The COVID-19 pandemic has resulted in both a major public health crisis and a major economic crisis. The economic impact is coming primarily via social distancing (or stay-in-place) restrictions that have resulted in the temporary closing of nonessential businesses in many parts of the country. As a result, millions of workers have been laid off or furloughed. Unemployment claims for the week ending March 21 totaled more than 3 million—the highest number of seasonally adjusted initial claims in the history of the series at that time. That record was broken quickly. For the week ending March 28, the number of seasonally adjusted initial claims increased to over 6 million. By the week ending May 2, the four-week moving average of weekly new unemployment insurance claims was over 4.1 million. In response, Congress has passed two laws that contain measures designed to help individuals affected by this shock: the Families First Coronavirus Response Act (FFCR Act), signed into law on March 18, and the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), signed into law on March 27. In addition, the Coronavirus Preparedness and Response Supplemental Appropriations Act was signed into law on March 6 and provided $8.3 billion in emergency funds to state and local governments to fight the outbreak.

In this Partners Update article, we expand on a recent macroblog post to show how the assistance offered in the acts supplements the preexisting social safety net. Specifically, we ask how the acts and the social safety net financially support a hypothetical displaced American working in a restaurant prior to the outbreak. We present our case study in two locations in the Southeast: Birmingham, Alabama, and Miami, Florida. Overall, the potential impact of these acts depends on the length of the unemployment spell, variation in state unemployment insurance laws, and variation in the cost of living.

Our case study: introducing Chef Andrew

Chef Andrew is a single 25-year-old adult without children. He works full-time in a restaurant, earning the area-specific typical entry-level wage for chefs. On April 1, Andrew's restaurant closed. He is laid off but unable to find another chef job since many other restaurants are also closed or operating in limited capacity.1

What the acts and existing social safety net do

Both acts have a variety of provisions to help those affected by COVID-19, but we focus only on the key unemployment-related components of the acts that benefit workers directly. The analysis excludes provisions that directly incentive employers to retain or rehire workers.2 In addition to the acts, the preexisting social safety net provides assistance to low-income individuals, including those who encounter short-term periods of financial distress. We review the key elements of the acts and the social safety net that are relevant to Chef Andrew:

- Individual receipt of up to $1,200 in tax rebates. The rebate begins phasing out when a single filer's annual income exceeds $75,000.

- A suspension of all payments on federal student loans through September 30 and a pause on the accrual of interest.

- Expansion of unemployment insurance (UI). On top of the regular state UI benefits, the federal government provides an additional $600 per week in federal pandemic unemployment compensation through July 31. After an individual reaches the state's maximum number of weeks on UI, emergency federal UI benefits extend the state UI benefits for up to an additional 13 weeks.

- In Birmingham, Chef Andrew's regular state UI payment is $275 per week for 14 weeks. Florida UI provides a similar amount of unemployment compensation: $275 per week for 12 weeks.

- With the acts, Andrew would have UI benefits for 27 weeks in Alabama versus 25 weeks in Florida.

- The FFCR Act suspends work requirements for determining Supplemental Nutrition Assistance Program (SNAP) eligibility until the declared end of the national public health emergency.

- Without the act, Andrew would have access to SNAP for only three months while unemployed. The act provides possible extended eligibility to the program. The initial amount he receives is small. He receives about $30 per month in Birmingham and $66 per month in Miami (support is higher in Miami than Birmingham because Andrew's income is lower in Miami). However, if he is still unemployed after the maximum duration of UI, the size of the support will be larger in both cities (about $200 per month).

- Medicaid and health insurance subsidies provided by the Affordable Care Act (ACA) help low-income individuals afford health insurance, but the laws vary significantly from state to state.

- When Andrew becomes unemployed, we assume he loses access to employer-sponsored health insurance. Neither Alabama nor Florida has expanded Medicaid under the ACA.3 Without financial support of the acts, Andrew's annual income is below 100 percent of the federal poverty level and he falls into the Medicaid coverage gap—subsidized health insurance from the marketplace is unavailable to him. With the financial support from the acts, Andrew's income is high enough to make him eligible for the ACA subsidies that significantly decrease the costs of health insurance.

The accompanying appendix describes the assumptions and specifics of how each program assists Andrew during his period of unemployment.

A tale of two cities: Birmingham and Miami

The extent to which the FFCR and CARES acts help stabilize a worker depends on state-specific social safety net policies as well as regional differences in wages and cost of living.

Our first case assumes Andrew lives in Birmingham. He earns $37,000 per year before taxes ($3,083 per month), which is the 10th percentile of chef wages in Birmingham. Every month he pays $700 in rent (fair market rent in Birmingham, according to the U.S. Department of Housing and Urban Development), $143 for health insurance (the average cost of employer-sponsored health insurance for a 25-year-old in Alabama, according to the Medical Expenditure Panel Survey), $100 toward his student loans, and $252 for basic groceries (based on the U.S. Department of Agriculture's low-cost food plan for a one-person household).

For comparison, we also show a case where Andrew is an entry-level chef in Miami. He earns $30,108 per year before taxes ($2,509 per month), the 10th percentile of chef wages in Miami. Every month he pays $1,084 in rent (fair market rent in Miami, according to the U.S. Department of Housing and Urban Development), $123 for health insurance (the average cost of employer-sponsored health insurance for a 25-year-old in Florida, according to the Medical Expenditure Panel Survey), $100 toward his student loans, and $252 for basic groceries.4

Putting it all together: Birmingham and Miami

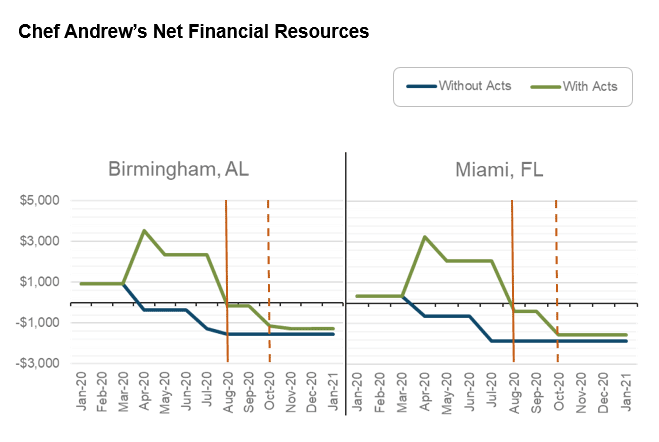

We now show the provisions in the FFCR and CARES acts, along with the preexisting social safety net, combine to support Andrew and help him pay his living expenses. The vertical axis in the following chart shows net resources, which we define as the sum of after-tax income, SNAP, Medicaid, ACA subsidies, and assistance from the two acts, minus the basic expenses affected by the acts and safety net provisions (food, health insurance, rent, and student loan payments). A value of net resources above zero can be thought of as the excess amount of money that can be used to cover additional expenditures.

The chart shows monthly totals of Andrew's net resources from January 2020 to January 2021. We assume his period of unemployment and the distribution of the acts' funds begin in April 2020. We also assume he remains unemployed for 10 months, which is the maximum duration of assistance in Alabama allowed under the CARES Act Pandemic Unemployment Insurance Compensation—27 weeks—and an additional three months of unemployment to illustrate his financial status without any of the acts' financial support. The solid vertical orange bars represent the end of support through the Federal Pandemic Unemployment Compensation; the dashed vertical orange bars represent the end of support for Federal Pandemic Emergency Unemployment Compensation.

Since the dynamics of the net resources over time are complex and depend on changes in individuals' income and expenses over time, we provide a simplified summary here and present a detailed analysis in the accompanying appendix.

Before the crisis, Andrew has about $1,000 of slack in his monthly budget in Birmingham. In Miami, due to the slightly lower wage and higher housing expenses, the net resources measure is slightly above zero ($330), meaning he can barely meet his covered expenses even before he becomes unemployed. Additional costs excluded in this analysis, such as transportation expenses, would result in even greater financial hardship.

When he loses his job in April, the financial assistance from the acts (represented by the green lines in the chart) allows Andrew to cover basic expenses in both cities from April until August. In August, if Andrew is still unemployed, his net resources drop below zero in both cities due to the loss of Federal Pandemic Unemployment Compensation (solid orange bar). In October, he loses Federal Pandemic Emergency Unemployment Compensation (dashed orange bar), reducing net resources even more in both cities.

Note: Solid vertical orange bars represent ending of support through the Federal Pandemic Unemployment Compensation; dashed vertical orange bars represent ending of support for Federal Pandemic Emergency Unemployment Compensation.

Source: The Fiscal Analyzer, authors' calculations

The FFCR and CARES Acts improve Andrew's financial security relative to a world without the passage of the acts. Without the acts (represented by the blue lines), net resources drop below zero as soon as Andrew loses his job and remain negative for the duration of unemployment.

Takeaways for practice

Our case study highlights that the FFCR and CARES Acts provide financial stability for displaced workers in the short term. However, the size and duration of the acts' positive impact will depend on individual circumstances, including their income prior to unemployment, personal savings, state of residency, and household composition. Duration of the crisis also matters. The longer the COVID-19 crisis continues, the greater the financial stress for many households and the greater the call for additional policy action.

We conclude with several takeaways for practice and thoughts for research.

- We assume Andrew receives unemployment assistance under the acts in April, the same month he loses his job. However, the unprecedented increase in claims has overwhelmed some state agency offices and may lead to delays in benefit payments.

- As part of the CARES Act, the Paycheck Protection Program provides small businesses with resources to maintain payroll and hire back workers who have been laid off. If Andrew's employer obtained Paycheck Protection Program loans, it may receive loan forgiveness by quickly rehiring Andrew.

- Provisions in the CARES Act may create opposing incentives for displaced workers to return to work. For example, the Paycheck Protection Program encourages companies quickly to rehire workers, yet generous and extended unemployment benefits may create disincentives for laid-off workers to return to work. The ultimate effect of these two provisions on workers' employment outcomes remains an open question for future work.

- Given the short-term duration of assistance under these acts, practitioners should consider strategies to support displaced workers as they transition back into the workforce. These strategies include identifying occupations and target industries with job openings and projected employment growth. Practitioners can facilitate worker access to job placement services, wraparound supportive services, and short-term retraining programs that leverage employee's transferable skills to new occupations. They also can help employees identify skills transferable to new positions for which they may be qualified.

- Higher typical housing costs in the Miami area place a financial burden on a worker like Andrew, especially during periods of unemployment without the assistance of the acts. Additional financial supports may be necessary to support workers as they transition back into employment.

- Cost-of-living and safety net policies typically vary by family type. Families with children, for example, may face significant financial barriers when seeking to return to the labor force. Related issues, such as the demand for childcare and lack of childcare access, compound these challenges. Developing two-generational programs that support parents and their children will be essential.

- Even with the assistance of the acts, low-income workers may face critical financial gaps due to debt accumulation during the unemployment period and under-enrollment in safety net programs. Low-income workers may accrue debt in the initial weeks of the crisis and before assistance is distributed. In addition, low-income workers may face higher living expenses than we assume in this analysis, creating a need to pay expenses using credit.

By Elias Ilin, research associate at the Atlanta Fed and a PhD candidate at Boston University, John Robertson, senior policy adviser in the Atlanta Fed's research department, Alexander Ruder, principal community and economic development adviser, and Ellyn Terry, economic policy analysis specialist at the Atlanta Fed and a PhD student at the University of Washington

_______________________________________

1 The case study of one hypothetical individual allows us to present a detailed analysis of how the acts and social safety net support an individual with specific characteristics. However, the results are not easily generalizable to a larger population or to individuals with different family composition, different income, or a different city of residence. Future work will examine how the acts support families with children.

2 For example, the CARES Act includes provisions for the Employee Retention Tax Credit, which provides eligible employers affected by COVID-19 a tax credit worth 50 percent of wages paid up to $10,000 for each employee.

3 For an analysis in a state that expanded Medicaid, see our earlier macroblog.

4 We assume Andrew rents an efficiency apartment. In certain markets, the fair market rent standard has been critiqued as being set too low, such that a high percentage of rental units are priced above the fair market rent.