Economic shocks are known to hit low-income individuals and communities the hardest, and their recoveries take the longest. The same is true for the organizations supporting these communities, but that story often gets lost. The risk, then, becomes that the very infrastructure that provides necessary services for economic resilience and mobility—programs for youth, homelessness support, and job training, for example—is defunded or drained of critical capacity when it's most needed. Service providers across the Southeast are already expressing these risks and concerns. They expect recovery in communities they serve will take longer than 12 months after the end of the pandemic, but are also concerned that their organizations will hit financial hardship in the next six months. If these conditions occur, recovery in low-income communities will be made even more difficult to achieve.

A national Federal Reserve survey hopes to keep a spotlight on this risk and provide policymakers and civic leaders with information to shape solutions. The survey polls representatives of nonprofit organizations, financial institutions, government agencies, and other community organizations approximately every eight weeks on the impact of COVID-19 on low- to moderate-income communities, with results released in regular reports.1

This article highlights data from the June survey in which we received more than 250 responses from the states in the Atlanta Fed's District—Georgia, Florida, Mississippi, Alabama, Tennessee, and Louisiana.2

Economic headwinds expected to persist for low-income communities

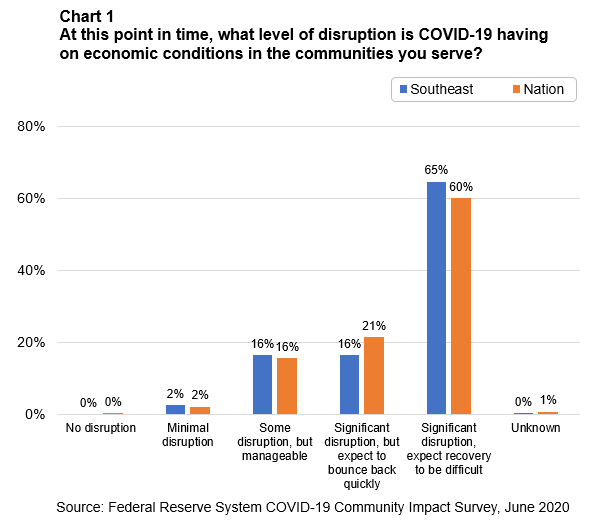

The survey starts by asking questions about the communities the respondents serve. For 65 percent of southeastern respondents, COVID-19 was having a significant disruption on the economic conditions of the communities they serve, and they expect that recovery will be difficult (see chart 1). This was 5 percentage points higher than the national sample. More than half of southeastern respondents named income loss as a top impact of the pandemic. Nationally, 42 percent of respondents shared it as their primary concern. This disparity in the Southeast versus national responses may be because many jobs in the Southeast are in the tourism and hospitality industries, both of which have been deeply affected by COVID-19.

Compared with the April survey, respondents were more pessimistic about communities' ability to bounce back. When asked "How long do you expect it will take the people and communities you serve to return to the conditions they were experiencing before the impact of COVID-19?" over 46 percent of national respondents said it would be more than 12 months. This is an 11 percentage point increase from the April poll, in which only 35 percent of respondents expected a recovery period longer than 12 months. Responses from the Southeast matched the national trend. It is clear that many organizations expect to be dealing with the impacts of COVID-19 for a long time. In addition, simply returning to a pre-COVID-19 condition would still leave many low- and moderate-income families deeply challenged.

Understanding organizational strains and challenges

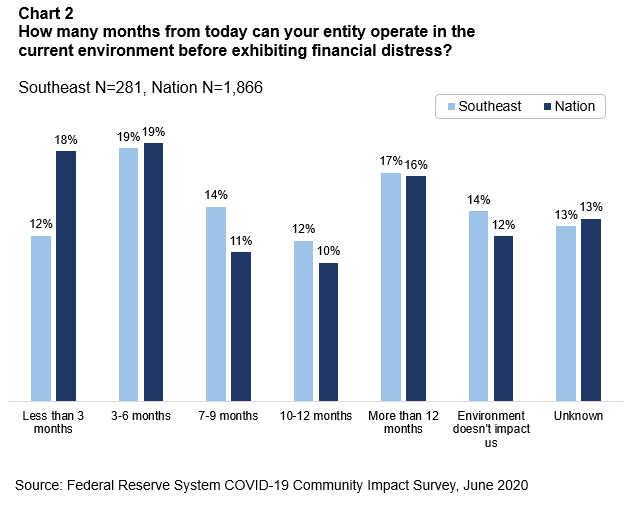

Over half of respondents in the Southeast said that COVID-19 is a significant disruption to the entity they represent, with only 31 percent expecting to bounce back quickly after recovery begins. While many southeastern respondents see over a year of economic disruption ahead of them, 12 percent indicated that their organization could operate for less than three months in the current environment before experiencing financial hardship that could result in reducing services, layoffs, closing locations, or closing entirely. Nearly a third of respondents in the region cannot last more than six months. Chart 2 displays these findings, comparing the Southeast to national trends.

These findings highlight a significant challenge for the ecosystems that support individuals and families, including nonprofit organizations, local government, and other community-based organizations. These entities are at the front lines of responses to this or any crisis. These organizations are providers of essential services such as helping laid-off workers get reemployed; small businesses retool and access necessary capital; or families figure out a strategy to get caught up on accumulated bills, rent, and mortgage payments. Without access to these supports, some communities may be left out of the economic recovery.

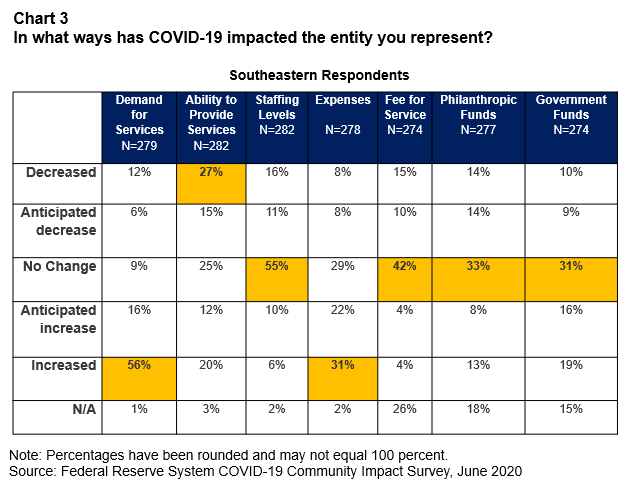

Chart 3 provides a closer look at the various strains that organizations are facing in the Southeast. As you can see, 27 percent of respondents noted a decrease in their ability to provide services, but 56 percent reported an increase in demand for services—an almost 30 percent gap. When asked about funding, respondents told us that few additional funding sources had surfaced as of June, with 28 percent anticipating or already experiencing a decrease in philanthropic funding. At the same time, 16 percent of organizations anticipated an increase in government funds, but that remained to be seen as many municipalities have been hard hit by budget shortfalls.

The factors reducing the organizations' ability to provide services are varied. Southeast respondents told us staffing levels overall are down 16 percent and they are expected to decline another 11 percent. In speaking with some community partners, we heard that the reasons for this staffing reduction include layoffs, staff attention being divided as they have taken on supporting their own children's remote education, and volunteers no longer working because they are uncomfortable or prohibited from providing support because of social distancing protocols.

In addition, 31 percent of these service providers across the Southeast reported rising expenses, and another 22 percent anticipate future increases in expenses. These increased costs may be driven by public health–mandated social distancing practices, making the delivery of some services slow, inefficient, and costlier as organizations acquire personal protective equipment and alter their physical environments. In some cases, these things might make service delivery impossible.

The work ahead: creating an equitable recovery

These challenges suggest that recovery will not be easy. Equitable and inclusive recoveries require cross-sector collaboration and the testing of new ideas. That effort will require government, philanthropy, direct service providers, and the private sector to hear from and engage individuals and communities that are affected to help with stabilization and recovery.

This survey documents a real need to assist front-line organizations. This support can come in many forms. For instance, organizations working in underserved communities sometimes partner with banks that are looking for opportunities to satisfy Community Reinvestment Act (CRA) requirements. In response to the pandemic, there has been a joint statement from the three regulatory agencies expanding their geographic service areas and encouraging other activities that are eligible for CRA investments. In Florida, for example, we have heard of new investments to front-line organizations and small businesses. In Atlanta, we have seen philanthropic investment from organizations such as United Way and the Atlanta Community Foundation to help address the current challenge.

As the public health crisis unfolds and we begin to move toward recovery, the Atlanta Fed's community and economic development (CED) program remains committed to identifying opportunities to work alongside policymakers, practitioners, funders, and researchers to support a coordinated COVID-19 response strategy that promotes long-term economic mobility and resilience in communities. We can do that by providing research, making data available and practical, helping improve networks, and sharing promising practices. When we have presented these results to leaders in the Southeast, they have said the information provides useful context and guidance around their work. Higher response rates from entities in the Southeast will allow us to offer more detailed information on the particular challenges, and promising solutions, within the region. We encourage you to subscribe to the survey at frbatlanta.org/forms/community-development/publications/subscribe-national-covid-19-survey.aspx and add your voice to the results. You are also invited to check out our resources and reach out to us as we all work toward recovery.

By David A. Jackson, senior CED adviser, and Jasmine Burnett, CED research analyst II

_______________________________________

1 The information in this article references data from the second round of survey results, collected from June 3 to 12, 2020. We received a total of 1,869 responses nationally. Respondents were primarily nonprofits and governments, with that group representing 58 percent of respondents nationally and 78 percent in the Southeast. While the majority of respondents nationally serve urban areas (63 percent), in the Southeast it is more evenly divided between urban (38 percent), suburban (32 percent), and rural (30 percent) service areas. Nationally and in the Southeast, 71 percent of respondents are direct service providers. They work across a variety of issue areas, including affordable housing; technical assistance support and lending to small or microbusinesses; job training; financial education and services; education; and health and basic public services. In the Southeast, respondents were most likely to report working in housing (63 percent), public and community service (47 percent), and workforce development/job (33 percent) issue areas.

2 The responses from the Southeast region were heavily concentrated in Florida and Georgia, our two most populous states. The results presented in this chart reflect an unweighted analysis of regional responses.