small bank, versus 47 percent of nonexporting businesses that did so; and just 2 percent turned to CDFIs, compared with 6 percent of nonexporting employer firms (see chart 3). Interestingly, a significantly larger share of export firms receive approval for at least some of the financing they apply for at large banks: 66 percent, compared to just 55 percent among nonexporting firms.

Among nonemployer firms, these differences in where firms turn for financing are less pronounced. A smaller share of nonemployer exporters turn to CDFIs: 3 percent do so, compared with 6 percent among nonemployers that do not export. Additionally, a larger share appear to turn to online lenders: 38 percent apply at these lenders, compared with 30 percent of nonemployers that do not export.12

One reason for the relatively muted roles of small banks and CDFIs compared with large banks could be because offerings of specialized trade financing products are highly concentrated. Niepmann and Schmidt-Eisenlohr (2014) found that in the United States in 2012 just five banks accounted for 92 percent of trade guarantees, and "there is a strong positive relationship between the probability of having non-zero trade finance claims and bank size." In fact, globally, just 21 banks supplied 11 percent of the finance needs for international trade in 2011.13 Also, since exporting firms appear to be applying for significantly larger amounts of financing, large banks could potentially better handle the greater risk to their loan portfolios.

Finally, while the role of small and community banks in export finance has historically been minor, factors such as technological advances in processing letters of credit, a growing need to offer a full suite of services to retain clients, and programs by the Small Business Administration and the Export Import Bank contribute to increased engagement by smaller banks in financing international trade.14

Conclusion

The Small Business Credit Survey shows that small export businesses exhibit several significant differences from those that do not sell goods or services abroad: a larger share are profitable, they apply for larger amounts of credit and carry greater amounts of outstanding debt, a smaller share apply at small banks and CDFIs, and they experience higher approval rates at large banks.

The 2018 SBCS will allow us to examine changes over time, and it contains additional questions that could clarify how export businesses experience the impact of recent changes in federal trade policy.

By Mels de Zeeuw, senior CED research analyst

_______________________________________

1 The Small Business Credit Survey (SBCS) is an annual convenience survey of small businesses with fewer than 500 employees conducted by all 12 of the Federal Reserve System's regional banks. The survey examines financing needs, decisions, and outcomes for these firms, and the data are weighted to be representative of the entire one- to 499-employee firm population in the United States for employer firm respondents, and of the U.S. nonemployer firm population for respondents who do not have employees.

2 The SBCS asks firms whether they exported "any goods and/or services outside the United States" in 2016, which allows us to identify export firms.

3 Small businesses or firms hereafter refers to businesses with between one and 499 employees, or nonemployers. U.S. Census Bureau, Business Dynamics Statistics, 2016. U.S. Census Bureau, Profile of U.S. Importing and Exporting Companies: 2015–2016.

4 U.S. Census Bureau, Preliminary Profile of U.S. Exporting Companies, 2017.

5 This difference is not statistically significant.

6 World Trade Organization. 2016. "Trade Finance and SMEs: Bridging the Gaps in Provision."

7 Clark, J. 2014. "Trade Finance: Developments and Issues," Committee on the Global Financial System (CGFS) publication no. 50. Basel: Bank for International Settlements.

8 United States International Trade Commission (USITC). 2010. "Small and Medium-Sized Enterprises: Characteristics and Performance" Investigation no. 332-510, USITC publication no. 4189, November. https://www.usitc.gov/publications/332/pub4189.pdf.

9 Niepmann, F. and Schmidt-Eisenlohr, T. 2014. "International Trade, Risk, and the Role of Banks," Federal Reserve Bank of New York Staff Report no. 633. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr633.pdf.

10 The difference in financing application rates between exporting and nonexporting firms is not statistically significant.

11 This difference is not statistically significant.

12 Ibid.

13 Clark, J. 2014. "Trade Finance: Developments and Issues."

14 Holod, D. and Torna, G. 2016. "Community Banks Play an Important Role in International Trade," The CLS Blue Sky Blog (Columbia Law School's Blog on Corporations and the Capital Markets). http://clsbluesky.law.columbia.edu/2016/11/18/community-banks-play-an-important-role-in-international-trade/.